Scott is the founder and principal investment advisor of Peterson Wealth Advisors. He graduated from Brigham Young University in 1986 and has since specialized in financial management for retirees. Scott is the author of Maximize Your Retirement Income and Plan on Living: The Retiree’s Guide to Lasting Income & Enduring Wealth.

For decades, you’ve dedicated yourself to the mission of Intermountain Health—providing compassionate care and improving lives. As retirement approaches, it’s time to focus some of that same energy on your own financial wellness.

Retiring from Intermountain Health comes with a unique set of benefits, decisions, and opportunities. Understanding your pension options, knowing how your 401(k) works, and making the best decisions on how to replace your paycheck with a reliable stream of income throughout retirement all need your attention.

All of this requires much more than guesswork. It requires careful planning.

At Peterson Wealth Advisors, we specialize in helping Intermountain Health caregivers retire with clarity and peace of mind. Here’s your step-by-step roadmap.

1. Review Your Retirement Timeline and Pension Options

First, understand when you’re eligible to retire with full benefits. Many Intermountain employees consider retiring in their early 60s, especially once they qualify for:

Pension benefits (if grandfathered)

Full vesting in the 401(k) match

Medicare or retiree healthcare options

It’s important to look at more than just your age. Reviewing years of service, health coverage options, and whether retiring early will penalize your benefits.

2. Understand Your 401(k) Plan Options

Intermountain’s 401(k) is a key retirement asset. You may have both pre-tax (Traditional) and after-tax (Roth) contributions, as well as employer match money. At retirement, you’ll face decisions like:

Should I roll over my 401(k) to an IRA?

How should I draw income from it?

What’s the best way to reduce taxes on withdrawals?

We help Intermountain retirees analyze these options and build a plan that maximizes retirement income while minimizing unnecessary taxes.

3. Coordinate Social Security and Medicare

Many healthcare professionals delay Social Security to increase their benefit. But is that right for you? Timing your benefits matters. And if you’re retiring before age 65, you’ll need a healthcare bridge until Medicare kicks in.

We walk you through:

Medicare enrollment windows

Spousal coverage options

Social Security timing strategies

4. Replace Your Paycheck with Purpose

One of the biggest questions we help answer is: “How do I turn my savings into income I can count on?”

That’s where our proprietary Perennial Income Model™ comes in. It breaks retirement into six 5-year segments and aligns your investments accordingly. You get:

A structured “retirement paycheck” every month

Protection against market downturns in early retirement

Protection against inflation later in retirement

Clarity on how much you can spend, give, and save

It’s the opposite of guesswork. And it brings our clients tremendous peace of mind.

5. Don’t Forget Taxes and Legacy Planning

Retiring isn’t just about income; it’s also about efficiency. We help Intermountain retirees with:

Roth IRA conversions

Charitable giving and Qualified Charitable Distributions (QCDs)

Updating estate plans to reflect new goals

You’ve worked hard. Let’s make sure your retirement dollars work hard for you.

Ready to retire from Intermountain Health with confidence?

Visit petersonwealth.com or call (801) 225-0000 for a personalized consultation.

Your Intermountain Healthcare Pension Plan comes with a choice you have to make. You can take a lump sum and keep control of your assets, or choose an annuity and turn them into a steady stream of payments.

Timing matters just as much, because starting now versus waiting can change both the value you receive and the role your benefits play in your retirement planning. Ultimately, the right decision depends on your personal circumstances and a thorough understanding of what each path trades away and what it preserves.

Your Two Core Choices: What You’re Really Deciding

Your Intermountain pension offer is a long-term structure choice. The option you select determines whether this benefit functions more like a steady cash flow or a flexible asset.

Monthly Annuity (Lifetime Income)

Electing the monthly annuity converts your benefit into fixed monthly payments that continue for life. The amount is determined by age and actuarial assumptions at election. Once the stream begins, it is governed by the annuity contract and cannot be adjusted.

The appeal is predictable lifetime income. The limitation is that the payment is level. Intermountain’s pension plan does not provide cost-of-living adjustments, which means purchasing power declines over time when inflation persists. Over a 25- or 30-year retirement, that erosion can materially affect spending flexibility.

Structure also affects payout. A single life annuity provides the highest monthly amount but ends at your death. A joint and survivor election reduces the payment in exchange for continuing benefits to a spouse. That structural tradeoff directly impacts household income security.

Lump Sum (A Transferable Asset)

The lump sum represents the present value of your earned benefit, calculated using interest rate assumptions and life expectancy factors. Pension lump sums are highly sensitive to prevailing interest rates, which influence how future payments are discounted into today’s dollars.

This path creates flexibility. The asset can typically be rolled into an individual retirement account (IRA), integrated with your 401(k), invested according to your allocation strategy, and drawn upon based on your personal income needs. You control timing, tax sequencing, and how this capital fits into your overall retirement savings.

The tradeoff is responsibility and market exposure. Future income depends on allocation, withdrawal discipline, and portfolio performance. There is no contractual guarantee. Instead of a fixed payment schedule, you manage an asset whose outcome reflects investment returns and risk management over time.

Rollover Strategy and Tax Mechanics: Where Precision Matters

A rollover election can be clean and tax-deferred, or it can turn into an avoidable tax problem. The difference often comes down to how the paperwork is processed and where the funds are sent. Below, we’ll cover the mechanics that often cause problems.

Direct Rollover vs. Distribution

A direct rollover sends the lump sum straight from the pension plan to your IRA (or other eligible retirement account). Because the money never lands in your hands first, it typically keeps its tax-deferred status and avoids automatic withholding.

If the plan cuts the check to you instead, it is treated as a distribution even if you plan to redeposit it later. In many cases, that triggers mandatory federal withholding, so the amount you receive can be smaller than the total you meant to roll over.

Mandatory Withholding and Early Withdrawal Penalties

When the lump sum is paid to you rather than sent as a direct rollover, two issues occur: withholding and potential penalties. Both can change how much cash you actually have available to move.1

Eligible rollover distributions paid to you are generally subject to mandatory 20% federal withholding. Additionally, if you take taxable dollars out before age 59½, you may owe an additional 10% tax unless an exception applies.2

What Can and Cannot Be Rolled Over

Most eligible lump sum distributions from employer retirement plans can be rolled over to an IRA or another eligible plan.

Ongoing pension income is different. Once you elect an income form that starts paying out as a stream, those periodic amounts are generally treated as taxable payments to you, not a balance that can be rolled over in a single transfer. This distinction is one reason the rollover decision often needs to be made before payments begin.

Understanding Integration Strategy

A rollover is only step one. The bigger win is deciding how this new account fits into a coordinated retirement-income plan, so it supports cash flow, taxes, and risk management rather than sitting in a silo. A strong rollover integration strategy typically involves:

Account placement: Fold the rollover into the accounts you already have, such as your 401(k) and existing IRAs, so your overall allocation stays intentional, and you avoid ending up overexposed (or underexposed) by accident.

Withdrawal sequencing: Plan future distributions around federal tax brackets, Medicare-related income thresholds (IRMAA), and the timing of other income sources so withdrawals stay proactive and tax-aware.

Understanding required minimum distributions (RMDs): Traditional IRA balances generally have RMD requirements beginning at age 73 (with the starting age scheduled to increase to 75 in 2033 for those born in 1960 or later), which can increase future taxable income if you do not plan for them.

Reviewing Roth IRA conversions: Strategic conversions can sometimes reduce future RMD pressure by shifting dollars from pre-tax accounts into a Roth bucket, but the tax cost and side effects should be modeled before acting.

Portfolio role clarity: Define what this asset is meant to do inside your plan, such as flexible spending, later-life income support, or a legacy reserve, and invest and draw it down in a way that matches that purpose.

A Structured Decision Framework: Matching the Option to Your Retirement Design

The goal is not to pick the “right” option in a vacuum. The goal is to choose the option that fits the way you plan to live, spend, and provide for others.

Define What You Want This Benefit To Do

Some want their pension to function like a personal paycheck that keeps showing up, even if markets are down or plans change. Others want it to behave like an asset that can be shaped around spending needs, tax planning, and long-term goals. Getting clarity on what you want this benefit to do will ground the election and keep the decision practical.

The option that best serves you can depend on the importance of the following:

Covering baseline expenses like housing, utilities, and insurance

Creating flexible spending capacity for travel, hobbies, and family support

Reducing pressure on withdrawals from investments in the early years

Providing a backstop for later years when spending patterns may change

Protecting a spouse from an abrupt drop in household cash flow

Building a buffer for healthcare and long-term care costs

Supporting charitable giving goals

Leaving a legacy to children or grandchildren

Decide Which Tradeoff You Are Willing To Live With

Once you define the job you want your benefits to do, line them up against your options and the trade each one asks you to accept. Annuitizing now tends to fit households that want income to start immediately and stay steady, while giving up some ability to adjust later if spending priorities change.

Taking the lump sum now tends to fit households that want control right away and plan to coordinate withdrawals with the rest of their accounts, while accepting that the long-term outcome depends on disciplined management and a consistent withdrawal approach.

Model The Decision The Way You Will Live It

Modeling turns a permanent election into a decision you can defend. It replaces guesswork with a set of scenarios that reflect your household, not generic averages. The best models also show how the plan behaves when conditions are inconvenient.

Important things to model and consider include:

Your baseline monthly spending and what must be covered no matter what

How income changes when one spouse dies, and what replaces it

Expected inflation and how a level payment holds up later in retirement

A longer-life scenario that reflects the possibility of living well past averages

Taxes year by year, including brackets and how withdrawals stack with other income

RMD timing and how it affects taxable income later in retirement

Portfolio drawdown stress tests during down markets early in retirement

A legacy scenario that estimates what may remain for heirs under each option

A healthcare and long-term care stress test that reflects rising costs and changing needs

Lump Sum vs. Annuity for Your Intermountain Pension FAQs

1. How do I determine whether lifetime income or flexibility is more appropriate for my situation?

Start with the job you want this benefit to do. If you want to cover baseline expenses with a predictable check, a life annuity often supports that goal. If you want adaptability, tax planning control, and the ability to preserve remaining value for heirs, the pension lump approach tends to fit better. Your household budget, other income sources, and who will manage the money later all matter.

2. What are the tax consequences if I mishandle a lump sum distribution?

A mishandled lump sum payment can create unnecessary withholding, immediate taxable income, and possible early-distribution penalties depending on age. The clean approach is a direct rollover to avoid avoidable leakage, then a planned distribution strategy over time.

3. Can I change my mind after I elect the annuity or lump sum option?

In most cases, this is an irrevocable decision once the election is processed and the payments or rollover begin. That is why modeling up front matters. Treat the election like you would any other permanent financial commitment and make it with full context.

4. How does this decision affect my spouse or other beneficiaries?

The election affects survivor protection, the continuity of household cash flow, and what remains for heirs. A joint and survivor election can protect a spouse by continuing payments after the first death, while other elections may end at death or change benefit levels. Beneficiary goals and household income design should be discussed before you sign.

Helping You Make a Confident, Coordinated Pension Decision

Intermountain’s pension election is not a standalone form. It touches cash flow timing, taxes, survivor planning, and how much flexibility you will have in the years that follow. A clear plan brings those moving parts into one coordinated decision.

At Peterson Wealth Advisors, we work with Intermountain Health employees to compare each election path side by side, and translate the numbers into real-world outcomes. We build the strategy around your goals, your household, and your timeline, then integrate the election into your broader plan so it supports long-term stability and flexibility.

Don’t wait to get help exploring your options. If you want to see how your pension choices fit with the rest of your retirement picture, schedule a complimentary consultation with our team today.

You’ve spent decades accumulating a pension benefit and building your retirement savings through Intermountain Health’s 401(k). Perhaps you have accumulated additional assets in HSAs, IRAs, or spousal plans along the way. But now comes the bigger question: How do I turn these assets into income I can actually live on, month after month, year after year?

At Peterson Wealth Advisors, we work with Intermountain Health Retirees to create exactly that: a structured, sustainable, and stress-free retirement income plan.

Our proprietary solution is called the Perennial Income Model™, and here’s how it transforms uncertainty into clarity.

The Problem With Traditional Withdrawal Strategies

Most retirees lack an actual retirement income plan built specifically to address their unique needs. Instead, they are told to “just withdraw 4% each year.” But what happens when the market drops 20%? What if inflation spikes or your expenses shift? And how do you know which accounts to tap first?

For Intermountain caregivers that are used to steady paychecks, this kind of guesswork feels risky and uncomfortable.

You need a smarter strategy that:

Matches your current investments with your future income needs

Minimizes market risk when you’re most vulnerable

Gives you confidence to spend, without fear of running out

We divide your retirement into six 5-year segments, each with a specific responsibility to provide income for a five-year period of your retirement. Think of it as a series of retirement “paychecks” that change and adapt with you over time.

Segment 1 (Years 1–5): Stability and Access

This segment is invested conservatively and provides the income you need immediately in retirement. It’s your safe and dependable financial foundation.

Segment 2 (Years 6–10): Protected but Growing

Segment 2 is slightly more growth-oriented but still designed for stability. These assets will soon be your paycheck source and are positioned to support you without excessive risk.

Segments 3–6 (Years 11–30): Growth for the Long Haul

These later segments are invested with increasing levels of growth, aiming to outpace inflation and keep your income strong—even in your 80s and 90s.

Benefits for Intermountain Retirees

1. Predictable Paychecks

The Perennial Income Model™ allows us to structure distributions so that every month, you get a “retirement paycheck.” No guesswork. No scrambling.

2. Tax Efficiency

We tailor withdrawals from Roth, Traditional, and taxable accounts to reduce your tax burden over time. This is especially helpful for Intermountain retirees with both pre-tax and Roth 401(k) contributions.

3. Risk Management

The two biggest risks for retirees are market volatility and inflation. Because your early retirement years are funded conservatively, you’re not forced to sell stocks during market downturns. Money designated to provide income during the later years of your retirement is invested for growth to keep up with inflation.

4. Flexibility for Living Your Best Life, Serving, Traveling, or Giving

Whether that means traveling, serving in your church or community, or spending time with your family, the segmented design makes it easier to plan for larger, short-term expenses without disrupting your overall income strategy.

5. Confidence in Retirement

When you know what you can spend (and where it’s coming from), you make decisions with confidence. That’s a powerful shift from “Will I run out?” to “How do I want to live?”

Real-Life Application for Intermountain Retirees

We’ve used this model to help:

Nurses transition to early retirement with confidence

Physicians phasing out of practice into semi-retirement

Administrators maximizing Roth conversions during low-income years

Couples coordinating their incomes for maximum tax efficiency

Each plan is customized, but all are grounded in the same powerful structure.

Want to turn your Intermountain benefits into a clear, structured retirement paycheck? Let’s create a plan that brings lasting peace of mind.

Visit petersonwealth.com or call (801) 225-0000 to schedule your complimentary Perennial Income consultation.

Peterson Wealth Advisors is a fee only registered investment adviser. The information presented is for educational purposes only. Please consult with a qualified financial advisor before implementing any strategy.

A generation ago, retirees didn’t have a lot of choice when it came to how they would structure their retirement income. They had Social Security, and their guaranteed monthly pension checks were provided by the employer they had dedicated thirty years of their lives to. In 1975, almost 80% of retirement income came from Social Security and defined benefit pension plans. The employees had little opportunity to contribute towards their own retirements through payroll deduction programs like 401(k)s. Employer-provided pensions are technically defined benefit pension plans. For ease of understanding, I will refer to these plans as “pensions.”

The Shift from Pensions to 401(k)s

The various plans where employees and employers can deposit into individual accounts are called defined contribution plans. Again, for ease of understanding, I will refer to all the various defined contribution plans as 401(k)s. The 401(k) was born in 1978, and it gained immediate popularity and started replacing the traditional pension plan. In 1975, there were 103,346 pension plans in the U.S.; today, there are fewer than 45,000. Additionally, the majority of the 45,000 remaining pension plans are found in the public sector with states, municipalities, universities, and school districts. It is estimated that there remain fewer than 7,000 private sector pension plans in the United States.

Following the national trend, Intermountain Health announced on January 20, 2026, that it is freezing its pension plan. Freezing a plan does not mean that employees will lose their pensions; it means that Intermountain Health will stop funding or adding more money to existing plans. Participants of the pension will continue to have the choice of receiving a guaranteed monthly income when they retire, or they will be able to roll the value of their pension into an IRA. Like other corporations, Intermountain Health decided to use the money that was being allocated to fund their pension in alternative ways, which would be more beneficial to their caregivers.

There are three reasons why companies are transitioning from the traditional pension plan to 401(k)s

Pension plans have become too burdensome for most employers to maintain.

The decline of the traditional pension plan began in the 1970s when the government tried to rectify the abuse it saw in corporate America. They did this by passing the Employee Retirement Income Security Act (ERISA). While ERISA has corrected much of the corporate abuse over the years, it also introduced many complicated laws that are hard to comply with. To avoid dealing with the politics and complexities of ERISA, many companies decided to do away with their pension plans. They were never a mandatory offering for companies, and it was easier to do away with the plans than to conform to ERISA’s complex regulations.

There is a tremendous liability for companies that provide pension plans.

Companies that offer these plans must, by law, provide current retirees with their pre-determined retirement benefit every month, even if the pool of money the pensions are paid from underperforms. Pension payments, especially during turbulent economic times, have the potential to put a company out of business. As companies calculate the risks, the costs, and the difficulty of maintaining pension plans, most companies conclude that there are better ways to provide value to their employees.

Monthly pension payments come from an investment portfolio managed by the pension plan. Many pension plans don’t have sufficient money in their plans to pay projected obligations; or, in other words, they are underfunded. In fact, the latest studies indicate that pension plans across the United States are underfunded by hundreds of billions of dollars. Intermountain Health’s pension plan is fully funded. The management of Intermountain Health’s pension plan has done an excellent job saving and investing to ensure that there will be sufficient dollars to be able to pay all the current and future obligations that it has to their employees.

Times have changed.

Employers recognize that pension plans do not protect and benefit their employees as they once did. Two societal changes have made pension plans less beneficial:

First, we have become a much more mobile society.

Gone are the days when an employee worked for one company for an entire career. Pension plans rewarded the long-term employee with a monthly retirement check, but these rewards came with a cost— not of money, but of time. The price to be eligible for these plans was decades of loyalty to a single company.

401(k) plans of today are much better equipped to deal with the shorter duration that most workers commit to a single employer. Even if employees work for an employer for a short amount of time, they can roll 100% of their contributions to a new 401(k), or to an IRA, upon terminating employment with the employer.

Second, longer life expectancies.

Inflation has always been with us, but this generation has a unique challenge when it comes to inflation. It is rare to find a private sector company with a cost-of-living benefit included within its pension plan. In other words, the monthly payments that retirees receive from their pension are usually not adjusted for inflation. Intermountain Health’s pension does not adjust for inflation. If you only live 10-15 years in retirement, as did previous generations, inflation does not have time to become a lifestyle-changing problem. Many of today’s retirees will live thirty years or more in retirement, and thirty-year retirements are destroyed by inflation. For example, if you start your retirement receiving a $3,000 dollar per month pension payment, and your payment is not adjusted for inflation, your monthly payment will stay $3,000 until you die. The historical inflation rate in the United States has been close to 3%, and at just a 3% inflation rate, the $3,000 monthly payment will only be able to buy the equivalent of $1,200 worth of goods and services at the end of a thirty-year retirement. That is a sixty percent cut in pay. Because of inflation and longer life expectancies, traditional pension plans do not furnish the security that they were originally intended to provide.

Before we get into the impact that this change will have on caregivers, I first want to remind you of the benefits that come with participating in a 401(k) plan.

Key Benefits of 401(k) plans:

Tax Savings Now (Traditional 401(k)): Contributions are deducted from your paycheck before taxes, reducing your current taxable income and potentially lowering your tax bracket.

Tax-Deferred Growth: Your investments grow without being taxed each year, letting your money compound more effectively.

Tax-Free Withdrawals (Roth 401(k)): If you choose the Roth option, you pay taxes now, but qualified withdrawals in retirement are completely tax-free.

Employer Match: Many employers contribute money to your account, often dollar-for-dollar up to a certain percentage of your salary – essentially free money.

Compound Interest: Starting early allows your earnings to generate their own earnings, significantly boosting your savings over time.

Convenience: Contributions are automatically taken from your paycheck, making saving effortless and disciplined.

Higher Limits: You can save more in a 401(k) annually compared to an IRA.

Portability: You can take your 401(k) with you when changing jobs, often by rolling it over.

The Impact of Freezing the Pension and Enhancing the 401(k) for Intermountain Health Caregivers

Since the announcement of this change, I have heard some Intermountain Health employees express that they are “losing their pension.” That statement is false and puts a negative spin on what I believe to be a very positive development. Intermountain Health is simply reallocating resources from the pension plan to the employees’ 401(k) plans. Beginning January 2027, Intermountain Health is going to pay all caregivers an additional 2% of their salary to their 401(k). Adding this, along with the already generous match that Intermountain Health provides to its 401(k) plan participants, makes Intermountain Health’s 401(k) one of the elite 401(k) plans in the country. Additionally, the company is allowing its employees to rollover the value of their pensions, while they are still employed, to an IRA or to their existing 401(k)s at Intermountain Health.

By freezing the pension plan and enhancing the 401(k) plan, Intermountain Health is putting its employees in charge of their own destiny. Caregivers should be excited about the opportunity to have more control over their own finances. Granted, some caregivers will need to be more thoughtful than they have been in the past as they manage their own 401(k)s. Some will need to become better educated. Even though this change will place more responsibility upon caregivers to manage their own retirements, there is a tremendous upside for those who learn, take advantage of this opportunity, and utilize the tools and the resources that they are given to enhance their retirement and grow their 401(k).

Intermountain Health is dedicated to the personal success of its caregivers, and they recognize that additional educational opportunities will need to be offered to ensure a successful transition and to prepare employees to have the best possible retirement. Intermountain Health has asked our company, Peterson Wealth Advisors, to teach the same class that we teach to employees at Brigham Young University and to the alumni of Utah Valley University to Intermountain Health caregivers. This online class helps participants to make sound decisions regarding their 401(k)s now and prepares future retirees with the knowledge they will need to make the best decisions at retirement. The class objective is to teach attendees how to create a tax-efficient, inflation-adjusted stream of income that will last throughout retirement.

Details as to the timing of the class will be forthcoming.

How can any retiree make a good decision about reducing taxes in retirement, without first mapping out, and projecting a future income stream?

The answer is. . . they can’t. All of us tend to be short-sighted when it comes to making tax-saving decisions. I say short-sighted because we focus on how we can save tax dollars in the current tax year, without giving long-term tax saving moves little thought. For the retiree, a little bit of planning can go a long way in saving future tax dollars.

A comprehensive retirement income plan must consider a lifetime tax reduction strategy that focuses on how today’s decisions to withdraw money from the various types of accounts will impact their tax liability years into the future. The Perennial Income Model™ from Peterson Wealth Advisors projects future income streams for the retiree enabling them to recognize and organize long-term tax-saving opportunities.

Three retirement account tax categories

Before looking at strategies to maximize your lifetime tax savings, you must first understand the categories of retirement accounts and the tax implications of withdrawing income out of each type of account.

Tax-deferred retirement accounts

The money in IRAs/401(k)s and a variety of other company-sponsored retirement saving plans are 100% taxable upon withdrawal unless you use the Qualified Charitable Distributions exception (to be explained). I am likewise going to lump non-IRA annuities into this category. The difference is that only the interest earned on the non-IRA annuity is taxed upon withdrawal, not the entire value of the annuity.

Tax-free retirement accounts

The funds in Roth IRAs and Roth 401(k)s can be withdrawn tax-free.

Non-retirement accounts (after-tax money)

Investments that are individually owned, jointly owned, or trust owned have their dividends and interest taxed annually. They are also subject to capital gains taxation in years when investments are sold at a profit.

Three strategies to reduce your taxes in retirement

At Peterson Wealth Advisors we utilize our Perennial Income Model to provide the organizational structure to recognize opportunities to reduce taxes in retirement. Let’s consider three of these tax-saving strategies:

1. Managing investment income according to tax brackets

Thankfully, your retirement income stream can come from a mix of tax-deferred, tax-free, and non-retirement accounts used in combination to lower your tax liability.

The key is to determine which of the above categories of accounts should be tapped for future income needs, and when. Tax-efficient income streams that are thoughtfully mapped out at the beginning of a retirement be extremely effective to help minimize your lifetime tax burden. With advanced planning, you can avoid the costly mistakes of conventional wisdom, such as: withdrawing from after-tax and Roth IRAs early in retirement and waiting to tap into taxable IRAs until the Required Minimum Distribution rules mandate withdrawals at age 73.

This mistake results in the retiree paying minimal taxes from retirement date to age 73, then paying high taxes and higher Medicare premiums from age 73 until death. The Perennial Income Model shows us that withdrawing some taxable money from IRAs early in retirement levels out the retiree’s tax burden and keeps the retiree from being forced into higher tax brackets once the RMD rules kick in.

When you thoughtfully structure your retirement income streams from a variety of tax locations within your portfolios, you can experience a higher standard of living while still paying very low tax rates.

2. Qualified Charitable Distributions

The most overlooked, least understood, and one of the most profitable tax benefits recognized by forecasting income streams through the Perennial Income Model comes as future Qualified Charitable Distributions are planned.

Qualified Charitable Distribution, or a QCD, is a provision of the tax code that allows a withdrawal from an IRA to be tax-free if that withdrawal is paid directly to a qualified charity. Charitable contributions are itemized deductions but because of the high personal exemptions associated with today’s tax code, few itemize. Thus, for those that do not itemize deductions, the only way to get a tax benefit by making a charitable contribution is by doing a QCD.

The Perennial Income Model becomes a valuable tool to help the retiree to spread their IRA throughout retirement in coordination of their future charitable giving plans. By simply altering the way contributions are made to charity, you can make the same charitable contribution amounts and reduce your taxes at the same time.

For more details on Qualified Charitable Distributions for the Latter-day Saint retiree, visit here.

3. Roth IRA Conversions

Converting a tax-deferred IRA into a tax-free Roth IRA can be a valuable tool in the quest to reduce taxes during retirement. Unfortunately, few retirees get it right deciding when to do a Roth conversion, deciding how much of their traditional IRA they should convert, or even deciding if they should convert any of their traditional IRAs at all. As advantageous as Roth IRA conversions can be, they are not free!

The price you pay to convert a traditional IRA to a Roth IRA comes in the form of immediate taxation. 100% of the conversion amount is taxable in the year of the conversion. For this reason, investors must carefully weigh whether doing a Roth conversion will improve their bottom line.

Without a projection of future income that the Perennial Income Model provides and the subsequent projection of future tax liability, it is virtually impossible to determine whether a Roth IRA conversion is the right course of action.

Perhaps the greatest unanticipated benefit that we have observed since creating the Perennial Income Model is its ability to clearly estimate future cash flows and subsequent future tax obligations for our retired clients. Given this information, the decision of whether to do a Roth conversion becomes apparent.

The Perennial Income Model™ as a tax planner

We first designed the Perennial Income Model to provide the structure to reinforce rational decision-making. It started with a focus on helping retirees match their current investments with their future income needs. Now, we see that the Perennial Income Model’s role is much bigger, including providing the structure to be able to see where future tax-saving opportunities can be realized.

To see how the Perennial Income Model can work with your retirement situation, visit PetersonWealth.com to sign up for a complimentary consultation with a Certified Financial Planner™.

As members of The Church of Jesus Christ of Latter-day Saints, we are accustomed to paying tithing and making other charitable offerings. Our motive for these donations is certainly not for the tax benefit. But as wise stewards over the material blessings with which we have been blessed, we should do all we can to make the most of our donations and pay our charitable obligations in the most tax-efficient way possible.

As a financial advisor, I often see retired members of the Church paying more income tax than necessary because they do not understand what a Qualified Charitable Distribution (QCD) is, and how this provision of the tax code could save them hundreds or even thousands of dollars annually in taxes.

A Qualified Charitable Distribution (QCD) is a provision of the tax code that allows a withdrawal from an IRA to be tax-free as long as that withdrawal is transferred directly to a qualified charity such as the Church.

These tax savings are brought about by simply altering the way LDS contributions are made to charity. Unfortunately, QCDs can only be used by persons over age 70.5. But since we will all be at that age sooner than later; it is beneficial to understand how they work so you can plan for your own future and so you can share this information with your fellow Latter-day Saint retirees.

Taxation 101: Understanding the Basics

Before I explain how a QCD might benefit you, let’s first review how we are taxed. Simply put, as you calculate your tax liability, you first add up all your income and then subtract deductions to come up with your taxable amount. We will all get a deduction.

The IRS has a list of itemized deductions such as mortgage interest and charitable contributions that we can subtract from our tax liability. The IRS also has a standard deduction number that we can subtract from the taxes we owe if our itemized deductions do not add up to more than the standard deduction amount. In essence, we are allowed to subtract the greater of our itemized deductions or the standard deduction from our tax liability.

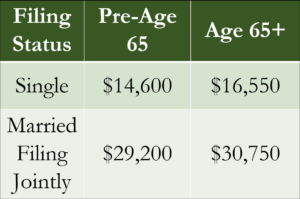

Why is this important to understand? Unless you have itemized deductions in excess of the standard deduction amounts seen in the graphic below, you will not itemize your deductions—you will default to taking the standard deduction.

You only receive a tax deduction for making charitable contributions if you itemize your deductions, and because of the higher standard deduction amounts, only 10% of Americans itemized their deductions last year.

That means that for the 90% of the people who do not itemize and take the standard deduction, there is no tax benefit for paying tithing or making any other type of charitable donation.

By donating via a QCD, you will receive a tax benefit for your donations even if you do not itemize and take the standard deduction.

2024 Standard Deduction Amounts:

Advantages of using a Qualified Charitable Distribution

Making charitable LDS contributions by doing a Qualified Charitable Contribution is a unique tax saving strategy:

You didn’t have to pay income tax when you earned the money that you put into an IRA or 401K.

You didn’t pay taxes on the compound interest your IRAs earned over the years.

Any money paid directly to a charity using a QCD from your IRA will not be taxed.

In running projections with our clients, we have discovered that in almost every instance, those who give to charity and simultaneously make distributions from an IRA can benefit from doing a Qualified Charitable Distribution. We have also found that even those that currently itemize their deductions still benefit from doing a QCD.

We believe that every person over age 70.5, who has an IRA, and who gives to charity should consider making charitable contributions via QCDs. You or your tax professional can run tax comparisons by paying charitable contributions the traditional way versus doing a tax-free transfer from your IRA to a charity using an QCD. Many of you will find the tax savings to be significant.

There are rules, regulations, and instructions on how to report Qualified Charitable Distributions that are too extensive for this article to properly cover but additional information regarding QCDs can be found on our website.

Additionally, examples of how QCDs have benefited retired couples can be found on our website at petersonwealth.com.

You may currently be missing out on a lot of tax savings if you ignore the benefits of the Qualified Charitable Distribution. Saving substantial amounts of money each year by simply altering the way you pay your charitable donations is worth investigating.

Most of us sacrifice and save for four decades in preparation for what we hope will be a comfortable retirement. We are laser-focused during our working years on accumulating as much as possible, and by the time we retire, many of us have refined the art of wealth accumulation in our IRAs, 401(k)s, and a variety of other investment accounts. We feel pretty confident in our retirement preparation and then something happens that shatters our confidence…we retire. We quickly come to the realization that successfully investing and managing the distribution part of retirement takes a completely different skill set than accumulating money in retirement accounts.

Besides the universal question of how to invest, there are questions regarding distributions, taxes, risk, and keeping our income up with inflation that will all have to be addressed as we transition from accumulating to distributing our retirement accounts. All these questions bleed into the single, overarching question that every retiree needs to figure out: How am I going to create an inflation-adjusted stream of income from my investments that will last for the rest of my life?

The Need for a Retirement Income Plan

The quality of the next 30 years of your life is dependent upon the decisions that you make at retirement and the plan you put in place. There is so much on the line, and mistakes made at the beginning of retirement are not forgiving. There are no do-overs. A well-thought-out retirement income plan will provide discipline, order, safety, and peace of mind. A sound retirement income plan will allow you to focus on your retirement dreams and not be obsessed with the daily movement of markets, interest rates, or how current events will impact your retirement.

A retirement income plan should be unique to you and your specific needs. So, copying your retired neighbor’s retirement income plan won’t work. Following some generic, “rule of thumb” withdrawal advice from your financial advisor won’t get it done, and buying an annuity that will never keep up with inflation over a long retirement will only serve to crush your future purchasing power. And finally, decades of investing have already taught you the futility of market timing and betting your future on guessing the direction of the stock market.

Now that I have shot down all the popular attempts to create retirement income streams, and before I show you how a professional retirement income plan is created, let’s address what it is that we need a retirement income plan to do.

A Successful Retirement Income Plan Must Address Five Objectives

It must be goal specific.

It must create a framework for investing.

It must create a framework for distributing.

It must create a framework to reduce risk.

It must create a framework for reducing taxes.

Goal Specific

A retirement income plan that is goal-driven provides detailed objectives. It is a date-specific, dollar-specific blueprint that will guide you throughout retirement. A date-specific, dollar-specific plan defines how much income will be needed during retirement, and when it will be needed. Its objective is to deliver future income to the retiree with the least amount of risk, after all risks have been considered. A properly structured retirement income plan matches your current investment strategy with your future income needs. Like any goal-driven program, the performance toward reaching the goal must be monitored to maintain discipline and allow for adjustments if the goal is to be realized.

Create a Framework for Investing

Retirees must find the proper investment mix of low-volatility fixed-income investments and higher-yielding, more volatile equities.

Fixed-income investments such as bank deposits and certain types of bonds can provide a haven to draw income from when the stock market takes its occasional dive. As valuable as these types of investments can be in the short term, they are a long-term liability that will never keep up with inflation.

On the flip side, retirees need to own some equities in their portfolios. Owning higher yielding equities is a logical way to keep ahead of inflation over the long run. But we all know that short-term volatility and unpredictability afflict all who own equities. Creating a retirement income plan that takes advantage of the opposing nature of fixed-income and equities is an essential component in creating a long-lasting retirement income plan.

It’s just commonsense to invest the money we’ll need in the short-term into fixed-income type investments and invest the money we don’t think we will need for a while into stock-related investments. But, most retirees and their advisors don’t invest this way. Unfortunately, the failed practices of chasing last year’s returns and making investment decisions based upon guessing the future direction of the stock market continue to be the prevalent methods used to determine investment allocations, even though these methods have proven to be extremely unreliable.

Following a plan that allocates retirement savings by determining short versus long-term income needs liberates the retiree from having to time the markets or beat the stock market average by superior investment selection. With an investment plan that matches current investments with future income needs, the retiree only needs to concentrate on maintaining discipline and following the plan.

Create a Framework for Distributing

When it comes to withdrawals from investments at retirement, I have noticed two types of personality traits. The first trait is manifested in individuals I will call the “entitled spenders” who think to themselves, “I have been saving all my life for retirement, and I am now retired, so I am going to spend however much I want on whatever I want.” The second type I will call the “paranoid savers”. These people are those who think, “I may have a lot of money, but it has to last a long time. And who knows what the future might bring?” These types of individuals are often afraid of spending any of their retirement funds at all.

The “entitled spenders” sabotage their retirement by spending too much, too early, as they burn through all their retirement savings in the first ten years of possibly a thirty year retirement. The “paranoid savers” likewise harm their retirement by living below their privilege by denying themselves many of the simple pleasures and opportunities of retirement. Ironically, both the spenders and the savers would greatly benefit from the same date-specific, dollar-specific retirement income plan, a plan that outlines how much money can and should be withdrawn from investment accounts and when.

Quite literally, the million dollar question is, “How much can/should I withdraw from my investments each year?” You must be able to answer this question if you’re going to have a sustainable income stream throughout retirement, and if you’re going to be able to enjoy your retirement experience to the fullest.

A sustainable withdrawal rate can be created through determining the answers to three important questions:

How much income will I need to pull from my investments to sustain my retirement lifestyle?

When will retirement savings need to be converted into retirement income?

How should retirement accounts be invested until they are needed to be converted into income?

Again, having a retirement income plan that includes date-and-dollar specifics should drive your withdrawal decisions. Adjustments in either the timing of withdrawals, the withdrawal amounts, or how retirement funds are invested between now and the future income date will impact your future income stream.

Create a Framework to Reduce Risk

A viable retirement income plan must recognize and minimize risks where possible. Retirees are particularly susceptible to three kinds of risks:

Inflation risk

Stock market risk

Behavioral risk

Inflation Risk

When it comes to inflation, you must ask yourself the following, “How do I invest to maintain my purchasing power and stay ahead of inflation?”

Inflation is the gradual but lethal loss of purchasing power. Currently, we are going through a period of high inflation but historically, the long-term inflation rate has averaged 3%. At just a 3% inflation rate, $1.00 will only be able to purchase $0.41 worth of goods and services at the end of a 30-year retirement. Unless you are willing to reduce your lifestyle and spending habits by about 60% during your retirement, inflation must be dealt with. Fortunately, the risk of inflation can be mitigated by investing in inflation-beating equities. The retirement income plan I will show you later in this blog helps by deliberately designating a portion of a portfolio toward long-term inflation protection.

Stock Market Risk

How do I maintain investment discipline throughout retirement and not make major mistakes during periods of market volatility? Market corrections are part of the investment cycle and should be planned for. Successful investors follow plans and are patient, while unsuccessful investors follow the breaking news and daily movements of the stock market and are prone to panic. Informed investors manage stock market risk by being diversified and patient because they understand every bear market is eventually followed by a bull market. Having a plan in place is the antidote to panic. Knowing what you own, and why you own it, goes a long way towards helping you stay the course during periods of market turbulence.

Behavioral Risk

Two related questions come to mind when considering the behavioral aspects of a retirement income plan:

How do I protect myself from my older self when my financial judgement is clouded by age?

How do I provide the less financially savvy spouse with a plan to follow that will provide for his or her financial needs after my death?

Retirement is not a time for investment experimentation. It’s not a time to be tossed about by every headline on the nightly news or story on the internet. It isn’t a time to change your investments based on irrational exuberance or equally irrational fear. A goal-specific income plan goes a long way toward helping to navigate the emotional roller coaster of investment management now, and especially as you age. It can also be a valuable tool to provide guidance to a spouse upon your death. A date-specific, dollar-specific retirement income plan helps protect your future from perhaps its greatest threat — you.

Create a Framework for Reducing Taxes

From which accounts, or combination of accounts, should I withdraw retirement income from to give myself the most tax-efficient income stream? Should I withdraw from my IRA, my Roth IRA, or my non-retirement accounts? How do I go about managing my Required Minimum Distributions?

Tax-saving opportunities rarely happen by accident. Rather, they come about through careful planning. This is especially true with retirees. Keeping retirees in lower tax brackets throughout retirement can be done by managing withdrawals from pre-tax versus after-tax investment accounts. In other words, the retiree can take income from IRA accounts until they reach the top of a tax-bracket and then take the balance of their needed income for the year from an after-tax account. This is an easy concept to visualize but a little more difficult to implement. What adds to the complexity is that implementing this plan has to integrate with the framework for investing and the framework for distribution sections that I just mentioned. At this point, it might sound daunting to bring all of this together. As we create the income plan in the next section, you will be able to see how all these components can integrate with each other.

Retirement Income Plan Creation

Now that I have explained the retirement income challenge, and what your retirement income plan must address, let me demonstrate how a professional retirement income plan is structured. In 2007, we created our proprietary retirement income plan that we call the Perennial Income Model™. It has helped hundreds of retired families successfully navigate their retirements during the volatile years since its inception. The Perennial Income Model is goal-based and creates the essential frameworks for investing, distributing, reducing risk, and reducing taxation, as previously mentioned.

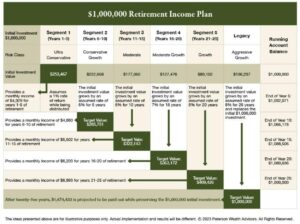

Allow me to introduce the Lee family who we will build a retirement income plan for. Tony and Kathy Lee are both 65 and are ready to retire. They have accumulated $1,000,000 in their 401(k) and their after-tax brokerage accounts. They want to know how they should invest the million dollars and how much income they should expect to receive from that sum of money. They feel a retirement income plan spanning 25 years should be sufficient, and they would like to pass the full $1,000,000 to their children upon their deaths, if possible.

When it comes to making investment decisions, the most important consideration is an investment’s time horizon. In other words, how long will the money be invested? The Perennial Income Model matches the Lee’s current investment portfolio with their future income needs by dividing their money into various investments that have different objectives based upon when a particular segment of their money will be called upon to provide future income. Therefore, the Perennial Income Model will divide the $1,000,000 they have accumulated for retirement into six different accounts. The first five of these accounts are responsible for creating retirement income for five different five-year periods of the Lee family’s retirement. I will refer to the accounts that cover the five-year period of income as segments. So, Segment 1 is responsible for providing the income for the first 5 years of retirement, Segment 2 for years 6-10 of retirement, Segment 3 for years 11-15 of retirement, and so on… until 25 years of retirement are covered.

The sixth segment, or Legacy Segment, is designed to create a fund that will replace the original investment of $1,000,000 to the Lee family at the end of 25 years. This provides money for their heirs or can serve as an insurance policy should they live longer than 25 years or experience large end-of-life expenses like nursing home costs. The accompanying chart shows the retirement income plan being built for the Lee family — I will walk you through it to make sure it all makes sense to you.

The Perennial Income Model Walk-Through

The underlying principle of the Perennial Income Model is matching current investment portfolios with future income needs. Therefore, the money that the Lee’s depend on to provide income in the short-term is invested in conservative investments that provide safety from volatile markets. The money that won’t be needed to create income for a prolonged period is invested into more aggressive investments that keep up with inflation. Segment 1 will provide income for the first five years of retirement. It will be invested into a conservative account that will systematically distribute $4,329 monthly to the Lee’s checking account.

Segment 1’s primary responsibility is safety of principle because it’s sending out a monthly payment immediately; so, this segment is the most conservatively invested. We assume only a 1% rate of return on the money invested in Segment 1. Certainly, in today’s environment retirees can, and should, expect a higher return than 1% on their conservative money. We also expect to outperform the conservative assumptions for the other segments as well. By choosing to underestimate performance, we avoid creating a false sense of security and unrealistic income expectations. Obviously, if the Perennial Income Model works with the conservative assumptions we are using, it will work better as investment performance exceeds these assumptions.

Segment 2 will take over the role of providing monthly income to the Lees once Segment 1 runs out of money at the end of the fifth year. Since the money from Segment 2 will not be needed for at least five years, it can be more aggressively invested than Segment 1, but it can’t be significantly more aggressive. A prolonged bear market could last longer than five years, so the bulk of this money should also avoid volatile investments. That’s why only a 5% return is assumed during the five years it’s invested before being turned into income in year 6.

Segment 3 will be invested for ten years before it will be called upon to create income for years 11-15. Because the money in this segment won’t be used for ten years, Segment 3 is moderately invested in a 50% stock/50% bond portfolio. A conservative 6% return is assumed for this segment.

You can see from the chart, Segment 4 assumes a 7% growth rate and Segment 5 and the Legacy Segment assumes an 8% growth rate. We use these higher growth assumptions because these segments are more aggressively invested. Investments that will not be needed for fifteen years and beyond must invest into a diversified portfolio of equities to keep up these higher growth assumptions. History has shown us that, in the long run, equities have always beaten inflation and have given us superior returns. It’s understood these inflation-fighting segments will experience occasional bouts of volatility that the stock market imposes with regularity. But given the long-term nature of these segments, short-term volatility is inconsequential. The key to making the stock market work for you is to maintain discipline and stay invested during periods of volatility. Following the Perennial Income Model will provide the discipline that is needed.

Harvesting

At first glance, the Perennial Income Model appears to become more aggressively invested as the retiree ages and gets into the latter segments of the plan. Having 80–90-year-old retirees with all their money invested in long-term, aggressive equity portfolios doesn’t make any sense. Fortunately, this is not how this retirement income plan works when the income model is properly managed and “harvested.” In financial terms, the process of harvesting is transferring riskier, more volatile investments into a conservative and less volatile portfolio once the target, or goal, of each segment is realized. The target, or goal of each segment is the number found in the dark green box associated with each segment.

For an example of harvesting, let’s look at Segment 4. You can see that the initial investment in Segment 4 is $127,476 and we know that if this initial investment grows by the assumed growth rate of 7%, it will reach its target, or goal amount by the projected fifteenth year. Segment 4 is invested in a moderate growth portfolio (70% stocks, 30% bonds). According to a study done by Vanguard, the historical return of a moderate growth portfolio has averaged an annualized return of 9.4% since 1926. So, it would be plausible, if history simply repeated itself, that the investment portfolio in Segment 4 would reach its goal of $363,172 before year 15 (at a 9% growth rate, the segment reaches its target in 12 years). Once the target is reached, no matter what year that happens, the investment needs to be harvested and preserved. That means the equities in the segment that have reached their target goal must be moved into more stable and conservative investments.

We have found, the key to successful outcomes is to begin with conservative growth assumptions and then maintain the discipline to harvest portfolios in the segments when they reach their targets.

Five Insights to Point Out:

Notice the account balance stays roughly the same throughout retirement (see the far-right column of the chart). People often assume that as segments are liquidated, the overall portfolio balance is going down, but that’s not the case. Recall that as the early segments are being liquidated, the later segments are invested and growing.

Notice that the retirement income plan is projected to automatically increase the Lee’s income every fifth year by an annualized 2.6% rate to help offset the effects of inflation.

To keep things simple and to help you to understand how the Perennial Income Model works, I have not incorporated any other sources of income such as Social Security or pensions into our example. But, for tax planning purposes, projected Social Security, pension, and other sources of taxable income should be incorporated into the retirement income stream projections. Once the income stream is created by adding all sources of income, thoughtful consideration should be made to determine which type of account (IRA, Roth IRA or after-tax account) should be allocated into the various segments for maximum tax efficiency.

Assumed growth rates are purposefully overly conservative. Historically, the S&P 500 has averaged more than 10%, and the largest assumed growth rate used in the most aggressive segment is only 8%. If you feel that these assumed growth rates are not realistic, you can always adjust the income plan to run at lower or higher growth assumptions. The Perennial Income Model uses conservative growth assumptions within the retirement income plan in hopes that the target for each segment is reached prior to the date it’s needed to provide income.

Please look at the bottom line of the chart. Based upon these conservative assumptions, the Lee family will receive $1,674,433 of income during their 25-year retirement and leave $1,000,000 to their heirs.

Conclusion

I end with the question that all new retirees and those approaching retirement need to ask themselves, “Will I outlive my money, or will my money outlive me?” Without knowing anything about your finances, I can tell you that you will be much more likely to have your money outlast you if you follow a plan. Your retirement income plan should be goal-based and should serve as a guide to your financial decision-making for the rest of your life. It should drive your investments, withdrawals, and even influence your spending and gifting decisions.

The Perennial Income Model appeals to those seeking a logical, goal-based roadmap for investment management during retirement. It reduces the retirees’ need to be anchored to the daily movements of the stock market which, in turn, will provide them with greater peace of mind and will make them less vulnerable to making the irrecoverable investment mistakes that so many retirees make.

Retirees that follow the Perennial Income Model understand why they are invested, when they will need a specific portion of their investments to provide future income, how much they can safely withdraw, and how their dollars will need to be invested to accomplish their goals. They will also realize a more tax-friendly way to navigate retirement. The Perennial Income Model is designed to provide a secure stream of income in the short-term, while providing an inflation-adjusted stream of income for the retiree’s future.

Hopefully, you can now see that there is so much more to planning retirement income streams than buying an annuity and more to consider than following generic and overly simplistic rule of thumb guidelines to manage your finances during retirement.

My hope is that this blog has opened your eyes to a better way to invest during retirement and that you might be able to incorporate some of the ideas found in this blog so you might face your financial future with confidence and have the peace of mind to free you to pursue your retirement dreams.

The Perennial Income Model is explained in greater detail in my book “Plan On Living”. You can get a complimentary copy of my book and get a better understanding of the services that we offer by visiting here.

Scott Peterson was a guest writer on the popular White Coat Investor blog—a blog esteemed amongst physicians and other high-income professionals. Scott’s blog outlines our proprietary process for investing, The Perennial Income Model™. The article also presents a retirement income plan creation example of a couple who have accumulated $1 million for their retirement.

“You must pay taxes. But there is no law that says you gotta leave a tip.” -Morgan Stanley

How can any retiree make a good decision about reducing taxes in retirement, or any financial professional recommend a proper course of action, without first mapping out, and projecting a future income stream?

The answer is . . . they can’t. Retirees often end up making only short-term, immediate tax-saving decisions, while missing out on more advantageous, long-term tax reduction opportunities because neither they nor their advisor project income streams across a full retirement. Focusing only on the current tax year ends up costing retirees many thousands of dollars because they fail to recognize, and then to organize, their finances to take advantage of long-term opportunities to reduce taxes.

A comprehensive retirement income plan must consider a lifetime tax reduction strategy that focuses on how today’s decisions to withdraw money from the various types of accounts will impact their tax liability years into the future. The Perennial Income Model™ is the ideal tool to help retirees recognize and organize long-term tax-saving opportunities to keep more of their wealth.

Three retirement account tax categories

Before looking at strategies to maximize your lifetime tax savings, you must first understand the categories of retirement accounts and the tax implications of each. How your investments are taxed depends on the type of account in which they are held. There are three categories of accounts to consider:

Tax-deferred retirement accounts

The money in IRAs/401(k)s and a variety of other company-sponsored retirement saving plans are 100% taxable upon withdrawal unless you use the Qualified Charitable Distributions exception (to be explained). Non-IRA annuities can likewise be lumped into this category with the exception that only the interest earned on the non-IRA annuity is taxed upon withdrawal, not the entire value of the annuity.

Tax-free retirement accounts

The funds in Roth IRAs and Roth 401(k)s can be withdrawn tax-free.

Non-retirement accounts (after-tax money)

Investments that are individually owned, jointly owned, or trust owned have their dividends and interest taxed annually. They are also subject to capital gains taxation in years when investments are sold at a profit.

Three strategies to reduce your taxes in retirement

At Peterson Wealth Advisors we use our Perennial Income Model to provide the organizational structure to recognize and benefit from major opportunities to reduce your taxes. Let’s consider three of these tax-saving strategies that can benefit you in retirement:

1. Managing investment income according to tax brackets

Thankfully, your retirement income stream can come from a mix of tax-deferred, tax-free, and non-retirement accounts used in combination to lower your tax liability. Even though income stemming from tax-deferred accounts is 100% taxable, Roth IRA funds can be withdrawn tax-free and money coming from non-retirement accounts hold investment dollars that can oftentimes be withdrawn with limited tax consequences.

The key is to determine which of the above categories of accounts should be tapped for future income needs . . . and when. Tax-efficient income streams that are thoughtfully mapped out at the beginning of a retirement, as we do with the Perennial Income Model, can be extremely effective to help minimize your lifetime tax burden. With advanced planning, you can avoid the costly mistakes of conventional wisdom: paying almost zero tax from retirement date to age 72, then paying high taxes and higher Medicare premiums until death. The Perennial Income Model shows us that it is better to pay minimal taxes from retirement date to age 72, along with how to be able to pay minimal taxes and minimal Medicare premiums from age 72 to death. When you structure your retirement income streams from a variety of tax locations within your portfolios, thoughtfully planned out, you can experience a higher standard of living while still paying very low tax rates.

2. Qualified Charitable Distributions

The most overlooked, least understood, and one of the most profitable tax benefits recognized by forecasting income streams through the Perennial Income Model comes from the use of Qualified Charitable Distributions. A Qualified Charitable Distribution, or a QCD, is a provision of the tax code that allows a withdrawal from an IRA to be tax-free if that withdrawal is paid directly to a qualified charity. Our clientele consists of retired people who regularly donate generous sums to charities. By simply altering the way contributions are made to charity, you can make the same charitable contribution amounts and reduce your taxes at the same time.

The ability to transfer money tax-free from an IRA to a charity has been around for a while, but the doubling of the standard deduction from the 2018 Tax Cuts and Jobs Act, was the catalyst that brought this valuable benefit to the forefront. With larger standard deductions, only 10% of taxpayers itemize deductions. Here is the catch: you only get a tax benefit from making charitable contributions if you itemize your deductions, and with the higher standard deduction, fewer of us will be itemizing. So, a 65-year-old single taxpayer, with no other itemized deductions, could end up contributing up to $13,000 and a 65-year-old couple could end up contributing up to $27,000 to charity and it would not make any difference on their tax returns, or their tax liability, because both generous charitable contribution amounts were lower than the standard deduction. So, they will just end up taking the standard deduction. Another way of saying this is that these charitable donors will not receive a penny’s worth of tax benefit for giving so generously to charity.

Doing a direct transfer of funds to a charity by doing a QCD versus the traditional writing a check to a charity, can restore tax benefits lost to charitable donors. QCDs are only available to people older than age 70 1/2, they are only available when distributions come from IRA accounts, and a maximum of $100,000 of IRA money per person is allowed to be transferred via QCD to charities each year.

3. Roth IRA Conversions

Converting a tax-deferred IRA into a tax-free Roth IRA can be a valuable tool in the quest to reduce taxes during retirement. Unfortunately, few retirees get it right deciding when to do a Roth conversion, deciding how much of their traditional IRA they should convert, or even deciding if they should convert any of their traditional IRAs at all. Without a projection of future income that the Perennial Income Model provides and the subsequent projection of future tax liability, it is virtually impossible to determine whether a Roth IRA conversion is the right course of action. Perhaps the greatest unanticipated benefit that we have observed since creating the Perennial Income Model is its ability to clearly estimate future cash flows and subsequent future tax obligations for our retired clients. Given this information, the decision whether to do a Roth conversion becomes apparent.

As advantageous as Roth IRA conversions can be, they are not free! The price you pay to convert a traditional IRA to a Roth IRA comes in the form of immediate taxation. 100% of the conversion amount is taxable in the year of the conversion. For this reason, investors must carefully weigh whether doing a Roth conversion will improve their bottom line.

Too much of a good thing usually turns a good thing into a bad thing. So, it is with Roth conversions. Excessively converting traditional IRAs into Roth IRAs without fully considering the tax consequences, can cause some investors to pay more tax than they otherwise would if they didn’t do a Roth conversion in the first place. So, it’s important to recognize when, and when not, to do a Roth conversion.

The Perennial Income Model™ as a tax planner

We first designed the Perennial Income Model to provide the structure to reinforce rational decision-making. It started with a focus on helping retirees match their current investments with their future income needs. Now, we see that the Perennial Income Model’s role is much bigger, including providing the benefit of reducing your taxes throughout the entirety of your retirement.

After my last blog, where I described the reasons we are experiencing high inflation this year, you might be asking “What can I do to combat inflation in my own life?” As I consulted with my team members, financial professionals that work with retirees all day every day, we came up with twenty-six inflation-fighting ideas that will help the retiree, or those nearing retirement.

Some of these ideas will have a huge impact, other ideas are less significant but are things that you may not have thought of previously.

I found it interesting that as we compiled our list, it morphed from being merely an inflation-fighting list into a commonsense checklist of things that every retiree should consider going through as a matter of just being financially responsible. Obviously, not every one of the money-saving ideas on our list will apply to your specific situation, but some will.

How to Fight Inflation at Home

We are confident that every one of you will benefit from going through this list in your own situation and that you will end up saving money by implementing the applicable ideas. These savings will be helpful for you to maintain your lifestyle as you are squeezed by inflation. Read on to learn how to combat inflation as an individual.

Combat Inflation with Investing

Investment mistakes early in retirement can be devastating and there are no do-overs. So, I first wanted to remind you of the inflation-fighting capabilities of your investments before we talk about any other inflation-fighting/money-saving ideas.

1. Remember, the price we pay for inflation-beating investments is having to endure temporary periods of volatility. Volatility is not risk, the synonym for volatility is unpredictability and in the short-term, equities are certainly unpredictable. You wouldn’t be human if this year’s stock market hasn’t caused you concern. However, you need to stay the course and not let yourself be frightened out of owning a piece of some of the most profitable corporations the world has ever known. Compound interest has helped you accumulate the nest egg that you now have. Keep the miracle of compound interest alive during retirement by owning equities. Hold on to your equities if keeping up with inflation is your objective.

2. Have a plan. We follow our proprietary Perennial Income Model™ to create an income plan that protects our retirees’ short-term income from stock market downturns while protecting their long-term income from the ravages of inflation. The Perennial Income Model helps to strike the right balance between owning less-volatile types of investments and owning the more-volatile inflation-fighting equities in a portfolio. It matches your current investment allocation with your future income needs. Do yourself a favor and learn how the Perennial Income Model can help you create your retirement income plan. To learn more about the Perennial Income Model, order a free copy of my book, Plan on Living, here.

3. Have faith in the future and follow your plan. We are not facing an investment apocalypse. Market conditions are cyclical, and we will continue to experience good as well as bad economic cycles. A well-thought-out investment and retirement income plan should have built within itself a contingency plan to deal with economic downturns and periods of market turbulence. In fact, your plan should not just help you to navigate volatile markets it should assist you in taking advantage of them. Don’t allow yourself to get derailed from your plan.

Combat Inflation with Income

4. If you haven’t started Social Security yet, consider delaying applying for your own benefit until age 70. Beyond the built-in annual cost of living adjustments of Social Security, your benefit will increase by 8% each year that you delay from your full retirement age until age 70 by simply waiting. Your full retirement age is somewhere between age 66 to 67 depending on your year of birth. Receiving 24%-32% more each month in Social Security benefits for the rest of your life can be a handsome inflation-fighting boost.

5. Go back to work. Statistics show that almost half of all retirees go back to work after two or three years of retirement and they go back to work for reasons beyond satisfying income needs. In other words, they get bored. Work satisfies their need for social interaction and the need to be part of something bigger than themselves. Find a part-time job that is interesting to you for a day or two a week. With a nationwide worker shortage, there are endless opportunities for retirees to find the kind of job they would enjoy with the flexible schedule that they desire. Being engaged in something that interests you, while picking up a couple of bucks to help with inflation can be realized…have fun!

Combat Inflation with Energy

6. Replace light bulbs and fixtures with LED. LED bulbs last longer and use 25% less electricity than outdated light bulbs that you still might be using in your home.

7. If you are regularly away from your house during the day, program your thermostat. Don’t heat or cool an empty house. You can drop your electric and gas bills by as much as 10% by adjusting your home temperature by a few degrees. Open a window in the summer or wear a sweater in the winter to offset the mild changes in temperature.