About the author

Key Takeaways:

-

Most retirees who pay tithing or make other charitable contributions receive no tax benefit because they take the standard deduction instead of itemizing.

-

Qualified Charitable Distributions (QCDs) allow those over age 70.5 to donate directly from an IRA to a charity, making the gift completely tax-free.

-

Using QCDs can save retirees hundreds or even thousands of dollars annually in taxes, making them one of the most effective ways to give charitably in retirement.

As members of The Church of Jesus Christ of Latter-day Saints, we are accustomed to paying tithing and making other charitable offerings. Our motive for these donations is certainly not for the tax benefit. But as wise stewards over the material blessings with which we have been blessed, we should do all we can to make the most of our donations and pay our charitable obligations in the most tax-efficient way possible.

As a financial advisor, I often see retired members of the Church paying more income tax than necessary because they do not understand what a Qualified Charitable Distribution (QCD) is, and how this provision of the tax code could save them hundreds or even thousands of dollars annually in taxes.

A Qualified Charitable Distribution (QCD) is a provision of the tax code that allows a withdrawal from an IRA to be tax-free as long as that withdrawal is transferred directly to a qualified charity such as the Church.

These tax savings are brought about by simply altering the way LDS contributions are made to charity. Unfortunately, QCDs can only be used by persons over age 70.5. But since we will all be at that age sooner than later; it is beneficial to understand how they work so you can plan for your own future and so you can share this information with your fellow Latter-day Saint retirees.

Taxation 101: Understanding the Basics

Before I explain how a QCD might benefit you, let’s first review how we are taxed. Simply put, as you calculate your tax liability, you first add up all your income and then subtract deductions to come up with your taxable amount. We will all get a deduction.

The IRS has a list of itemized deductions such as mortgage interest and charitable contributions that we can subtract from our tax liability. The IRS also has a standard deduction number that we can subtract from the taxes we owe if our itemized deductions do not add up to more than the standard deduction amount. In essence, we are allowed to subtract the greater of our itemized deductions or the standard deduction from our tax liability.

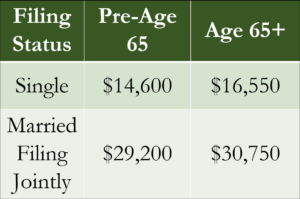

Why is this important to understand? Unless you have itemized deductions in excess of the standard deduction amounts seen in the graphic below, you will not itemize your deductions—you will default to taking the standard deduction.

You only receive a tax deduction for making charitable contributions if you itemize your deductions, and because of the higher standard deduction amounts, only 10% of Americans itemized their deductions last year.

That means that for the 90% of the people who do not itemize and take the standard deduction, there is no tax benefit for paying tithing or making any other type of charitable donation.

By donating via a QCD, you will receive a tax benefit for your donations even if you do not itemize and take the standard deduction.

2024 Standard Deduction Amounts:

Advantages of using a Qualified Charitable Distribution

Making charitable LDS contributions by doing a Qualified Charitable Contribution is a unique tax saving strategy:

- You didn’t have to pay income tax when you earned the money that you put into an IRA or 401K.

- You didn’t pay taxes on the compound interest your IRAs earned over the years.

- Any money paid directly to a charity using a QCD from your IRA will not be taxed.

In running projections with our clients, we have discovered that in almost every instance, those who give to charity and simultaneously make distributions from an IRA can benefit from doing a Qualified Charitable Distribution. We have also found that even those that currently itemize their deductions still benefit from doing a QCD.

We believe that every person over age 70.5, who has an IRA, and who gives to charity should consider making charitable contributions via QCDs. You or your tax professional can run tax comparisons by paying charitable contributions the traditional way versus doing a tax-free transfer from your IRA to a charity using an QCD. Many of you will find the tax savings to be significant.

There are rules, regulations, and instructions on how to report Qualified Charitable Distributions that are too extensive for this article to properly cover but additional information regarding QCDs can be found on our website.

Additionally, examples of how QCDs have benefited retired couples can be found on our website at petersonwealth.com.

You may currently be missing out on a lot of tax savings if you ignore the benefits of the Qualified Charitable Distribution. Saving substantial amounts of money each year by simply altering the way you pay your charitable donations is worth investigating.

Scott is the founder and principal investment advisor of Peterson Wealth Advisors. He graduated from Brigham Young University in 1986 and has since specialized in financial management for retirees. Scott is the author of Maximize Your Retirement Income and Plan on Living: The Retiree’s Guide to Lasting Income & Enduring Wealth.