Alex Call: Let’s go ahead and get started. One of the first questions that we had actually came in a couple of days ago.

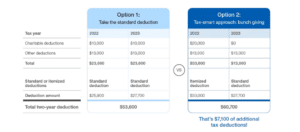

Q: After learning from the last webinar on the Big Beautiful Bill about the increased standard deduction beginning this year, the question came to mind: Is there a limit on charitable contributions as a percentage of income in a given year? I was thinking of grouping my charitable giving this year to allow me to itemize on my 2025 taxes, but can I give over 40% of my income to charity?

It’s a great question. It seems like what it’s really asking is: How much of my income can I deduct if I donate a lot of money to charity? The answer is a little nuanced. Part of it depends on what type of charity you donate to and also what type of asset you donate.

For most people, donating to a private charity, you can deduct up to 60% of your income if you donate cash. If you donate stock or an appreciated asset, it’s 30% of your income. If you end up donating more than that, you’re still able to carry forward that deduction to the following year for up to five years.

Scott Peterson: You mentioned depending on the type of charity. We might want to clarify if it’s a foundation versus a donor-advised fund versus donating directly to the charity. If you use some of these other things, there could be different rules.

Alex Call: For many of our clients, they donate to their church. That would be a public charity, which allows you to deduct up to 60% of your income if the donation is cash, or 30% if it’s stock.

Q:How do you go about calculating an annual required minimum distribution (RMD) from your various 401(k)s or IRAs? And when do the distributions need to begin?

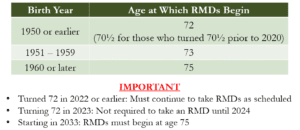

Scott Peterson: For years, the age was 70½, but that has changed.

If you were born prior to 1960, RMDs now begin at age 73.

If you were born in 1960 or later, RMDs begin at age 75.

How do you calculate it? The IRS has a calculator. You plug in your year-end account balance, and it will tell you how much your RMD will have to be the following year.

Alex Call: The formula essentially means that the older you get, the higher the percentage you’re required to withdraw.

Scott Peterson: There’s often a misconception that people have to spend all their IRA money within a short period of time. That’s not the case. At age 80, for example, the RMD is still less than 10%. The required withdrawals start out around 4–5%, then 6%, and step up gradually over time.

Alex Call: We’ll send out the formula for calculating RMDs in a follow-up email, along with a link to the IRS calculator.

Q: Do you have resources to help us choose which Medigap, Part C, or Part D plan to choose?

Yes, we have a chart breaking down Parts C and D and how they work. We’ll go ahead and send that out to everyone to help explain the differences.

Q: Is there a way to set up a scholarship or a tax-deductible way to contribute to my grandchildren’s college?

Scott Peterson: The answer is no — there isn’t a direct tax-deductible way to set up college funding like that. However, for members of the Church of Jesus Christ of Latter-day Saints, there are tax-deductible options for setting aside funds for future missions for your heirs. But not for college.

Alex Call: You may have heard of people setting up scholarships, but that’s a different process. There isn’t a straightforward tax-deductible method to contribute directly to children’s or grandchildren’s college costs.

Technically, you can use a private foundation, but in most cases, it’s going to be more hassle than it’s worth unless you’re truly setting one up with significant funding. Even then, it can’t just go to your grandkids — you have to follow certain rules within that.

Q: Will you review how to get tax advantages from charitable contributions from an investment account?

The best way to do this is by donating appreciated stock or appreciated assets. That’s where you get the most benefit when donating. For example, say you bought Apple stock for $50 and it grew to $200. If you donate that appreciated stock directly to charity, you don’t have to pay capital gains tax on the $150 of growth, and you still get the full deduction for the $200 donation.

Alternatively, if you sold the stock first, you’d have to pay capital gains tax on the $150 gain and wouldn’t get as large of a deduction.

This strategy only works from regular brokerage accounts — not IRAs or 401(k)s. You take the stock that has appreciated the most and donate it directly. That’s the most tax-efficient way to give before age 70½.

Scott Peterson: After age 70½, things change. At that point, you can make donations directly from your IRA. This is called a Qualified Charitable Distribution (QCD). We’ve found that before 70½, donating appreciated stock is best, but after 70½, in almost every instance, making donations directly from your IRA is the better option.

If you regularly contribute to charities and don’t know about QCDs, reach out to us — it’s the most tax-advantaged way to donate after 70½.

Q: How does a 529 plan fit in when helping kids or grandkids pay for college?

Alex Call: Here’s how it works:

Money you put into a 529 is after-tax dollars, so you don’t get a federal deduction up front.

The money grows tax-free inside the plan.

If you use it for qualified education expenses, withdrawals are also tax-free.

This makes it a great way to help kids or grandkids with college costs, especially if you start early to give the money more time to grow.

Each state has its own 529 plan. Some states offer a state tax deduction or credit for contributions. For example, in Utah, you don’t get a federal deduction when you contribute, but you do get a small state tax deduction for contributions to Utah’s 529 plan.

Q: I’ve always planned to wait until 70 to take Social Security. I don’t need the money now, but I keep seeing articles suggesting to take it as soon as possible. I expect a long life. I’m 68. Should I wait or take it now?

Scott Peterson: You should wait. Your Social Security benefit grows by 8% per year for every year you delay, up until age 70. After age 70, the benefit no longer increases.

So, if you’re 68 and wait two more years, your benefit will be 16% higher for the rest of your life. And since you mentioned you don’t need the money now, that makes the case even stronger for waiting until 70.

It’s a whole different answer if you needed the money or if your health was poor. There are other considerations. But since you expect a long life and you don’t need the money now, to me this screams: don’t take it until age 70. Absolutely.

Alex Call: One other thing I’d add is if you’re married, it’s not just your life expectancy you should take into account, but also your spouse’s. If you wait until 70, that will likely be the larger Social Security benefit between the two of you. If you were to pass away first, your spouse would continue to receive that higher benefit.

That’s where it can be really advantageous to wait until 70 — especially if one of you is expected to live a long life. The survivor benefit can really help.

To be clear, when one spouse passes away, the surviving spouse will get the larger of the two checks. That’s why if you don’t need it, and you’re married, by all means, wait.

Q: What is the break-even age if you wait until 70 to start taking Social Security versus taking it at age 67?

Scott Peterson: The answer depends on what inflation rate you plug into the calculation. That will determine the exact break-even age. Getting back to our earlier point: if you need the money to live on, by all means, take it at 67. But if not, waiting until 70 usually makes sense.

Alex Call: As a rule of thumb, the break-even point tends to be around 10 years — give or take a couple of years. So, if you start at age 70, the break-even point is around age 80.

Scott Peterson: Of course, this also depends on inflation and whether your spouse is drawing Social Security based on your earnings, which complicates the calculation. So reach out to us and we can run the numbers more precisely for your situation.

Q:I have a Roth versus a traditional IRA at a 50/50 split. I want to minimize my taxes later, which I believe will likely go up. How can I move to a more tax-efficient future? I’m 55 and would like to retire by 65.

Alex Call: First off, you’ve already done a great job. We call this tax diversification in retirement. You have some money in Roth accounts, which will be tax-free in retirement, and some in traditional accounts, which will be taxable.

It’s hard to give a perfect answer because it depends on several factors. Here are some of the considerations we look at:

Your current tax bracket.

Your expected tax bracket in retirement.

That will probably be the biggest factor. For example, if you’re currently in the 37% tax bracket and expect to be in the 22% bracket in retirement, then it makes sense to contribute as much as possible to your traditional IRA or 401(k) now. You’ll get the 37% tax break today, and then pay only 22% when you withdraw in retirement.

Taxes may go up in the future, but they’re unlikely to rise dramatically for people in the lower or middle tax brackets. Most of the discussion about higher taxes usually applies to high earners making $300,000–$500,000+ per year, rather than those making $100,000–$200,000.

Another consideration: if you’re charitably inclined, it’s helpful to have some money in a traditional IRA. That way, when you reach 70½, you can make Qualified Charitable Distributions (QCDs). This is by far the most tax-efficient way to withdraw from retirement accounts. You donate directly from your IRA to charity, and that money is never taxed.

So, there are a few different moving pieces when it comes to Roth versus traditional balances. If you’d like, we’d be happy to dive into your specific situation in more detail.

Scott Peterson: Sometimes people say, “I don’t want to pay any taxes in retirement. I’m going to convert everything I have over to a Roth IRA.”

The problem with that approach is that when you convert everything, you have to pay tax on the full amount at the time of conversion. People end up paying the full tax bracket rate on their entire balance. Then they retire and, yes, they have zero taxes in retirement — but they probably would have paid almost zero taxes anyway.

That’s why it’s so important to understand your current and future tax brackets before making that decision. Don’t make a knee-jerk move to get rid of all your traditional retirement accounts and move everything to a Roth. You could miss out on future tax-saving opportunities.

For example, Qualified Charitable Distributions (QCDs) are tax-free transfers to charity, which you can only do from traditional IRAs. A Roth conversion, on the other hand, is always a taxable event.

Q:Is there any advantage or disadvantage to investing more in one account versus another? Would my business retirement account — say $850,000 — have a bigger compounding potential if it were spread across two investment accounts, or does it make no difference at all?

Alex Call: The answer: it makes no difference at all. If two accounts are invested in the same way, they’ll grow at the same rate regardless of whether the money is split or not. The account type (401(k), IRA, brokerage, etc.) is just the “bucket” that holds the investments.

What really matters is what you’re invested in, not which account the investments are sitting in.

Q: How do I create a retirement budget when expenses will change during retirement?

Scott Peterson: This is one of the biggest challenges, because most people have never been retired before and don’t know how much they’ll spend.

Here’s a practical way to start:

Review your checkbook and credit card statements from the past year or two to get a baseline of your current spending.

Adjust upward for things you may do more of in retirement, such as travel.

Build a generous budget to ensure you’ve covered lifestyle costs.

Factor in inflation. Over a 30-year retirement, even a 3% inflation rate will cut your purchasing power by about 60%.

This is where our Perennial Income Model™ comes in. It helps plan for inflation-adjusted income across your retirement so you don’t run out of money or lose purchasing power. If you’d like to see how that works, reach out to us.

Q: What is your current thought on the future of Social Security?

We often hear concerns like, “Social Security is going bankrupt, so I need to take it as early as possible.” Some people apply at age 62 out of fear.

We think that’s a mistake. It’s unwise to base your personal Social Security decision on the assumption that the system is going out of business.

Here’s the reality:

Social Security currently has about $2.7 trillion in its trust fund.

As baby boomers retire, that fund is being drawn down.

By 2034, payroll taxes are expected to cover only about 81% of obligations.

That means changes will have to be made — but it does not mean the system will disappear. The challenge is political: whenever solutions are proposed, the other side demonizes them, and nothing gets done.

Still, history shows that Congress has always stepped in with adjustments when needed, and there’s every reason to believe they will again.

If nothing gets done, then by 2032 or 2033 we’ll be in panic mode trying to figure out how to make up for the Social Security shortfall.

If you have any influence with congressmen or senators, encourage them to be brave, reach across the aisle, and act now. Small adjustments today could keep Social Security viable for decades to come.

For example, they could:

Adjust the cost-of-living calculation.

Gradually raise the retirement age for younger workers.

Increase the wage base subject to Social Security tax (currently only income up to about $176,000 is taxed).

These types of tweaks would shore up the system.

For most of us, Social Security will remain intact. Laws may change around the edges, but I wouldn’t make decisions based on the assumption that the system will disappear.

Alex Call: In fact, it’s more likely changes will affect younger generations rather than those currently nearing retirement. For example, raising the retirement age to 70 may apply to workers under 30 today, not those already in their 60s.

Historically, adjustments have happened before. For instance, during the Clinton administration, the full retirement age was raised from 65 to 66 and then to 67. Expect similar gradual adjustments in the future.

Q: If I have all my retirement savings in one fund that targets a retirement year — for example, Vanguard’s Target 2035 — should I diversify more, or is one fund like this enough diversification?

Target date funds have become very popular in 401(k)s over the past 5–10 years, and for good reason: they make investing simple.

A target date fund is a fund of funds. Inside one fund, you get exposure to:

U.S. stocks

International stocks

U.S. bonds

International bonds

This means you are already very well-diversified.

The beauty of a target date fund is that it gradually becomes more conservative as you approach the target year. For example, a 2035 fund will slowly reduce stock exposure and increase bonds as that date nears.

For someone in the accumulation phase (still working and saving), a target date fund is a simple, effective, and diversified solution.

However, once you enter the distribution phase (retirement), it can be helpful to break things up. Having separate conservative and growth buckets allows you to live off the safer money while letting stocks continue to grow.

Scott Peterson: One caution, make sure the target date matches your actual retirement timeline. For example, if you’re 30 years old, a 2035 fund will become too conservative too early. You’d likely want a 2060 or 2065 fund instead. The target year should align with when you plan to retire, not simply be chosen at random.

Q: Should I prioritize paying off my mortgage or saving for retirement?

It depends. Do you already have a lot saved for retirement? Is your mortgage almost paid off? What’s your mortgage interest rate — 3% or 7–8%?

It usually shouldn’t be an all-or-nothing choice. Paying down the mortgage while also saving for retirement can give you the best of both worlds. That way, you benefit from compounding on your investments while working toward being debt-free by the time you retire.

Many clients are glad to enter retirement without a mortgage payment, so it’s a worthy goal. But don’t ignore retirement savings while you’re working toward it.

Q:Should I use taxable investments first and then my 401(k) afterwards?

Don’t automatically assume that’s the best strategy.

Here’s an example: a client followed his broker’s advice to live only off his taxable investments in the early years of retirement, leaving his IRA untouched. He stayed in a very low tax bracket for about 10 years. But by the time he reached age 73, his IRA had ballooned, and now his required minimum distributions (RMDs) push him into the highest tax bracket for the rest of his life.

A better approach may be to take some withdrawals from both taxable accounts and IRAs each year. This balances out taxes over time and avoids being pushed into a much higher bracket later.

These years before RMDs begin can also be an excellent time to do Roth conversions, reducing future RMDs and building up tax-free assets.

The key point is this: in retirement, the goal isn’t to pay the least tax in year one. The goal is to minimize taxes over your entire retirement.

Unfortunately, most CPAs focus only on reducing your taxes in the current year. Retirement planning requires a broader view. A thoughtful, long-term tax strategy makes all the difference.

Conclusion – (38:04)

Alex Call: That about sums it up! If you have any other questions that pop up after reading this, please send us an email. We’re here to help however we can.

And if you’d like us to cover a specific topic in more detail — maybe even in a future webinar — let us know. We want to provide the information that’s most valuable to you.

Alek Johnson: Welcome, everyone. We’re just going to give everyone a minute or two to jump in here. I can see our participants are climbing steadily right now, so we’re just waiting a minute.

This is my favorite time of the year. I’m a big fan of March Madness, so I’m not going to talk too much about how my own team did. Utah State had more of an abysmal performance than I would’ve liked. But for a lot of you jumping on here, I’m sure there are a lot of Cougar fans. BYU is in a good spot right now—hopefully, they can get it done.

I know that I have Jeff Sevy on here with me. I know he’s not rooting for them at all.

Jeff Sevy: Not true.

Alek Johnson: Okay, I think we’re in a pretty good spot, so we’ll go ahead and dive in. There we go—“Go Cougs” is already coming through in the chat.

I’m going to go ahead and share my screen here, and we can get going.

First and foremost, I just want to say thank you very much for taking the time to jump on this webinar with us. As a financial advisor, I love working with couples and individuals one-on-one, getting to know my clients in a more personal way. But I also really love this webinar setting—just the group setting—being able to talk to and present to a large number of people at once.

So thank you for tuning in when I’m sure you have plenty of other things you could be doing at lunch right now.

For those who don’t know me, my name is Alek Johnson. I am a Certified Financial Planner™, one of the lead advisors here at Peterson Wealth.

Before we dive in today, just sticking to the status quo here, we have a couple of quick housekeeping items.

First, just to give you a gauge of timing—this should be a quicker webinar today. I think around 20 to 25 minutes is where we’ll settle in, so a little bit shorter. But hopefully, we’ll still give you some really good information to take with you today.

If you have any questions at all during the presentation, my colleague Jeff Sevy is online with us. He will be helping answer through the Q&A feature located toward the bottom of your screen. Feel free to use that to submit any questions.

I also like to take some time at the end of each of my webinars—three to five minutes or so—to go through any questions that apply to the group. I’m happy to chat and go through those with you.

If you have more of an individualized question, please feel free to either reach out to your advisor if you’re a client with us here at Peterson Wealth, or if you’re not a client, please feel free to just email us or schedule a free consultation. We’re happy to help you in that manner as well.

Last but not least, as always, at the end of the webinar there will be a survey sent out to give me and our team some feedback on future topics. Please, please utilize that—it’s always so helpful. You’ve already given us so much good feedback that we’re trying to incorporate into our future webinars. The more you share, the better for us. So please take the time to fill that out for us today.

Just a quick disclaimer: nothing in this webinar should be taken as investment, tax, or legal advice. It should be used for general purposes only. Obviously, I don’t know what each of your individual situations looks like—that’s why we encourage you to reach out if you have specific questions. But hopefully, you can glean some good value out of today’s topic.

Why Does a Balance Sheet Matter? – (4:03)

As you know, today we are going to be talking about balance sheets. Why are we doing that? Why is a balance sheet important to have?

My background is in accounting, so if you’re like me, sometimes when you hear the term “balance sheet,” you immediately jump to corporate finance. In my undergrad, that’s all I was doing—looking at balance sheets.

Investors use a company’s balance sheet to understand its overall financial health, liquidity, profitability, and a bunch of other aspects to decide if they want to invest in it.

At first glance, it doesn’t really seem like something the average person needs to have. But in reality, a personal balance sheet is one of the most powerful financial tools a retiree can have.

It’s much more than just a list of what you own and what you owe. It’s a financial snapshot at any given point in time that helps you make smarter decisions, reduce your stress, and uncover potential opportunities.

In my opinion, having a balance sheet can really be the difference between kind of drifting through retirement—or confidently being able to navigate it.

To help today’s webinar stick a little better—this is going to be a little cheesy—but I want to take you back to when I was in college at Utah State.

For about a nine or ten-month stint, I worked as a jewelry salesman up in Logan, Utah, at a company called S.E. Needham Jewelers. The picture you see here is with another sales professional we had invited to come in. He gave us some tricks of the trade.

Anyway, I’m happy to report that as young and goofy as I was, I was able to help a lot of happy couples get engaged. It was a good time—but really, that’s not the point of me walking down memory lane with you.

When I was there, we would always take the time to educate couples—or individuals—on what we called the Four Cs of diamonds.

You’re probably familiar with this yourself, right? The four Cs of diamonds: cut, color, clarity, and carat.

We’d pull out the different diamonds, let them look under the magnifier, and talk about the differences between each diamond. The four Cs always seemed to stick with people. When they’d come back, they’d say, “Okay, I thought about it more. I want a better color,” or “I want better clarity,” or “a bigger carat size.”

So today, to help this webinar stick, I’m going to give you what I’ve termed the Three Cs of the Balance Sheet.

The Three Cs are why having a balance sheet should matter to you:

Control

Your balance sheet will help you stay in control of your finances. Most retirees don’t have all their assets in one place. They might have an IRA at Fidelity, a Roth IRA at Schwab, a 401(k) with their previous employer, their home, maybe a second home, and various checking and savings accounts at different banks. Everything ends up scattered.

Now, individually, each of those accounts might seem manageable. But collectively, it can be a lot—especially without a centralized document that shows all your assets and liabilities in one place.

Without that, it’s easy to lose track. You can make uninformed decisions—or assume everything is fine until it isn’t. Control is number one.

Clarity

A personal balance sheet, in my opinion, forces clarity. It gathers everything into one place and says, “Here’s where I stand.” That clarity is a powerful tool and often reveals things you wouldn’t have seen otherwise.

It also allows you to have better conversations—with your spouse, your financial advisor, your children, or other professionals. When everything is visible, clear, and organized, decision-making becomes a lot more straightforward and collaborative—rather than overwhelming.

Confidence

Many retirees don’t actually know how wealthy they are without a balance sheet. A well-structured balance sheet can offer a comforting realization of, “Hey, we’re okay,” when you see that bottom line. On the flip side, it can also be a wake-up call: “Okay, we need to make some adjustments to get to where we want to go.”

Overall, a balance sheet helps you gain confidence—either in where you stand now or in creating a plan to get to where you want to be down the road.

Breaking Down Your Balance Sheet – (9:00)

So those are the Three Cs. Keep that in mind—that’s going to be the main focus of this webinar.

In a few minutes, I want to talk about the benefits of having an updated balance sheet, so you can see what control, clarity, and confidence you can gain from having that document in place.

But first, I want to briefly touch on how you set up and create your balance sheet so we’re all on the same page. Let’s go ahead and break this down.

A personal balance sheet gives you a clear, organized snapshot at a specific point in time. It’s made up of two primary sections:

Assets – what you own.

These are items with value that you could sell, use to produce income, or convert to cash. This is the good stuff—what everyone wants to have.

Liabilities – what you owe.

These are your obligations, debts, or future payments. Together, your assets and liabilities determine your net worth.

Liabilities are not inherently bad, even though they reduce your net worth. We’ll talk more about that in a bit.

Once you’ve listed everything, subtract your total liabilities from your total assets. That result is your net worth.

When you create your balance sheet, your assets should be listed in order of liquidity—from the most accessible (cash) to the least liquid (real estate or personal property like collectibles).

A note on personal property: this section is optional. My general rule of thumb—if it could realistically be sold for over $5,000, consider putting it on. Otherwise, it may just clutter the statement. You don’t need to list your couch or TV. But if you have art or other collectibles worth more than $5,000, definitely consider including them.

A few other tips when listing your assets:

Include the account name

The institution where the account is held

The account type (IRA, Roth IRA, joint, trust, etc.)

And the titling—whether it’s held individually, jointly, or in a trust

Also, make sure to use realistic and current market values—not what you think it’s worth or what you paid for it.

Your liabilities should be listed from short-term to long-term. I also suggest including the creditor name, the interest rate on each liability, and the monthly payments you are making. If you know the payoff date for any liabilities, I would include that as well when you’re creating or updating your balance sheet.

Once both sections are complete, you’re simply going to take your total liabilities, subtract them from your total assets, and that will give you your net worth.

This is your financial scoreboard, so to speak—tying it back to March Madness, right? The scoreboard of your net worth shows what you’ve accumulated and gives you a good baseline you can track over time as you progress through retirement.

Pro Tips for Creating or Updating Your Balance Sheet

Here are some quick, friendly pro tips when you’re updating or creating your balance sheet. A few of these we’ve already touched on, so I won’t spend too much time there.

Update it at least annually.

Set a date—whether it’s the beginning of the year, after you file your taxes, or even your birthday (although that might make for a sad birthday!). The point is: your assets grow, your debts shrink, and things change all the time. So get in the habit of updating it at least once a year.

Be honest and accurate.

Use realistic market values—not what you hope it’s worth or what you paid for it. This is especially true for things like real estate or collectibles. Don’t inflate the value of your assets, even though we tend to have a bias as owners to think they’re worth more. But also don’t deflate them either—get a market value that’s realistic and current.

Don’t include income or expenses.

This is a common point of confusion. Your balance sheet is not your income statement. Both are great tools, but they are different. So when creating your balance sheet, don’t list out your monthly spending or income. This is strictly a snapshot of your assets and liabilities.

Label ownership clearly.

Titling really matters—especially for estate and tax planning implications. Be sure to label whether the asset is held individually, jointly with a spouse, in a trust, etc. And while you’re at it, make sure your beneficiaries are up to date, and that you know who the beneficiary is on each of your accounts.

Benefits of Having an Updated Balance Sheet – (14:50)

Pretty straightforward, right? I assume most of you have created a balance sheet at some point in your life. So for many of you, this is probably more of a refresher than anything new.

Now let’s talk about the benefits of having an updated balance sheet.

I’ve had many great conversations and made strong planning decisions for clients simply because we first reviewed their balance sheet. Having this one document updated and in place can make a big difference. Here are a few key things we’ve discovered from it.

It drives smarter decisions.

First, it brings clarity to your investment decisions.

For example, when reviewing retirees’ balance sheets, I’ve often found they have an improper asset allocation. You might be investing appropriately inside your 401(k) or IRA, and think you’re allocated well. But if you’re also holding a large sum of cash on the side—just because you like a bigger emergency fund—that cash can impact your overall It might make you more conservative than you need or intended to be.

Another common situation: you may be well-invested overall, but not strategically invested across your different accounts.

Let’s say you want to be 60% stocks and 40% bonds in your overall portfolio. Many retirees split that 60/40 ratio evenly across their IRA and Roth IRA. But a potentially smarter strategy would be to invest the Roth IRA more aggressively—to capture market growth 100% tax-free—and keep the IRA more conservative.

So you still maintain the 60/40 balance overall, but now you’re directing more of the growth to a tax-free account, which can significantly benefit your long-term wealth.

It improves cash management.

Many retirees unknowingly hold excess cash spread across multiple bank accounts—checking, savings, etc. These funds often sit idle and earn little to no interest, which creates a huge opportunity cost.

With a balance sheet, it’s easier to identify surplus cash and redirect it to better options—like a high-yield savings account, CDs, a money market fund, or even short-term bond funds.

I’ve seen retirees with hundreds of thousands of dollars in cash earning 001% interest, while high-yield savings accounts were offering 4–5% during that same time. Some banks simply don’t reward savers, and unless you’re paying attention, that lost interest can add up quickly.

Cash management is a huge benefit we find with the balance sheet.

Confidence in Your Debt Strategy

It also helps us have better confidence in our debt strategy.

Often, retirees—and really just people in general—assume that all debt is bad, but that’s not always true. Some debt, like a low-interest mortgage, might be strategically kept as part of your financial plan.

In fact, I’ve recommended holding onto a mortgage instead of paying it off, several times. A balance sheet brings that conversation to the forefront. It allows you to ask questions like:

Is this debt manageable?

Could paying it off improve our cash flow or peace of mind?

What asset would we use to pay off that debt?

Can we incorporate the debt into our retirement plan?

All of these decisions become clearer when you have your balance sheet in place.

Identify Red Flags

Another great benefit of a balance sheet is that it helps you identify red flags.

One of the biggest advantages is that it brings things to the surface—things that may have been hiding in plain sight for years.

For example, you might come across an old 401(k) from a job 20 or 25 years ago that you forgot about. You wouldn’t believe how many clients have come in—some of whom I’ve worked with for years—and said:

“Alek, I got this thing in the mail about my 401(k) from a firm I worked at years ago. Do you know if there’s any money in there?”

And I’m thinking, I didn’t even know that account existed! It’s not necessarily a huge problem, but it can be a missed opportunity if that money isn’t invested properly. Having a balance sheet helps us track that kind of thing.

Another common red flag is mismatched account titling. For example, you may meet with an attorney to create a solid estate plan—establishing a trust and a will—but still have a joint account that should be titled in your trust. Or you might have a brokerage account with no named beneficiaries.

These things can create big headaches later if they’re not cleaned up now. I promise you, your kids will thank you endlessly for doing this now, rather than having to sort it all out after you’ve passed.

And while it’s not as common, we sometimes find lingering debt issues—a credit card balance, or a home equity line of credit with a high interest rate quietly growing in the background.

Knowing what you owe is just as important as knowing what you own. That knowledge gives you the control and confidence to deal with outstanding debt. We’ve caught some really high-interest debts this way—ones clients weren’t even aware of.

Improves Tax and Estate Planning

A balance sheet isn’t just helpful right now—it’s also incredibly useful for future planning. It improves coordination with your CPA, financial advisor, estate attorney, and other professionals by giving them a full financial picture.

From a tax planning standpoint, it helps uncover opportunities. For example:

Are you sitting on appreciated stock in a taxable account that could be donated instead of triggering capital gains?

Do you have a large portion of your savings in pre-tax retirement accounts that could lead to large Required Minimum Distributions (RMDs) down the road?

Having the full picture allows us to evaluate if Roth conversions might be a good strategy to reduce future tax headaches.

These kinds of questions can’t be answered without knowing what’s where and how much is in each account. A balance sheet sets the stage for thoughtful tax planning, rather than reactive tax filing.

When it comes to estate planning, the same applies. Account titling, beneficiary designations, and estate documents all depend on knowing what assets exist and how they’re structured.

With a good balance sheet, we can discuss:

What will pass through the will vs. directly to beneficiaries?

Are all of your assets properly titled in the trust?

Can accounts be consolidated to make things easier on your heirs?

One recent example from another advisor in our office: a client had their mother’s house titled in their own name, which meant they were not going to receive a step-up in basis when their mom passed away. That advisor was able to help retitle the property appropriately.

These details matter, and a balance sheet helps you streamline estate settlement for your loved ones down the road.

Tracking Your Financial Plan Over Time

Perhaps the biggest benefit of a balance sheet is that it helps you track your overall financial plan over time. One of the biggest problems I see when people create a balance sheet is that they do it once, feel accomplished—”We did it! Got it done!”—and then they don’t look at it again for years.

But financial planning isn’t a one-and-done event. It evolves—and it can evolve quickly. Your assets grow. Your spending changes. Your debts get paid off. Your goals shift.

By updating your balance sheet regularly, you can see if you’re building wealth, maintaining it, or starting to spend it down. It helps answer important questions like:

Are we on track?

Is our net worth holding steady?

Have our liabilities been reduced, or is interest still accumulating?

Are we using our money the way we intended?

A balance sheet creates an ongoing conversation rather than a one-time report. That’s the biggest gap I see—people are great at creating it once, but they don’t go back to compare over time.

However, your balance sheet is one of the best indicators of whether your plan is actually working.

Summary – (25:22)

In retirement, it’s not enough to hope your finances are in good shape. You need visibility. You need structure. And you need the ability to make informed decisions as your life continues to change and progress.

A personal balance sheet provides you with just that. It’s not about spreadsheets (even though some of us—myself included—love Excel). It’s about staying in control, getting clarity on your planning decisions, and moving through retirement with confidence.

So I highly recommend making your personal balance sheet a living, breathing part of your financial life. It’s one of the best tools you can have, and I truly believe it will help you be set up for long-term success.

Alright, quick and easy—hopefully I didn’t go too long there.

Before I open it up to questions with Jeff, I just want to mention, hopefully all of you already have a copy of the book Plan on Living by our founder, Scott Peterson. If not, please feel free to request it. It’s completely free, and we’ll get it sent out to you in the next day or two.

If you’d like to share a copy with someone, email us. We can send it directly to them or to you if you’d prefer to deliver it yourself.

Lastly, thanks again for attending today. I know you probably had other things you could be doing here at noon on a Wednesday, but I appreciate you taking the time to join.

And one more plug for the survey—if you wouldn’t mind filling that out, letting us know what you thought and what topics you’d like to hear more about, we’d be grateful!

Question and Answer Session – (27:13)

Okay, Jeff, I’ll turn it over to you. Any questions that we got?

Jeff Sevy: Ya, we have one or two here that would be easy to answer.

Q: Can Peterson Wealth work as a financial planner prior to retirement—like one to two years out?

Alek Johnson: A: The short answer is yes. The longer answer, it really depends on your situation. As fiduciaries, our goal is to put your best interest first. Some people are comfortable managing things on their own up until retirement, which is a major transition from accumulation to distribution. That shift brings a lot of change, and it’s often a great time to link up with a planner. If you’re ready to offload some of the complexity, we’re happy to help.

Jeff Sevy: Q: Should I list CDs as short-term or long-term assets?

Alek Johnson: A: For the most part, list them as short-term. Even though you can get longer terms on CDs, they’re still fairly liquid. If needed, you can access them early with a small interest penalty.

Jeff Sevy: Q: Does it make sense to use investments to pay off my mortgage?

Alek Johnson: A: It depends. Sometimes yes, sometimes no—it depends on what type of accounts you’d be pulling from. If everything is in an IRA or 401(k), paying off the mortgage might trigger a big tax hit. But if you have assets in a brokerage or trust account, it might make more sense. Reach out to us—we’re happy to walk through it with you.

Jeff Sevy: Q: What goes into the decision to pay off a mortgage early or keep it?

Alek Johnson: A: A few key factors come into play, but the biggest is usually your interest rate. This one really depends on your personal situation. If you’re pulling from a 401(k) or IRA, all of that will be taxable. Depending on your tax bracket, that could mean paying 12%, 22%, or more in taxes just to eliminate a mortgage with a 3% interest rate. That’s a tough tradeoff.

Jeff Sevy: Q: How do you determine the actual value of assets?

Alek Johnson: A: For brokerage and retirement accounts, the values are straightforward—just look at your most recent statements. The market value is usually up to date.

For assets like real estate, collectibles, or art, you’ll want to get an appraisal. That small investment up front can go a long way in giving you an accurate sense of what your assets are worth—especially when doing estate planning or calculating net worth.

If you’re unsure what something is worth or whether it’s worth including, feel free to reach out to us and we can help point you in the right direction.

Jeff Sevy: Q: If I already own my home, is there any reason to take out a mortgage before retirement?

Alek Johnson: A: That’s a loaded question. For most people, I’d lean toward no. If your home is paid off, it’s typically best to keep it that way.

But there may be very specific situations where it makes sense—perhaps for liquidity, investment opportunities, or estate planning. That’s something we’d want to discuss one-on-one so we can evaluate your numbers and goals.

Thanks again to everyone who joined us. If you haven’t already, please fill out the post-webinar survey. It helps us improve these sessions and gather ideas for future topics you’d like to see.

We appreciate your time and hope you found this session helpful. Enjoy the rest of your day!

Taxes In Retirement – Welcome to the Webinar (0:00)

Carson Johnson: Good afternoon. Welcome, everyone. Thank you all for joining me.

I’m so excited to be with you on this beautiful, technically still spring, afternoon to talk about the exciting topic of taxes.

I know you probably think I’m crazy for finding this a fun topic, but I actually do enjoy taxes. It’s interesting that when it comes to taxes, retirees always find it a big and important topic.

While we’re waiting for everyone to join, I’d like to quickly introduce myself. My name is Carson Johnson. I’m a Certified Financial Planner™ and one of the lead advisors here at Peterson Wealth Advisors. Joining us virtually today and manning the Q&A and chat is Josh Glenn, one of our Certified Financial Planners™. If you have any questions, feel free to use the Q&A feature at the bottom of your Zoom application, and Josh will get to your questions as they come up.

A couple of housekeeping items: We’ve received a lot of interest in today’s webinar, so I expect the presentation to be about 30 to 40 minutes, with a short Q&A afterwards. For anyone who can’t stay for the entire time, don’t worry. We are recording this webinar, and there will be an email sent out tomorrow with the link to the recording.

At the end of the presentation, there will be a survey. Thank you to those who have been filling these out; it’s super helpful for us to get feedback and improve our presentations. It also helps us understand the topics you want to hear about.

Another quick disclaimer: The information we discuss today is not considered tax, legal, or investment advice. All information discussed is for general informational purposes only. It’s important to remember that everyone’s situation is different, and you should discuss any ideas you glean from our conversation today with a qualified professional or tax advisor.

Let’s go ahead and jump right in. Today, my hope is to cover five main areas regarding taxes in retirement:

How retirement impacts your taxes

The taxation of different types of retirement income

The taxation of different types of investment accounts

What Roth conversions are and when you should consider them

Other tax traps and planning strategies to consider in retirement

How does retirement impact your taxes? (3:10)

First, how does retirement actually impact your taxes? This is a big topic that is usually top of mind for retirees. For some, the impact may not be significant, but for others, it could be. Many studies say that taxes can be one of the largest expenses in retirement, so it’s a topic that shouldn’t be overlooked and should be carefully thought through.

Retirement Income Sources and Tax Implications

One of the major changes upon retirement is where your income comes from. Before retirement, income primarily consists of wages earned from working for an employer. In retirement, income usually comes from various sources, such as social security, pensions, rental income, or income from your portfolio, including IRAs, investment accounts, and Roth IRAs.

These different sources of income can present some challenging tax situations in retirement but also offer important planning opportunities. While all income sources eventually flow through to your tax return, not all are taxed in the same way or at the same rate. Retirees may be able to structure their income to minimize taxes and create a more tax-efficient income stream. However, without careful planning, they could end up with a less tax-efficient income stream or pay unnecessary taxes.

Today, we’ll discuss some of the rules to be aware of. By understanding some basics, you can significantly impact not only your retirement outcome but also how long your assets will last in retirement.

Changes in How Retirees Pay Taxes

Another major change upon retirement is how retirees pay their tax bills. Many retirees are used to having taxes withheld from their paychecks by their employers. In retirement, this responsibility falls squarely on your shoulders. It’s important to understand what taxes retirees are subject to and how they pay them.

Payroll Taxes and Retirement

One tax that goes away upon retirement is the FICA tax, which stands for Federal Insurance Contributions Act. This U.S. federal payroll tax consists of two parts: the Social Security tax, which is 6.2% of your gross wages up to a cap, and the Medicare tax, which is 1.45% of your gross wages with no cap. Upon retirement, you are no longer subject to these taxes because FICA tax pertains only to payroll taxes, leaving many retirees having to pay only federal and state income taxes. We’ll discuss one other category that retirees may be subject to in just a minute.

Also, as a quick note and an important distinction related to payroll taxes and deductions: once you’re retired, you’ll likely no longer be contributing to a 401(k) or an employer HSA, or have other deductions that you might have had during your working years. Even though these additional deductions aren’t taxes per se, they are expenses that will likely go down in retirement.

Methods for Paying Your Tax Bill in Retirement

So, if you’re no longer associated with an employer, how does a retiree pay their tax bill? Ultimately, there are two methods that retirees can use to pay their tax bills.

The first method is called tax withholding. Tax withholding is money that is withheld and sent directly to the IRS or state from one of your retirement income sources. This is similar to the elections you make on your paycheck, where you can specify a specific dollar amount or percentage to go towards taxes. This can be a great way to cover your tax bill, as it is fairly easy to set up and manage.

However, it’s key to be aware that you need to specify a certain dollar amount or percentage, so you’ll have to do some thinking and calculating to determine how much you should be withholding to cover your tax bill at the end of the year. Examples of where tax withholding might apply include pensions, IRA and 401(k) distributions, and Social Security. Note that Social Security only allows federal withholding, not state.

The other method to cover your tax bill is through estimated payments. This method is generally used by self-employed individuals who don’t have the other sources of income listed above. They typically have a non-retirement account and are probably already used to paying taxes this way. With this method, you pay taxes to the IRS throughout the year on a quarterly basis. This method can be more cumbersome than having tax withholding, as you have to send money in either by mailing a check or setting up a direct deposit on the IRS.gov website.

Importance of Timely Tax Payments

As a general suggestion, tax withholding is generally easier to manage. Although this may seem like a small adjustment for many of you, for some retirees it is a big change. You have to think about how much to withhold because some might think they can just wait until the end of the year to pay their taxes and figure it out then. Unfortunately, our tax system works differently; it’s a pay-as-you-go system, meaning it’s important to pay your tax bill in a timely manner throughout the year to avoid underpayment penalties.

These penalties are essentially an interest rate that the IRS charges on the amount you underpaid. Currently, with higher interest rates, this penalty is about 7-8% and can be substantial. The goal of withholding is to withhold enough to avoid underpayment penalties, but not so much that you end up with a big tax refund. A major misconception is that a tax refund is a gift from the government, but it’s actually just a refund of your own dollars that you overpaid. There’s no reason to give the IRS an interest-free loan when you could be using those funds for something else.

Ordinary Income Tax for Retirees

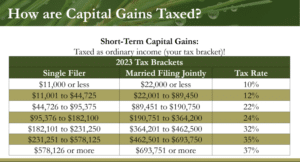

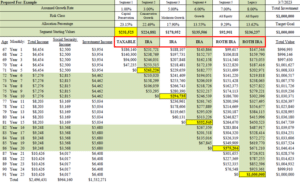

Moving on to the next topic, I want to discuss the two categories of taxes that retirees are generally subject to. The first is taxation on ordinary income. When I refer to ordinary income, I mean income sources such as wages, taxable withdrawals from retirement accounts, taxable Social Security benefits, annuity distributions, pensions, and more.

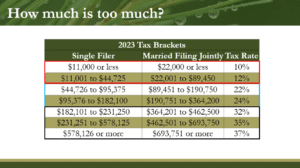

Each of these income sources is taxed as ordinary income, meaning they are taxed based on your tax rate or federal tax brackets. We have the tax brackets for single filers and married filing jointly, showing based on your income what the tax brackets are. Our tax system is progressive, meaning not all of your dollars are taxed at one rate.

For example, if you’re a married couple with a combined ordinary income of $180,000, the first $23,200 is taxed at 10%, the next $71,000 is taxed at 12%, and the remaining portion of that $180,000 is taxed at 22%. It’s important to figure out your tax rate and the average or effective tax rate among these blended rates to make informed decisions. This could be for determining how much to withhold on your pensions and Social Security to cover your tax bill or for making other decisions such as whether to do a Roth conversion or other tax planning strategies.

There are calculators online that you can use to figure out your effective tax rate, or you can work with a CPA or financial advisor who can project this out for you.

Capital Gains Tax in Retirement

Now, the second category of taxes a retiree may pay is called capital gains tax. This tax only applies if you’re selling an investment or an asset in a non-retirement account, or if you’re selling other assets such as a business interest or investment properties other than your primary residence. So, if you only have a 401(k) or an IRA account, this won’t apply to you. However, some retirees do have non-retirement money, and I think it’s important to go over this.

So, what is a capital gain? Simply put, a capital gain is when you sell an asset or property for more than what you originally paid for it. For example, let’s say you buy Apple stock for $50,000, and over time it grows to $120,000. If you then decide to sell it, you would report the difference of $70,000 as capital gains income on your tax return.

Capital gains are taxed at different rates depending on how long you’ve held or owned that investment. There are two categories to be aware of:

Short-term capital gains

These are gains realized on investments or assets sold after holding them for less than a year. The tax rate for short-term capital gains is the same as your ordinary income tax rate.

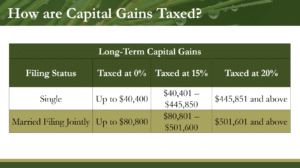

Long-term capital gains

These are gains realized on investments or assets sold after holding them for more than a year. Long-term capital gains are taxed at preferred rates of either 0%, 15%, or 20%, depending on your income level.

It’s important to understand a couple of key rules. First, short-term and long-term capital gains must be reported on your tax return in the year that you sell the investment. Second, capital gains only occur when you sell an investment for a profit. For example, if you hold Apple stock in your brokerage account and it appreciates in value, you won’t pay taxes on that growth until you actually sell the investment.

Short-term capital gains are taxed at your ordinary income tax rate. So, wherever you fall in the tax brackets we discussed earlier, that rate will apply to your short-term capital gains. Long-term capital gains, on the other hand, get preferred treatment and are taxed at lower rates.

Tax Strategies for Short-Term and Long-Term Gains

A common issue with short-term capital gains is that some retirees or investors may own investments that generate significant short-term gains, leading to higher taxes. For instance, mutual funds managed by fund managers who buy and sell investments frequently can result in substantial short-term capital gains being passed down to shareholders, causing unnecessary tax burdens.

One strategy to mitigate this is to be cautious of mutual funds and other investments that generate short-term capital gains. Holding investments long enough to qualify for long-term capital gains rates can significantly reduce your tax liability.

Understanding Tax Loss Harvesting

Another related tax strategy is tax loss harvesting, which can be very beneficial. Tax loss harvesting allows you to sell an investment in a non-retirement account at a loss and use that loss to offset other taxable income on your tax return.

For example, let’s say you bought Apple stock for $50,000, and the stock market drops, reducing the value to $40,000. You could sell the stock, report the $10,000 loss, and use that loss to offset other capital gains or income, potentially reducing your overall tax bill.

Some might think that selling an investment at a loss is not a good idea, which is true to an extent. However, the goal of tax loss harvesting is to strategically use losses to your advantage by offsetting gains or income and lowering your tax liability. This strategy can be especially useful in volatile markets where some investments may experience temporary declines.

Reinvesting After Tax Loss Harvesting

Remember, the key to successful tax planning in retirement is understanding how different types of income are taxed and using strategies like tax loss harvesting to manage your tax liability effectively.

So the other part of tax loss harvesting is not to just stay out of the market, but to take those proceeds from what you just sold and reinvest them into another investment. In this case, I mentioned Johnson & Johnson as an example. This is not a recommendation, but just to illustrate the point.

The reason for this strategy is that once you sell the investment and immediately reinvest, you can stay invested and benefit when the market bounces back and recovers. This allows you to take advantage of the losses while still staying invested over that period of time.

Now, an important rule to be aware of with this strategy is that whatever investment you’re buying back has to be substantially different from what you just sold. You can’t simply sell Apple stock at a loss and then buy back Apple stock later. This is due to a rule called the wash sale rule, where the IRS may not allow you to take advantage of those losses if you do that. So, whatever you’re buying back has to be substantially different, but it can still be a great way to reduce taxes and other income that you report on your return.

Taxation of Social Security Benefits

Now let’s move on and talk about the taxation of Social Security—another big-ticket item that a lot of people have questions about. In many instances, more money can be saved by minimizing tax on Social Security than strategizing on when you should claim your Social Security benefits. This is not to say that you shouldn’t do your homework and run some analysis on whether you should claim now, at age 67, or at age 70, but the focus today should be more on how you can minimize tax on your Social Security benefits themselves.

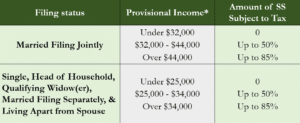

I won’t go into all the nitty-gritty details of the taxation of Social Security, but the IRS has a formula that states the more money you make outside of your Social Security benefits, the more your Social Security benefits will be taxed. For example, let’s say you’re married filing jointly and your provisional income—which is your combined income plus half of your Social Security benefit and tax-exempt interest—is under $32,000. In that case, none of your Social Security will be subject to tax. If your provisional income is between $32,000 and $44,000, then up to 50% of your Social Security will be subject to tax. If your provisional income is over $44,000, then up to 85% of your Social Security is taxable. I’ve also listed the single-filer version of income as well.

A couple of key takeaways here: First and foremost, not all of your Social Security benefit is taxable, unlike other sources of income such as pensions or IRA withdrawals where 100% of those distributions are generally fully taxable. This can be a consideration as you’re creating your income stream. Another point to note is that the way to reduce tax on Social Security is to reduce other sources of taxable income.

Strategies to Minimize Taxes on Social Security

I want to give you a couple of examples of how you can minimize taxes on Social Security benefits. First is to reduce other income with tax-advantaged investments. If you’re generating a lot of interest, for example, in a bank account or investment account, you may want to consider investing in higher interest-earning investments in an IRA where you’re not taxed on the interest you earn, only on the withdrawals. This can help you avoid taxes on Social Security benefits.

Sometimes people think you should invest in municipal bonds, but remember from the formula, tax-exempt interest from municipal bonds is also included, so you can’t avoid that with municipal bonds.

The second way is to anticipate your Required Minimum Distributions (RMDs). If you have an IRA or 401(k), at some point you’ll be required to withdraw a certain amount of money from those accounts, which is currently at age 73. If not properly planned for, RMDs can turn into a big tax nightmare later on, pushing you into higher tax brackets or impacting other aspects of your retirement.

The third strategy is to delay Social Security. By reducing the number of years your benefits are subject to tax, you can ultimately reduce the overall amount of taxes paid. Delaying Social Security might also give you more time to implement other tax strategies like Roth conversions, tax loss harvesting, or others.

Lastly, consider doing a Qualified Charitable Distribution (QCD). We’ve discussed this in past webinars, but it’s worth mentioning again. A QCD allows you to withdraw money from an IRA tax-free as long as it goes to a qualified charity. If you regularly give to charities or churches, this can be one of the best ways to reduce the amount of tax you pay on your Social Security benefits. You have to be at least age 70½ to do this, but it can be a great strategy to consider later on.

Taxation of different account types (25:11)

Now moving on to the next area of taxes in retirement: understanding the taxation of different account types.

So before you can begin creating a tax-efficient stream of income, you need to understand the basics of how your investment accounts are taxed.

Broadly speaking, there are three types of accounts, each with its own unique tax advantages:

Tax-Deferred Accounts: These include accounts like 401(k)s, traditional IRAs, and similar. Contributions to these accounts are made pre-tax, meaning you get a tax benefit by reducing your taxable income in the year you make those contributions. Once you make those contributions, you can invest those dollars, and the investments grow tax-deferred. This means you’re not taxed on any gains, interest, or dividends earned while the money is within the account. However, you will eventually be taxed on those dollars, especially when you start taking Required Minimum Distributions (RMDs). Withdrawals from these accounts are 100% subject to income tax.

Tax-Free Accounts: These include Roth 401(k)s and Roth IRAs. Contributions to these accounts are made with after-tax dollars, so you don’t get a tax benefit in the year you make those contributions. However, the investments in these accounts grow tax-deferred, and if you meet certain conditions, withdrawals from these accounts can be completely tax-free. The conditions typically include being over 59½ and having held the Roth IRA for at least five years.

Taxable Accounts: These include bank accounts, high-yield savings accounts, and investment accounts at institutions like Fidelity or Charles Schwab. These accounts are funded with after-tax dollars and provide flexibility since you don’t have to wait until age 59½ to withdraw funds. However, you pay taxes on dividends, interest, and any gains from selling investments for a profit in the year they are earned.

Generally speaking, because taxable accounts are funded with after-tax dollars and you’re only paying taxes on the growth, these accounts, along with tax-free accounts, are generally more tax-efficient. However, it’s important to remember that no single account type is inherently better than another. It takes careful consideration to determine which accounts you should contribute to and how much you should contribute.

Every person’s situation is different with their pensions, Social Security, and investments, so it requires individual analysis to determine the best contribution strategy. As general advice, it can be beneficial to have a mix of all these account types to provide flexibility and tax diversification, allowing you to structure your retirement income in the most tax-efficient way.

It’s important to remember that a retiree can’t and often won’t make good decisions about reducing taxes in retirement without first mapping out and projecting what their future retirement income will look like. Towards the end, we’ll go over a case study of how we do this with our Perennial Income Model™, our proprietary way of handling retirement income. But before that, let’s hit on a few other important items.

What are Roth conversions and when should I consider them? (29:40)

Next, let’s move on to Roth conversions. What are Roth conversions, and when should you consider them? This is another big question that comes up regarding taxes in retirement. You hear about Roth conversions in the news and media, and sometimes retirees get carried away with this strategy. So, it’s important to understand the basics and why we do them.

As we discussed before, virtually all retirement accounts are classified into one of two categories: pre-tax money (like IRAs and 401(k)s) or post-tax money (like Roth IRAs and Roth 401(k)s). For most retirees, it’s common to have retirement accounts that are pre-tax dollars. A Roth conversion allows you to take pre-tax money and convert it to an after-tax account like a Roth IRA or Roth 401(k). Keep in mind that pre-tax means you haven’t paid any taxes on that money, so whatever amount you choose to convert becomes taxable to you in the year of the conversion.

Because of this, it’s uncommon to convert an entire IRA or 401(k) to a Roth account all at once, as it would create an unnecessarily large tax bill. The advice we give is to convert enough to gain the future benefits of the Roth account but not so much that it pushes you into a higher tax bracket. This involves some projections, whether on your own with online calculators or with the help of an advisor or CPA. You need to project what your retirement income will look like and what your tax rate will be today versus later.

Ultimately, the decision boils down to whether you want to pay taxes at today’s rate or wait and potentially pay at a lower rate in retirement. This is why understanding and projecting your future retirement income and tax rates is crucial.

Converting Pre-Tax to After-Tax Accounts

Now, I want to leave you with three last considerations when thinking about Roth conversions:

First and foremost, consider where you will live in retirement. This might seem like an odd consideration, but some states partially or entirely exclude certain retirement incomes, such as distributions from an IRA or Roth conversions. Some states may not have any state income tax at all. If you plan to move to one of these states, you might want to wait to do Roth conversions until then. Alternatively, if you currently live in a state with no state income tax, like Texas, Florida, or Nevada, you might want to consider doing more Roth conversions now to avoid state taxes if you later move to a state with income tax.

Location and State Tax Considerations

The second consideration is to identify who will benefit from the Roth conversion. If the goal is to create a tax-efficient stream of income for yourself, focus on your specific situation, tax rates, and how the conversion will affect you. If the goal is to leave money to heirs or if your spouse is likely to outlive you, think about how Roth conversions can benefit them. This context will help guide your decisions.

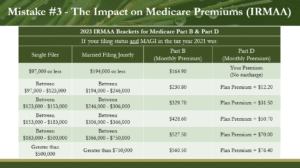

Lastly, while we’ve discussed tax rates extensively, it’s also important to consider how Roth conversions can impact other aspects of your retirement plan, such as Medicare premiums, which is commonly overlooked.

Many people don’t realize that Medicare is not free; there is a premium that you must pay. Moreover, Medicare premiums are based on your income. The more income you report, the higher your premiums will be. Medicare looks at your income from two years prior. For example, your 2024 Medicare premiums are based on your 2022 income. The thresholds work like tax brackets, where higher income can move you into a higher IRMAA (Income-Related Monthly Adjustment Amount) bracket, resulting in surcharges.

Everyone pays a base level premium for Part B, which is $174.70 per person per month. However, this can increase depending on your total combined income. Excessive Roth conversions can push your income higher and thus increase your Medicare premiums.

If you’re just getting onto Medicare and were in your highest earning years two years ago, it might feel punitive to pay higher premiums. Remember, it adjusts yearly based on your income from two years prior. However, Medicare recognizes life-changing events that might reduce your income, such as marriage, divorce, death of a spouse, or work stoppage. You can request relief from Medicare by filling out form SSA-44 if you expect your future income to be lower.

For example, I had a client who was a retired Delta pilot with high earnings nearing a million dollars. When he retired, Medicare sent a letter indicating his premiums would be in the highest IRMAA bracket, about $1,200 per month for him and his wife. We filled out form SSA-44, estimated their future income, and submitted it to Medicare. They accepted it, and it saved him hundreds of dollars per month, amounting to a few thousand dollars by the end of the year, simply by being aware of this rule. So, be aware of it; it can be a huge tax-saving opportunity.

Case Study: Structuring Retirement Income

We’ve covered a lot of strategies here. I know we’re coming up on the hour, so I want to wrap up with a case study to illustrate how you can properly structure your retirement income.

So, for those who aren’t familiar with this plan on the screen, this is an example of our retirement income plan, which we call our Perennial Income Model. I won’t go through all the details of how it works, but if you want to learn more, there is a video on our website that you can watch for a detailed explanation.

Ultimately, this plan matches your current investments with your future income needs. For example, when you take your investment portfolio, we spread it across different segments, each representing five years of retirement income.

Let’s say we have a married couple with a million-dollar portfolio, which is split across three different accounts: a taxable brokerage account, an IRA, and a Roth IRA. The income generated from these investments per month, plus their Social Security, equals their total monthly income.

By running this plan, we can project what their future retirement income will be and what their tax rate will be in retirement. A common question is, “Where should I be drawing my income from?” In this particular case, the clients are 67 years old, and most of their portfolio is in an IRA, which would push them into higher tax brackets once they are required to withdraw money at age 73.

So, we may want to do some Roth conversions in the early years. We decided to live on the taxable brokerage account for the first five years. This account has very low taxes, providing more flexibility to do Roth conversions, which will be taxable.

Then, we decided to use IRA money for segments two, three, and four because, at age 73, they’ll be required to withdraw money due to Required Minimum Distributions. They can also take advantage of qualified charitable distributions, withdrawing money tax-free from IRA accounts as long as it goes to a qualified charity.

Lastly, we chose to use Roth IRA accounts towards the end of the plan to maximize tax-free growth for 20 to 25 years. This can benefit the client if they live longer than expected or if they need funds for long-term care.

You can see that this plan can be adjusted in many ways. For instance, you could draw part of your income from the IRA and part from the taxable brokerage account and Roth IRA throughout your retirement to stay in a low tax bracket. It requires some thought on how to organize your accounts and understanding the taxation of your retirement income sources.

To summarize, tax planning is incredibly important for retirees at all stages of life. However, ages 55 to 73 are crucial for planning. There are major milestones during this period, such as claiming Social Security, Medicare premiums, accessing retirement accounts, and Qualified Charitable Distributions.

Take advantage of these planning opportunities to create a tax-efficient stream of income.

Here are five key insights to remember:

Retirement may change the way you manage your tax liability.

Understand how your investment accounts are taxed and organize your retirement income plan in a tax-efficient way.

The amount of your Social Security that is taxable is based on your combined income.

Roth conversions can minimize taxes in retirement with proper planning.

Be aware of retirement tax traps that might impact other aspects of your retirement, such as Medicare premiums and short-term capital gains.

Question and Answer (42:45)

That’s it for today. Thank you for bearing with me. I apologize for going a bit longer. We’ll now leave the next few minutes for any questions you may have. If we don’t get to your questions today, please send us an email. We would love to address them.

Let’s see if we have any questions. One question is, “If I’m still working and my spouse retires, can I keep my spouse on the work health plan, or is it mandatory to go to Medicare?”

You do want to make sure that once your spouse turns 65, they apply for Medicare Part A to get that started. However, it is not mandatory for them to go on Medicare if they can stay on your work health plan. You can still have your spouse be covered by your work plan if you want to if it’s more cost-effective that way. Good question there.

Is the Medicare premium a monthly premium?

Yes, it is a monthly premium.

What happens when you sell stocks at a loss?

What’s the maximum you can claim on losses? Good question. You can actually harvest an unlimited amount of losses, but the way you use those losses works a little differently. You can offset as much capital gains as you have with as many losses as you have. However, if you don’t have any capital gains to offset those losses, you’re limited to offsetting $3,000 of ordinary income, such as Social Security or IRA distributions.

Is there a date when the RMD will change to 75 years old?

Yes, in 2033, the RMD age will move to 75.

If your spouse is a retired military member and can go on TRICARE at age 60, how does that impact Medicare? Vicki, please send us an email about that. There are a few things to consider, not just the cost of Medicare and TRICARE, but also ensuring you apply at the right time and that it’s considered coverage for Medicare purposes.

Don’t you have to sign up for Medicare at age 65, or do you lose benefits?

You don’t necessarily lose benefits, but if you don’t sign up at the appropriate time at age 65, your Medicare Part B and D premiums could be penalized. That’s why it’s important to be covered by your employer’s health insurance plan or sign up for Medicare at age 65.

What is the current range for Medicaid premiums?

If we’re talking about Medicare premiums, the range depends on your income. Whatever you show on your tax return will determine your Medicare premiums. Medicare premiums do adjust for inflation, so the base amount of $174.70 will adjust over time.

How is the sale of my primary residence treated for capital gains?

There’s an important rule for primary residences. If it’s your primary residence, you can exclude part of the capital gain. I believe it’s $250,000 if you’re a single filer, and $500,000 if you’re married filing jointly. For example, if you bought the house for $100,000 and it’s now worth $1 million, you would have $900,000 of capital gains. Since it’s your primary residence, you can exclude $500,000 if you’re married or $250,000 if you’re single. It works differently for your primary residence.

We’ll take one last question here, and then we’ll wrap up.

Can you provide additional information and rules on QCD, the Qualified Charitable Distribution?

You can withdraw money tax-free from an IRA account as long as it goes to a qualified charity. A couple of rules to be aware of: you have to wait until you’re exactly 70 and a half years old before you can begin using that strategy. You would work with your IRA provider, like Fidelity or Schwab, to fill out a form that allows you to do that. The other important rule is you can’t do a QCD from a 401k account; it must be from an IRA account. There is also a maximum of $100,000 that you can do, but we don’t often see people reach that maximum.

One last question related to the residence:

If it’s a secondary residence, how does it work for capital gains?

Generally, you can only elect one primary residence. If it’s a secondary home, it’s probably not your primary residence, so you don’t get that exclusion. Look into it a bit closer; there may be ways to apply for both depending on how long you’ve lived in each of those homes.

Thank you, everybody. Great questions. Thank you for participating. Again, there will be a survey, please fill that out. Thank you all for joining me, and I hope you have a great week. Thanks.

Navigating Retirement Planning: Why Your Retirement Portfolio Needs Stocks – Welcome to the Webinar (0:00)

Alek Johnson: Welcome, everyone. We’re just going to give it a minute here for everyone to get filed in. We had quite a few participants sign up, so we’re just going to give it a minute or two while everyone files in.

Daniel, while we’re waiting, do you have any good Easter plans coming up?

Daniel Ruske: Oh, we do. My wife’s cousins from Canada are coming down for Easter. They have the spring break off, so we’ll be showing them around Utah. We might go down to Manti and check out that open house. We might—my in-laws are heating up the pool, so at least we’ll get in the hot tub. Depending on the weather, we might get in the pool as well. What are you doing?

Alek Johnson: Oh, I’m just—we’re just pretty much hanging out at home. Easter egg hunt, all the good stuff. So nothing too crazy, but great.

Daniel Ruske: You wanna get this started a minute after maybe?