Presenter

Presenter

Executive Summary

With The SECURE Act 2.0 being passed, Alex Call and Carson Johnson provide updates on what changes will impact you for retirement. These updates include Required Minimum Distributions, Qualified Charitable Distributions, and other aspects of retirement. Follow along with the transcript below.

How The SECURE Act 2.0 Impacts Your Retirement

Alex Call: Thank you everybody for attending. We’re really looking forward to going over this with everybody. My name is Alex. I am a financial advisor here at Peterson Wealth. And Carson is also a financial advisor, and he will be helping us present.

So, before we jump in, we will be having a Q&A at the end. So, any questions that you have just feel free to put them in the chat or in the question part. And we do have Daniel and Josh manning those questions. So they’ll be able to help answer any of those, and any that they don’t get to, we will be answering in the webinar. And then also we will get back to you with an email or a phone call to make sure that all the questions are answered.

So with that being said, let’s just go ahead and jump right in.

What is The SECURE Act 2.0? (1:02)

So what I want to talk about first is really what is The SECURE Act 2.0. And so really it was part of the consolidated appropriation act of 2023, which was just a really big 1.7 trillion bill that was passed right at the end of the year. And this was a small part of that. And what it stands for, SECURE is for Setting Every Community Up for Retirement. And then the 2.0 part is because this is an extension of The SECURE Act that was passed in 2019.

And what’s the purpose of this act? I really think of it as there’s two purposes. One is encouragement. It’s to encourage people to contribute to their retirement plans. And along with that is access. It’s giving people greater access to retirement plans. And so it’s easier for them to make contributions and save for retirement.

~ Time to fix screen ~

So the purpose is encouragement and access. And so then the next thing is, what are we going to cover today? And so what I will tell you what we are not going to cover is that within this act there are hundreds of minor changes to retirement plans that have happened. Things that are not really going to affect anybody here and that will just be gradually implemented and changed to retirement plans over the upcoming years. We don’t want to talk about that.

What we want to cover are what we feel are really the five most impactful changes for current and soon-to-be retirees. And that’s going to be a combination of retirement catch-up contribution limits, QCDs, RMDs, Required Minimum Distributions. And we’ll go through all of these today.

Transferring a 529 Plan to a Roth IRA (3:37)

But the one that I want to go over first is one that has probably been receiving a little too much attention within the financial media that I have seen at least for what it actually is. And the reason why is because in theory, this sounds awesome.

And that has been able to transfer a 529 plan. And a 529 plan is an education savings account that you can contribute. It’s essentially a vehicle to help you save for college, for kids, grandkids, and so forth. And that you’re able to transfer that into a Roth IRA. It sounds awesome. But there’s a lot of rules and restrictions around it. And so, these rules are first, that the IRA receiving the funds, it must be in the name of the beneficiary of the 529 plan.

The next, the 529 plan, it must have been maintained for 15 years or longer. Meaning it has to have been opened for at least 15 years before you can make those transfers into a Roth IRA. Any contributions to the 529 plan within the last five years are ineligible to be moved to a Roth IRA. And then for the other ones, there’s a maximum lifetime limit of $35,000 that can be moved into an individual’s Roth IRA. There’s also an annual limit. And this annual limit is the contribution limit, that for a Roth IRA, just the normal contribution, limit less any regular contributions that have been made.

For example, today the Roth IRA contribution limit is $6,500. So, if I were to contribute if I were doing this for myself, and were to contribute $3,000 as regular contributions, then the most I could transfer from a 529 plan to a Roth IRA is $3,500. So the most combined is that $6,500 amount.

And then next, the Roth IRA earner, or owner, must have earned income the year of the transfer. Meaning if you’re retired, you’re not going to be able to transfer money from a 529 plan into your Roth IRA because you don’t have earned income because you’re not working anymore.

When and How to Use the 529 to Roth IRA Transfer Option

So those are the six rules. Now if we look at when can we use these, what’s a good time to use these and how does this actually be applicable?

So, the first one is what the intended purpose of it is. And that is for allowing money that was earmarked for educational purposes to be repurposed as retirement savings in the event those funds are not needed for education after all. So, you save money for your child’s education. They don’t use all of their money in their 529 plan whether it maybe they got scholarships, maybe they didn’t go to college, something like that. Now you can repurpose those funds into your Roth IRA, and that’s the intended purpose. But there’s another strategy that could be used for, what I think of it as Legacy Planning.

And essentially what this is, it is giving you the ability to help fund your grandkid’s retirement. And how this would work is the time a child is born, say a grandchild is born, you make a meaningful contribution to a 529 plan for their benefit. And then later, you know 15 years later, the child turns 15, 16 years old, and the account funds in the 529 plan could begin to be moved to a Roth IRA for the child’s benefit. Again, following all of those rules and the amount to the maximum IRA contribution each year and so forth.

And so with proper planning and continued annual transfers, until that $ 35,000 lifetime transfer limit is reached, this child’s, your grandkid’s Roth IRA when they turned 65, that could easily approach about roughly a million dollars. And so, it’s giving you the opportunity to really pre-fund your grandkid’s retirement. Those what I would say would be the two main purposes or strategies to be able to use this for.

So the next thing we want to talk about that Carson will dive into is Required Minimum Distributions.

Required Minimum Distribution Age Changes (8:48)

Carson Johnson: Thank you, Alex. So I’m excited to be here with everybody to talk about these important changes as it pertains to retirement. And specifically, Required Minimum Distributions is probably what many of you have already heard about that was going to change. And so there’s actually two main things about the RMDs that I wanted to talk about.

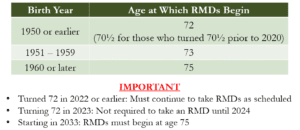

So first, the biggest change to Required Minimum Distributions is that the age at which you begin Required Minimum Distributions is being pushed back. So to make it a little easier for everybody, I created a table that summarizes those changes that were included in The SECURE Act 2.0.

So for those that were born in 1950 or earlier or those who have already started Required Minimum Distributions, because they reached the age 72, the old RMD age, their age will be age 72. Their Required Minimum Distributions will continue on. SECURE Act 2.0 did not impact those that were already taking Required Minimum Distributions. Those that are born between 1951 and 1959 will begin taking Required Minimum Distributions at age 73. And those born in 1960 or later will start Required Minimum Distributions at age 75.

Now, this is pretty simple, but I want to make a couple of important points here. First, like I mentioned, those who have already turned 72 in 2022 or earlier will continue to take their RMDs as planned. The SECURE Act does not impact those. Those turning 72 in this year will not be required to take their RMDs until 2024. So that they won’t have to take that until they’re age 73. And lastly, those starting in 2033, all Required Minimum Distributions will begin at age 75. So, some really important changes there. It’s a phased-in RMD change.

Now, how does this impact retirement? How does it impact those that are preparing for retirement? There is just a few points I want to make here on this. First, those that are planning on and living on all the Required Minimum Distribution or all of their IRA income, will have a very little impact with this. They’re living off of all the Required Minimum Distribution whether they take that, whether their RMD starts at 72 or 75, they’re going to be living on all of it. It’s going to have very little impact to them.

The RMD age change did not impact Qualified Charitable Distributions, the age at which you can begin that. It’s the tax strategy where you can pull money out of your IRA retirement accounts tax-free, as long as it goes to a qualified charity. That still can continue at age 70 and a half. So, the RMD changes did not impact that.

Ultimately, the biggest thing that this does is that it gives you more time for planning. Particularly, the one strategy in mind that this could be very beneficial is doing Roth conversions where you’re taking money out of your IRA, converting it into a Roth IRA so that it’s now tax-free, and can grow tax-free. And I can see this being beneficial because those that are actively doing these Roth conversions and instead of, you know, having to do conversions until age 72 or 73 may now have more years, a few more years to age 75 or 73, depending on your situation, to do these additional conversions. And that way you can take advantage of those lower tax brackets and better planning there.

Surviving Spouse – Required Minimum Distributions (12:36)

The next big change related to Required Minimum Distributions is it impacts surviving spouses. So before The SECURE Act 2.0, generally surviving spouses, so if a spouse has passed away, the surviving spouse would take their IRA account as their own. And once they start Required Minimum Distributions, it would be based on their age. With The SECURE Act 2.0, you still have that option where you can take your IRA and your deceased spouse’s IRA and roll it over into your own IRA and take RMDs based on your age.

But you also have the option, the surviving spouse, to take Required Minimum Distributions based on your deceased spouse’s age. And so you’re probably thinking, why is that important? It’s mainly important for those that apply where the deceased spouse here is much younger than you. Think about it this way. If your deceased spouse is 65 and you are at RMD age at 73 let’s say, you have the ability to rather than taking your RMD right away because you’ve reached your Required Minimum Distribution age. You may be able to delay that until your deceased spouse would have started Required Minimum Distributions and therefore give you more time again for Roth conversions, or any other tax, or financial planning strategies that you’re working on.

And so, this is a small change, but I think it does make a big impact when it comes to planning. So that’s the two major changes related to the Required Minimum Distributions. I’ll let Alex take over here and talk about how Qualified Charitable Distributions have slightly changed.

Qualified Charitable Distribution Changes (14:24)

Alex Call: So Qualified Charitable Distributions as many of you know, it’s one of our favorite tax planning strategies. As Carson highlighted, it’s the ability to put money, it’s a tax-free transfer, from your IRA to a qualified charity. The big thing here is that there’s really only one change that has happened, and it’s for the better. The annual amount that you can contribute as a QCD is now going to increase with inflation starting in 2024. So, before it capped out at $100,000 and now that will be inflation adjusted.

And so what this means is that we can still do QCDs at age 70 and a half. They still satisfy your Required Minimum Distribution. You’re still only able to do it out of an IRA. You’re not able to do QCDs out of a 401k. And probably most importantly is that it doesn’t look like this strategy is going anywhere. They’ve just improved it and made it better.

Catch-Up Contributions in 401k or IRA (15:38)

The next thing I want to talk about are catch-up contributions. So catch-up contributions are when you turn 50 years old, you are able to contribute more to your 401k, or IRA, or retirement plan. Allowing you to catch up your retirement contributions.

And so, there’s really three main changes that have happened here. The first one is that it is now with your IRA, it is that the catch-up amount for your IRA has been stuck at $1,000 for about the past 10 years. Well, now that $1,000 is going to be inflation adjusted.

The next is there’s going to be an extra catch-up contribution for people between the ages of 60 and 63. The amount on this, we’re not quite sure on. The language used in The Act, it’s a little confusing. And so, we are still waiting for Congress to share some additional information or some clarity on that. But just know that when you turn 60 to 63, you’ll be able to contribute an extra catch-up during that time.

The last one is what I call “rothification” of these catch-up contributions. And what that means is, if you are making over $145,000, then any catch-up contribution to your 401k has to go into a Roth 401k. You’re not able to make a contribution to a traditional 401k.

And so you may be thinking, well what happens if my plan does not offer a Roth if there is no Roth option within my plan? Well, unfortunately, you’re not able to make catch-up contributions if that’s the case. With that said though, a lot of these minor changes that we talked about earlier in The Act go towards making Roth plans more accessible and encouraging more people to set up Roth plans.

So what I would expect and really assume is many if not all 40lks, simple IRAs, and so forth moving forward, will have Roth options. It might take a year or two for the plans to implement, but I would assume that most if not all of them will begin to have Roth options as well.

And now I’m going to turn it over to Carson just so he can highlight a couple of things that were not covered in the plan or in The Act.

What was not covered in The SECURE Act 2.0 (18:36)

Carson Johnson: Thank you, Alex. So when it comes to legislation that’s passed like this. A lot of times many retirees and many, many people are concerned about current tax or financial planning strategies going away or being limited. And so we thought this would be helpful to include a few items that were not impacted, not changed by The SECURE Act 2.0.

The first of which was the elimination or restricting of Roth IRAs or Roth 401ks, that nothing has changed regarding those accounts. And including as part of that, the use of backdoor Roth conversions or mega backdoor Roth contributions, which is a more, a little more complex tax strategies have also not been impacted. So in that, it includes normal Roth conversions. There aren’t any provisions in The SECURE Act 2.0 that addressed those changes.

The age at which you can begin Qualified Charitable Distributions has not changed like Alex has mentioned. It continues to be age 70 and a half. And so, even if your RMD age is pushed back to 75, you’ll still be able to take advantage of this awesome tax strategy once you’ve reached that age.

And then lastly is the clarification on what’s called the 10-year rule that was originally created by the first SECURE Act. And it really only applies to those that inherited IRA accounts from non-spouses. Meaning if you inherited an account from an aunt or an uncle that was already taking Required Minimum Distributions, it was on the original understanding that you had 10 years to be able to pull that money out from that account. You had 10 years to pull all that account money out of that account.

But there might be some additional clarification where you might have to take some Required Minimum Distributions each year within that 10-year window or some other changes that they’re going to come out with. So that clarification has not come out yet. We’re expecting an answer, some additional insight on that later this year or even next year, the beginning of next year. And so we’ll be keeping an eye on that.

But those were some of the four main things that people were worried about that was going to change with this bill that actually was not covered and not changed.

So in summary, like Alex talked about, there is a lot of different things that the bill covered. There was about 4,000 different pages that was included in this bill, but we wanted to cover the most important things that pertains to retirement. We talked about how the 529 transfer rule works to Roth IRAs and how that can be used as a legacy planning tool. We talked about Required Minimum Distributions and how those ages have been pushed back as well as the additional changes for surviving spouses. We talked about the inflation adjustments to Qualified Charitable Distributions and how they will adjust each year for inflation as well as the retirement catch-up contributions. And ultimately what was covered and what was not covered in The SECURE Act 2.0.

So we want to leave you with a couple of questions here today. First, think about how will these changes affect my plan and how can I best plan going forward.

For clients of Peterson Wealth Advisors, reach out to your advisor if you have questions. Be rest assured your advisor will bring these changes up to you if it applies to your situation. But during your spring meeting, feel free to reach out or sooner to see how these changes might apply.

And those that aren’t clients of Peterson Wealth, but would like to know how these changes might impact your retirement and your situation, feel free to reach out to our office and schedule a free consultation. We’d be happy to meet with you and at least point you in the right direction.

So now we’ll leave the rest of the time for questions. We may not be able to get to everybody’s question today. But if we don’t, feel free to send an email to info@petersonwealth.com. We will make sure that one of our Certified Financial Planners will reach out to you and answer your questions. But for now, we’ll leave the rest of the time for you and your questions that you may have.

SECURE Act 2.0 Question and Answer (23:01)

Daniel Ruske: Oh, I didn’t mean to interrupt. Sorry, Alex. I have a question here that Greg wants to know the answer to, are you ready for it?

Alex Call: Yeah.

Daniel Ruske: So it says, is it only the extra catch-up amount that has to go into a Roth, or is it all catch-up contributions now?

Alex Call: It’s a great question and I appreciate that. To get that clarification, it is all catch-up contributions. So once you turn 50, if you’re doing the catch-up, that has to go into a Roth 401k.

Daniel Ruske: Awesome, and then we had some other questions that I know Carson answered by typing, but I’ll read them here for the class. It says, any moved funds from a 401k to an IRA so one can do a Qualified Charitable Distribution?

Carson Johnson: Yeah, so on that one, the answer is yes. So it’s important to remember with this Qualified Charitable Distribution strategy that you can only do that from an IRA retirement account. So QCDs are not eligible and 401k’s or 403b’s or other retirement plans are only eligible from an IRA, and it’s actually pretty easy. If you roll over money from your 401k, you can actually set up an IRA account at Fidelity, Schwab, Vanguard, or any of the major companies. And just roll it over so that money goes from your 401k to your IRA and to be able to do that strategy.

Daniel Ruske: Awesome. A couple more coming in that I think are good. How do you differentiate between a catch-up contribution and a regular contribution?

Alex Call: That’s a great question. We don’t really know how that’s actually going to be applied and that will likely be something that the 401k plan administrator, the one who manages the 401k, will have options and be able to help you differentiate between those two. Between what’s a catch-up and what’s the regular.

Carson Johnson: Generally though, if you haven’t reached your 401k contribution limit, your first contributions will be the 401k or will be the regular contributions. And then once you’ve reached that limit, then that’s when the catch-up contributions kick into place. But every plan is different. So it’s up to like Alex said, the plan administrator there.

Alex Call: Yeah, but Carson just again to reiterate that it will be having the first money in will always be the regular, and then it’s the last money. So let’s say the regulars $20,000 for the year and the catch-up is $4,000. Those numbers aren’t accurate. But for the first $20,000 it is the regular. And then the last $4,000 that you put in would be catch up.

Daniel Ruske: Very good. So Kevin has a question, here’s the question. And make sure to sort this out here. It says, when RMD start, first day of the month following the month turning the required age, or is it April the year following the year you turn the required age, say 73? I’ve heard different definitions of what the actual RMD is required to start.

Carson Johnson: Yeah, great question there. So with Required Minimum Distributions, how it works is generally your first one is due by December of that current calendar year. However, there’s an exception for your very first one. So The SECURE Act did not change this at all actually. So if you’re taking your very first Required Minimum Distribution, let’s say you’re turning 72 in this year, 2023. With the change to The SECURE Act 2.0, you don’t have to take it this year, you can take it in 2024. But because it’s your first RMD, you actually have the ability to wait to take your RMD until April of 2025.

And you can do that if you want. But then the danger with that is that if you wait till April 2025, you’ll have to take that RMD plus the RMD that’s due for 2025 by December of that same year. So essentially, you’re going to have two RMDs due in 2025, in that particular example.

Daniel Ruske: Very good, so I’ll do one last one if that’s okay. So Dave wants to know, it says, a QCD transfers funds to a charity but has no tax advantage in the year the funds transfer such as a donation to a Donor Advised Fund. Is that true?

Alex Call: So with that, to answer the question David, you’re not able to, you don’t get the charitable contribution deduction in that year. But what you are able to do is that the money that you take out of the IRA, instead of you paying taxes on it and then donating it to charity, it just goes directly to charity.

And so it’s a tax-free transfer. So a lot of what we have found is that for about the majority of our clients, that the QCD is more advantageous at 70 and a half than a Donor Advised Fund. But there are always exceptions with that. And for your case, or for anybody else’s, your advisor will be able to let you know if it makes sense to do a Donor Advised Fund instead of a QCD. But for the majority of people, we have found that the QCD is more beneficial.

And then I was going to do, just really quick, we had somebody ask us if we can notify you through email when we find out the details on the amount allowed on the extra catch-up contributions for those between 60 and 63? Absolutely, we’ll go ahead with that. We’ll put a note in that and we’ll send out more of a mass email to our email list for that.

And then Carson, we had one more. So do the Roth earning limits apply to the catch-up contributions now that catch-up needs to go into a Roth 401k?

Carson Johnson: Yeah, so on that, how I understand it, and Alex you can correct me here if I’m wrong, but when it comes to the actual amount that’s contributed that’s counted towards the limit is just your contribution that you make. The earnings that are on those contributions are going to apply to the catch-up contribution there.

Oh, on that one, so that’s a great question. So Alex asked, or talked about a lot of the catch-up contributions for 401k plans, retirement plans, and how if you exceed a certain dollar amount that those catch-up contributions have to go into a Roth 401k. That does not apply to catch-up contributions for IRA accounts.

So you can still earn more than the $145,000 limit and your catch-up contributions, your additional amount that you can make to IRAs, does not have to be Roth it can still be traditional IRA.

Alex Call: That’s good. Well, that’s all the questions that we have. Thank you very much everybody for attending. If you could there will be a really brief survey. If you could fill that out as soon as we end this that would be great. We’re always looking for input of how we can improve, and probably more importantly what it is that you want to learn about so that we can get you the information that you’re wanting to know about.

So, thank you again. And Carson thank you so much for helping.

Carson Johnson: Yeah, you’re welcome. Thanks guys.