Presenter

Presenter

Executive Summary

Carson Johnson and Alek Johnson focus ‘How Does Retirement Impact Your Taxes?’ on the taxation of different account types, Roth conversions, Social Security, and different charitable giving strategies in retirement. Follow along with the transcript below.

How Does Retirement Impact Your Taxes? (0:00)

Carson Johnson: Thanks for joining us today, we are very excited about this topic. When we were seeing the numbers and how many people registered, it seems to be a really popular topic and we hope that the information we provide today is really helpful in answering some common questions we get.

So to get started, a quick introduction for those that don’t know me, my name is Carson Johnson. I’m a Certified Financial Planner™ and Lead Advisor here Peterson Wealth.

Along with me is Alek Johnson, another one of our Certified Financial Planners™ and Lead Advisors.

Alek Johnson: Yeah, thanks Carson. Excited to be here with you all today. We’ve got a lot of information prepared for you and we’re just excited to dive in and get going here.

Carson Johnson: So a couple of housekeeping keeping items first that we want to go over, that we figure that today’s presentation will be about 30 minutes with a short Q&A afterwards. So if you’re on a time crunch, don’t worry, we’ll have this webinar being recorded so you can watch it at another time. So that email with the recording will be sent out tomorrow and so just be on the lookout for that.

Also, in Zoom, there is a Q&A feature. So if you have any questions throughout the presentation, feel free to use that. We have Daniel and Josh who are advisors here that can help answer any questions along the way.

And then at the end of the presentation feel free to fill out the survey. The purpose of the survey is to help us get better and as well as get some ideas for topics that you may want us to talk about in the future.

So with that introduction, let’s get started.

So our hope today and objectives that we can help you answer five common questions that retirees have as they prepare for and enter retirement.

Questions like how does retirement impact your taxes? Understand the taxation of different types of accounts, how Social Security is taxed, what are Roth conversions, and when you should consider them. And then understand some charitable giving strategies that are available to you in retirement.

So first, let’s talk about how does retirement impact your taxes?

How Does Retirement Impact Your Taxes? (2:06)

A key part of planning for retirement is first, a basic step, is determining how much of your income that you will need to cover your expenses.

Taxes can be one of the largest expenses in retirement and shouldn’t be overlooked. And there are some small changes that occur upon retirement. Things like no longer contributing to your retirement accounts like your 401(k), or not having to pay FICA taxes, Social Security, Medicare taxes.

But today we want to focus on some of the main items or common pain points for retirees as they retire.

If you think about it, while you’re working in your career, income generally comes from your employer with the exception of those that are self-employed or invest in real estate.

But when you retire, your income may come from a variety of sources. Things like Social Security, pensions, and your investment portfolio. And each may have its own taxation rules or may be taxed differently.

So understanding how your retirement income will be taxed well in advance can significantly make an impact on how long your assets last in retirement as well as minimizing taxes in your life and in your heirs.

So first, let’s talk about tax withholding and quarterly estimated payments for once you’re retired. Our federal tax system is a pay-as-you-go system. This means that taxes are paid throughout the year in the form of estimated payments or withholding.

And while you’re working, you have the option to make certain elections which withholds a certain amount of money from each paycheck that goes towards these towards your taxes.

But once you’re retired, that responsibility is placed squarely on your shoulders. And you have to make sure that the appropriate taxes are paid.

Retirees have complete control of this and how they withhold and how much goes towards the IRS or state, if you live in a state that has state income tax.

Overpayment and Underpayment Consequences

Overpayment Consequences

If you withhold more than you owe, then there is an overpayment which results in a tax refund. And an underpayment will result in owing a tax liability or a tax bill.

Tax Withholding

It’s a common misconception out there that people think that if you get a tax refund that it’s a gift from the government for filing your taxes, which certainly isn’t true.

In fact, tax refunds are just as simply a refund or return of your dollars that you’ve overpaid throughout the year. And so, it’s important that you remember that and the goal for many is to withhold enough to cover your liability while not withholding too much and using your funds ineffectively.

So that’s essentially the tax withholding piece.

Estimated Payments

The second method is estimated payments, which is a method used by people who do not work as employees or have income sources that do not have withholding as an option.

So this typically takes shape in the form of having a non-retirement investment account where they don’t have withholding as an option so they have to make those estimated payments.

Now many of you may be thinking, well if the timing of my tax payments doesn’t impact the amount of tax that I pay, then why don’t I just don’t withhold anything and just wait till the end of the year and pay my tax bill then?

Then I can use those funds that I would have used to pay for taxes and invest it or for other uses. Well first, you may want to keep that money set aside because you know you’re going to have to pay your taxes soon and you don’t want to invest and lose that money.

Underpayment Consequences

But second and most importantly, if you underpaid too much on federal taxes, then there may be an additional penalty that’s added to your tax bill. So although this may seem like a small adjustment for some of you, for some retirees it can be quite challenging and new because they’ve never really had to manage their tax withholdings. They just make their elections through their paycheck through their employer and it takes care of their tax withholdings.

So getting the withholding right so that you don’t over-withhold or under-withhold requires some work and requires some tax planning.

Next, let’s talk about tax deductions.

Understanding Tax Deduction (6:13)

In a very basic and simplistic explanation of how we are taxed, we take our total income minus tax deductions, which equals the amount of income that’s subject to tax.

Due to some recent changes, tax law changes, in 2018 and because of the very nature of retirement, I want to share a few ways it may impact retirees and how they take tax deductions.

So first, the IRS has a list of things that we can count when we itemize deductions. This may include your mortgage interest, charitable contributions, property taxes, state and local taxes, and a few more.

The IRS also has a standard deduction number that we can use. And if our itemized deductions don’t add up to be more than the standard deduction, then you will automatically take the standard deduction. In other words, taxpayers receive the greater of itemized deductions or the standard.

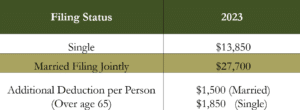

So let’s take a look at what the current standard deduction is. The standard deduction for a person that files a single return in 2023 is $13,850. For those that are married and file a joint return, the standard deduction is $27,700.

There’s also an additional deduction that is added per person if you are over the age of 65, which is $1,500 for those that are married and $1,850 for single filers.

Now a few minutes ago, I had mentioned that there were some changes made back in 2018. So what were they and how does it impact retirement?

Those changes ultimately doubled the standard deduction amount. So in 2018, the standard deduction for a single filer was $6,350, and for married filing jointly was $12,700. So you can see that the standard deduction has significantly jumped up, it’s doubled about.

And again to reiterate, or reiterate what I previously went over, this means that unless you have itemized deductions and excess of the standard deduction, you’ll simply just take the standard deduction.

In fact, according to some data from the IRS, about 90% of Americans now take the standard deduction because of these changes. This is particularly important for retirees that generously give to charities each year.

Many of you will not be itemizing deductions going forward which means you will not get a tax benefit from making charitable contributions. Later today, we’ll actually be talking about different ways you can get more out of your charitable giving so that you can maintain that tax benefit which Alek will go over.

Next, let’s talk about the taxation of different accounts.

How is Retirement Income Taxed? (8:52)

As you enter retirement, many often ask how will my retirement income be taxable, and what will my tax rate be once I retire?

These are excellent questions and as we understand that and with proper planning, retirees can end up having a better tax outcome.

So to help answer these questions, we’ve got to understand the basics of how different sources of income and different types of accounts are taxed.

Three Types of Retirement Accounts

Broadly speaking, you have three account types each with its own unique tax advantages. You have tax-deferred, tax-free, and taxable accounts.

Tax-Deferred Accounts

Tax-deferred accounts such as 401(k)s, 403(b)s, and traditional IRAs are funded with pre-tax dollars.

This means that by contributing to your 401(k) or to these accounts, it reduces taxes because the income that you put into these accounts are not reported. It’s not taxable.

Once you make those contributions then those savings grow over time and grow tax-deferred, meaning that you’re not taxed on any of the growth things like gains, interest, dividends. None of that is taxed while over the course of your life.

Now, unfortunately, you can’t leave your savings in these accounts forever. The IRS requires you to take RMDs, Required Minimum Distributions, starting at either 73 or 75 depending on your age. Those rules have recently changed with The SECURE Act 2.0. And if you have questions about that, we can tell you what those changes were.

Once money is distributed from these accounts they are 100% subject to tax based on your tax rate, and that’s an important part.

Tax-Free Accounts

Now moving on to tax-free accounts, unlike tax-deferred accounts, contributions to Roth 401(k)s or Roth IRAs are made with after-tax dollars. So they won’t reduce your current taxable income as you make those contributions, but as you make those contributions and they grow, they also will grow tax-free. And when you withdraw money from these accounts, you won’t owe any taxes on that income which includes any of the growth or appreciation you’ve earned over the years.

Taxable Accounts

Lastly is taxable accounts. Whether you have a bank account or an investment account, the taxation is actually similar. These accounts are funded with after-tax dollars and the flexibility these accounts provide is that you can sell investments, you can contribute to them, you can withdraw money at any time, and for any reason without penalty.

Any taxable investment income is taxed in the year that it is earned or received, and investments sold for a profit are subject to capital gains taxes.

So an easy way I like to think of it, as dividends and interests come into these accounts, your taxed. But then capital gains only applies when you buy an investment, it grows in value, and you pay capital gains taxes.

Generally with taxable accounts, the tax rate on this, on these types of earnings is at a lower rate than if you were withdrawing from a quote 401(k).

It doesn’t depend on your tax bracket, but generally that is the case.

As you prepare for retirement, it’s important to remember that retirees can’t and often won’t make good decisions about reducing taxes in retirement and without first mapping out and projecting a future income stream,

At Peterson Wealth Advisors we use our Perennial Income Model™, which is our approach to creating a retirement income stream to provide the organizational structure to recognize and benefit from major opportunities for tax planning to reduce taxes and ultimately maximize the retirement outcome.

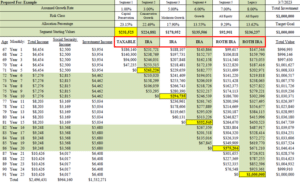

So on the screen, I’ve shared with you a simple example of how this can be done with our approach, the Perennial Income Model. For those that are not familiar with this plan, this is an example of what that looks like. And I won’t go through all the details of how this works, so if you want to learn more about it, there are videos on our website. And actually tomorrow, the email that Everett sends out, he’ll include a link to that video to explain how this process works.

But the main thing to know about this plan is it tells retirees the amount of income they can reasonably expect in retirement, as well as how their investment portfolio should be structured because money that you will need in the beginning of retirement that you’re drawing for from income needs to be conservative while money that you may not tap into for 10, 20, 30 years from now needs to get a better return and keep up with inflation.

The plan is split up among six different segments, and each segment represents five years’ worth of retirement income.

So, let’s see how this would apply in a tax planning perspective. Let’s say a client has a taxable account, an IRA account, and a Roth IRA.

One way that you can structure this is by living off of the taxable account for segment one, which will have very little tax impact. You’re still taxed on dividends and interests, but you can keep your taxes fairly low in a taxable account.

Then this gives you an opportunity for the taxpayer, the retiree, to do things like Roth conversions, which we’ll talk about here shortly, which can help reduce the impact of Required Minimum Distributions once you start those at 73 or 75.

Then segments two through four, income will come from the IRA account and there are ways to also pull money out of those accounts tax-free if you do it in a certain way, and Alek will go over that here shortly as well.

And then lastly, if you do Roth conversions or have Roth IRA money, having it at the end of the plan allows you to maximize that tax-free money over time. You can see that this plan ends with $1,000,000 and all that $1,000,000 would be in a Roth account that is tax-free.

So if you needed to tap into that at the end of your plan for significant healthcare costs, or simply leaving an inheritance for your heirs, that money will be tax-free to help minimize taxes for you.

Now not everyone is married and in the same situation, and so every retiree’s tax planning is going to be unique and custom. There’s lots of ways you can do this and one other option you could do is maybe taking half of your income from taxable accounts or Roth accounts and half of it from IRA accounts.

And what that does is you can help manage your tax brackets and the amount of income that is taxed over the course of your retirement. So tax planning requires careful consideration of each aspect of your plan and being aware of how you draw your income and which accounts you have.

Okay, now let’s move on to talk about Social Security benefits. So today in many instances, more money can be saved by minimizing the tax on Social Security then strategizing on how to maximize your benefit.

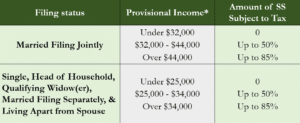

Social Security is unique compared to other sources of income because it’s taxed differently. I won’t take time to go through every single detail of how it’s taxed, but I want to go over the most important items which is if your only income was Social Security, then your benefits would not be taxed. However, the IRS has a formula where the more money you make outside of Social Security, the more your Social Security benefits are taxed.

So for example, on your screen you can see how it’s broken down. If you are married filing jointly and you have combined income over $44,000, up to 85% of your Social Security benefits are taxable or are included in the tax formula. If you have income between $32,000 and the $44,000, up to 50% of your benefit is included or subject to tax.

I’ve also included how it works for those that are single filers as well, but you can see it’s based off of your other sources of income.

So the way to reduce tax on Social Security is to reduce the other sources of taxable income that you have.

So just to give you a few ideas on how to do this, first reduce other income with tax advantage investments. Now calling this conception that people have is municipal bonds. Although they may be tax-free or tax-exempt from a federal level, they are included in the taxation of Social Security.

But another way is you may want to invest in things called like Exchange Traded Funds which is just a fund that has better, that is more tax efficient than say mutual funds because mutual funds will often generate capital gains and other income that may increase your taxes.

Second, anticipate your Required Minimum Distributions. If you think that your RMDs may put you into a higher tax bracket, you may want to consider drawing down your IRA before you reach RMD age. And even better if you can do Roth conversions and getting that into that tax-free account, that can help reduce the impact of RMDs.

Next, maybe delaying Social Security. By delaying your Social Security benefits you reduce the number of years that your benefits are subject to tax. And if you coordinate that with either Roth conversions or other tax planning strategies, that can help enhance the tax outcome.

And then lastly, consider doing a Qualified Charitable Distribution. Alek will be going over this, but the QCDs are the best way that I know to reduce the tax on Social Security, significantly saving you money and also accomplishing your charitable giving goals.

What is a Roth Conversions? When Should I Consider one? (18:22)

Alek Johnson: Okay, thanks, Carson. That’s a lot of information that is very important I think for any retiree to be able to understand.

So another question that kind of regularly comes up during the retirement stage is that of Roth conversions.

And so I just want to take a few minutes and go through this strategy with you, like Carson mentioned.

So, what is a Roth conversion? Well, as Carson mentioned virtually all these retirement accounts are classified into one of two categories. And that is that they either contain pre-tax money or post-tax money.

So for most retirees, it is much more common to have retirement accounts that are in that pre-tax money column. So what a Roth conversion allows you to do is take a pre-tax retirement account and convert either all of it or just a portion of it to a post-tax Roth account.

Now keep in mind that just as the name suggests, any money in a pre-tax account has never actually been taxed before. And so, any amount that you choose to convert will become taxable to you in the year that conversion is performed.

So for this reason it’s very uncommon that you would be converting an entire account at once as it would likely just push you into a higher tax bracket and create a tax bill that’s unnecessarily large, right?

For example, if you were to convert $1,000,000 all at once from a traditional IRA to a Roth IRA, you’d be paying close to 40% in taxes.

So generally the advice that we give our clients as advisors is to convert enough to get the future benefits of a Roth conversion, but not too much that it pushes you up into the next federal tax bracket.

Now a common misconception is that it is better to pay taxes on the seed than on the harvest. Meaning it’s better to pay taxes now and let them grow tax-free than vice versa. The truth of this is it doesn’t really matter when you pay the taxes on the seed of the harvest if the tax rate is the same.

So that being said, what’s often more advantageous in your specific situation comes down to the amount of time that you have to invest but also what tax bracket you are in and when you’re in that tax bracket.

Now, knowing that the conversion is all taxable kind of begs the question well, why should I do a Roth conversion? How do I even know if it’s going to benefit me?

There are several situations and benefits where a Roth conversion can help you in the long run. So let’s just say situation number one, your current income is low now, so you’re in a lower tax bracket and you expect to be in a higher tax bracket again in the future. That would be an opportune time to do a Roth conversion, is you’re going to pay minimal taxes in the lower tax bracket compared to the higher tax bracket.

A second benefit is Carson showed in that quick example, most oftentimes we use those Roth accounts as the last place that we’re taking retirement income from. That being said, with those pre-tax accounts there’s those RMDs that need to be satisfied. And so it makes sense that we would be pulling your income from those accounts first.

Often, that’s going to lead the Roth IRA to just be growing in the background. Not only that but because we’re not using the Roth IRA for your short-term expenses, we can then invest it more aggressively so that it’s going to accelerate that tax-free growth that you’ll get.

Now, this can provide a benefit to you as Carson mentioned either later in retirement to have a source of tax-free income or to your heirs as any inheritance left in that Roth account is going to be tax-free to them as well.

And then lastly, another advantage of converting to a Roth is that those Roth accounts do not have any Required Minimum Distributions. So as Carson mentioned, once you hit age 73 or 75 now depending on when you’re born, the IRS requires you to take money out of that account so that they can get those taxes that they have been ever so patient waiting for.

For a lot of folks between their different income streams such as Social Security, pensions, maybe some rental income, really they don’t even need that money from those pre-tax accounts to cover their living expenses.

So what often will end up happening is that with an RMD, you are now going to end up paying on taxes on money that you’re not even using. And so if you’re account had been converted to a Roth first, you would not be required to take any of that money out and it can continue to grow tax-free.

Now I just want to give you a quick practical example here. So we’re just going to take up our make-believe Brother and Sister Reed here. They were just called to serve a mission in Columbia.

Now currently before they’re going on their mission, they’re spending about $10,000 a month as they like to travel, they like to have fun, they like to spend time with kids and grandkids, so on and so forth.

Now once they begin their mission, their expenses will drop drastically. Not only is moving to Columbia a lower cost of living but now they’re not doing a lot of those extracurricular activities. And so their income drops to that $4,500 a month.

So what’s happening is they’re needing to withdraw less so their total annual income is going from $120,000 a year to $54,000 a year.

Tax-wise, that means they’re going from the 22% bracket down into the 12% federal bracket. That’s a 10% gap there. Given their new situation, this is the perfect time to do a Roth conversion. They could convert just over $50,000 from their traditional IRAs into their Roth IRAs. Again, they only end up paying 12% on this conversion opposed to the 22% that they would have paid if they had done that free or post-mission.

Another key thing here is depending on the length of their mission, if they serve a two-year church mission, they could even be able to do that type of conversion twice.

So obviously the more long-term benefit of this is now you have $50,000-$100,000 invested aggressively that will continue to grow and grow tax-free. And that can turn into a pretty hefty amount rather quickly.

However, to illustrate just a near more near-term benefit, let’s imagine that once Brother and Sister Reed get home from their mission in Columbia, they want to celebrate just being reunited with kids and grandkids again. So they decided to take that same $50,000 they converted and now go on a trip to Disneyland.

They’re able to pay for that trip entirely tax-free while remaining in that 22% tax bracket. If no conversion had been done and the same trip had been taken, then the tax bill for that year would have been $5,000 higher. So you get an immediate $5,000 savings just in the following year when you get home from that mission.

That being said, missions as well as other scenarios can definitely be beneficial to do a Roth conversion.

Strategies for Tax Efficiency When Donating to Charities in Retirement (25:24)

All right, now speaking of charitable endeavors here, another tax strategy that comes into play during the retirement stage is that of how you’re going to donate to charity. So I just want to briefly go back to what Carson said just a couple of minutes ago regarding that standard deduction.

More and more people are taking the standard deduction nowadays which essentially eliminates the deduction that you get when you’re going to donate to charity.

Now that being said, there are still three strategic moves that you can make to be tax efficient when you donate to charity that I want to highlight with you today.

1. Donating Appreciated Assets to Charity

Strategy number one is donating appreciated assets to charity. Now donations and kind are essentially non-cash assets. So for those of you who know our founder Scott Peterson, there was a time back when he had hair that essentially all charitable donations were made in kind.

And so instead of using cash to pay tithing and other church obligations, essentially the members of the church will bring what they produce to the Bishop’s Storehouse. You know tithing was paid using eggs, milk, bales of hay, essentially what agricultural products they had.

The church as well as other charities around still accept certain donations and kind. Here’s my little play on words for you. So our ancestors would pay their tithes and offerings by donating apples. And today, we too can pay tithes and offerings by donating Apple. It’s just a little bit of a different kind of apple with Apple stock.

It is a very common practice to donate appreciated stock to charity which can definitely result in generous tax savings. Now all charities including the church, they know how to receive these donations in kind.

They can accept really almost all marketable securities such as stock, mutual funds, ETFs. Some will even accept gifts of real estate, life insurance policies, partnership interest. So there’s kind of a vast realm of what you can donate in kind. You should always check with your intended charity to see what they’ll accept. But as you can see, it’s a great strategy.

I just want to give you just a quick practical example of how that would look. So we’re going to take the Smiths. The Smiths want to donate to charity. If the Smiths, as you can see here, if they were to sell the Apple stock and donate the cash, they would end up paying that $5,000 in federal and state tax and end up donating that $20,000.

However, if they donate the Apple stock directly in kind, they can donate the full $25,000 and skip out on paying any of the tax.

Benefits of Donating Stock and Other Appreciating Assets to Charity

So here’s a couple of the benefits that the Smiths are going to receive for their donation. One, the charity is going to get an additional $5,000, or essentially a 20% greater donation than they would have if they liquidated.

The Smiths will not have to pay any tax on the gain of the stock. The Smiths also get to deduct $25,000 versus $20,000 as a charitable contribution.

And then what cash they would have been using to pay for the tithing with cash, they can instead use to invest in a more diversified stock of portfolio, portfolio stocks I should say.

Now, this strategy obviously saves you from paying the capital gains tax as you can see here illustrated. But if you don’t donate enough, you may still be taking that standard deduction.

However, there is a strategy where you may be able to combine your donations in one year to get a higher deduction where you can itemize, and then the next year revert to taking that higher standard deduction when you’re not making any charitable donations.

2. Bunching Donations

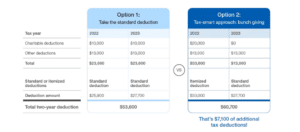

This is called bunching. And I just want to give you a quick glimpse of how bunching works. So again, let’s just take another example here, Mr. and Mrs. Miller. Now, the Millers regularly have $23,000 of deductions each year of which are about $10,000 are going to charity.

So as you can see on option one, with the $10,000, if they spread that out $10,000 and $10,000 over 2022 and 2023, their total deduction each year is only $23,000, which is under that standard deduction. And so by default, they’ll end up taking that standard deduction. And the combined two-year deduction at the bottom here, you’ll see that $53,600.

Where option two, the more tax savvy approach, instead of donating $10,000 in 2022 and 2023, they’re going to bunch that and combine it into 2022 where you can see, now in 2022 there are total deduction is $33,000 instead of $23,000.

This allows them to itemize as they are higher now than that standard deduction. And in 2023 they will revert back to taking that standard deduction.

At the very bottom here, you can see you have the total of $60,700. So that’s a $7,100 additional tax deduction swing.

Now one item that our clients bring up is okay, this seems like a really good strategy, but one, they either don’t want to get behind on their donations or they don’t feel comfortable paying their donations ahead of time. They’d rather be paying it in the year that they’re contributing.

This is where the second half of this strategy comes in, which is utilizing a Donor Advised Fund. So a Donor Advised Fund is not necessarily an investment, but rather just a tool which again may or may not be right for everyone, but we want to make sure you’re aware of it.

Donor Advised Funds

So Donor Advised Funds, or DAFs, they’ve been around for years and there’s a lot of them. They’ve become more and more popular, especially over the last decade, as you essentially have Fidelity, Vanguard, Charles Schwab, promoting them more.

What are Donor Advised Funds and How do they Work?

The best way to describe a Donor Advised Fund is that it is an account to hold your charitable contributions until you decide when and to what charity you want to ultimately donate to.

So to give you kind of the idea of how it works, the donor is going to make a charitable donation to the Donor Advised Fund. This can be done either in cash or better yet as we just talked about a donation and kind such as a share of stock.

The donor then receives this tax deduction back for the contribution in the year that the contribution was made. This could be a good planning tool for someone that has a higher income. Maybe their last year of retirement, or they’re selling a business and they know that in retirement they’ll have less of an income.

Now your donation is going to sit inside of this Donor Advised Fund in an investment account and it’s going to continue to grow for you until you decide where you want to give that to and when you want to gift it. So it’s kind of up to you on the timing of those when they go out to the charities.

Practical applications of the Donor Advised Fund

- With the DAF, essentially bunching of deductions becomes easier to do and charitable giving becomes much more flexible and easier to accomplish.

- A Donor Advised Fund helps the charitable donor get a tax deduction when it’s advantageous to the donor. Again, if you have a higher income year, it may make sense to donate more when you can get a bigger tax deduction.

- You essentially create a legacy for future generations. You can kind of think a missionary account for future grandchildren, anything like that.

Now this brings me to my last point on charitable giving, which is what you can see here is a Qualified Charitable Distribution or a QCD for short.

Qualified Charitable Distribution (QCD)

Now a QCD is a provision of the tax code that essentially just allows you to withdraw money from an IRA to be tax-free as long as that is paid directly to the qualified charity.

Now there are huge tax savings that can be realized by incorporating the use of these QCDs, but it’s not necessarily about by how much you donate to the charity, but by simply altering the way that you contribute to the charity.

So I just want to highlight a few perks here. The first is you didn’t have to pay income tax when you earned the money that you either put into your IRA or 401(k) throughout your working years.

Second, you didn’t have to pay taxes on the compound interest that your IRAs earned over the 30, 40-year working career that you had.

And then last, any money paid directly to a charity using a QCD from the IRA will not be taxed. So that’s triple tax savings, that’s definitely huge.

4 Benefits of Using a QCD

As Carson mentioned, it can potentially reduce the amount of Social Security benefit that’s going to be taxed.

Second, it can reduce the overall amount of income that is taxed.

Third, it’s going to enable you to get a tax benefit by making a charitable contribution. Now one thing I want to highlight here is with the standard deduction, when it comes to QCDs, whether you itemize or take the standard deduction, you will still get a tax benefit by doing a QCD.

So it doesn’t matter which one you take once you hit the QCD.

And then fourth, a Qualified Charitable Distribution counts towards satisfying those Required Minimum Distributions that you have to take out starting at again, age 73 or 75.

Now as beneficial as QCDs are, they’re unfortunately not available to all taxpayers and there are rules that govern these distributions that have to be followed pretty much to a “T”, or also be considered a taxable IRA distribution, which we don’t want to have happen.

The rules for using a QCD

- They’re only available to people older than age 70 and a half. Again, why Congress decided to throw the half in there, who knows but that’s kind of the age there.

- They’re available only when distributions are from an IRA account. So if you have a 401(k), a 403(b), any other type of retirement account other than an IRA, those are not QCD eligible. You would have to roll it into an IRA first.

- A QCD must be a direct transfer from an IRA to a tax-qualified charity. Meaning you cannot send yourself the money and then pay it to the church or the charity. It has to go directly to them from the IRA.

- There is a cap of a maximum of $100,000 of IRA money each year that is allowed to be transferred via QCD.

I really do believe that every person over age 70 and a half who has an IRA and that’s giving to charity regularly should consider making it through a QCD.

You or your tax professional, you can run a comparison just to see whether it makes sense to do it by cash or by using a QCD, and I think that you’ll find the tax savings will be significant.

Key Insights on Retirement Taxes (36:20)

All right, well, I know that was a lot of information and kind of a short amount of time that Carson and I just gave you so we just want to kind of recap quickly with some key takeaways for you.

So number one, retirement may change the way a retiree manages their tax liability.

Number two, understanding how investment accounts are taxed can help you organize retirement plan and minimize taxes. Carson kind of gave us the big three-bucket approaches there.

Third, the amount of your Social Security that is taxable is based on your combined income.

Four, those Roth conversions can minimize taxes and retirement and for your heirs with proper planning.

And number five, charitable giving strategies can help maintain a tax benefit while accomplishing your charitable giving goals.

Retirement and Taxes Question and Answer (37:11)

So, we have some time for some Q&A here just for a couple minutes, but before we get into that, I just want to thank you all for attending today. I’m going to turn it to Daniel to send over any questions that would be beneficial for the group to hear.

If you have any more like what you feel would be individual-type questions that pertain to your situation, please feel free to reach out to Carson, myself, or really any member here at Peterson wealth, and we’re happy to help.

And then as a quick reminder, there will also be a brief survey after the webinar that we’d really appreciate you filling out to give us any feedback that you have. So, Daniel?

Daniel Ruske: Awesome, well, we have had a handful of really good questions. I’d love to answer a couple of them in front of the group here.

Questions: Once RMDs are required, can they be satisfied by doing a Roth conversion?

Alek Johnson: It’s a great question. So the answer to that is no. Essentially what you have to do is with the RMD, you would have to take that and either put it in your checking account, put it in a trust account first, and then you can convert after that Required Minimum Distribution there. But you cannot use a Roth conversion to satisfy that Required Minimum Distribution.

Carson Johnson: Yeah, another way to think of it is the IRS says you have to do your RMD first before you do conversions. So it’s actually, it’s important to know that because that means Roth conversions might be ideal before you reach RMD rather than waiting to RMD because if that, if you’re doing the RMD, then doing a conversion on top of that’s just going to create extra taxable income.

Daniel Ruske: Awesome, so we have a couple more here and I’ll just remind everybody we do have a survey, we love your feedback, and so hang around just a couple more minutes.

Questions: What is the max amount per year that can be converted from pre-tax to Roth?

Alek Johnson: As far as the maximum, there is no max. Again, you can really convert if you wanted to your entire traditional IRA into a Roth IRA. But again, our advice is you want to make sure you reap the benefits of doing that conversion without pushing you into a higher tax bracket because if you were to convert an entire account, that’s going to likely just unnecessarily boost your tax bill for that year.

Daniel Ruske: Awesome, let’s do two more here.

Question: How we qualify for this 75-year-old Required Minimum Distribution?

Carson Johnson: Yeah, so if I understand correctly, the question is when you start Required Minimum Distributions, I believe. So just to reiterate, there was a new law passed in December, SECURE Act 2.0, and essentially it’s based off of your age now, your RMD start date.

And I believe if I remember right, for those that are born after 1960, the Required Minimum Distribution starts at 75. If you were born before then, it’ll be 73. If you’re starting your RMD then it’s that.

Daniel Ruske: So I’m looking at the cheat sheet you sent me earlier and you’re exactly right. 1960 or later, 75, everybody else, it’s if you started where you’re at or your 63 now.

Question: I can authorize Social Security Administration to withhold some of my benefit. Do pensions usually have the same option?

Carson Johnson: Yeah, so the answer is yes. A lot of times, pensions have withholding elections. So you can just contact your pension provider and ask them. And a lot of them, a lot of them have withholding as an option.

Daniel Ruske: Awesome, time for one more.

Question: I have a Roth IRA and I’m limited to $7,000 per year contribution. I thought I contribute once I stopped working. Can you do a Roth conversion after retirement?

Alek Johnson: The answer to that is yes. So in order to contribute, you are maxed out of that $6,000, $7,000 depending on your age there. However, after retirement, you can still convert no matter what your age.

Daniel Ruske: Awesome, well, that’s the last one. I’m going to take a screenshot of one other for David as it’s a little bit more specific. I’ll have you, Alek, get back to him in a moment.

Alek Johnson: Okay, perfect, sounds good. Well again, thank you so much for attending today. Again, if you have time to fill out that brief survey, that would be great.

Carson Johnson: And any other questions feel free to reach out. Okay, thanks everyone.