Presenter

Executive Summary

Alek Johnson and Chris Cutler, a licensed health/life insurance agent at Cutler Insurance Agency, dive into Marketplace insurance, how it works, and what it means for you. Follow along with the transcript below.

Health Insurance Options for the Early Retiree

Alek Johnson: Well good afternoon and welcome everyone. Thank you for joining us today. We are very excited to be here with you to talk about the Marketplace insurance.

For those of you who don’t know me, my name is Alek Johnson. I am a Certified Financial Planner™ and one of the lead advisors here at Peterson Wealth Advisors.

And then here with me today is also Chris Cutler one of our trusted health insurance agents.

Chris Cutler: Thanks for having me Alek. Happy to be here.

Alek Johnson: Yeah, thanks Chris.

So today’s webinar is, we’re planning on just being nice and short. We’re going to shoot for 20 to 30 minutes here. Now before we get started, I do have a couple of housekeeping items I just want to go through real quick.

First of all, if you have any questions throughout our webinar, please feel free to use the Q&A feature located at the bottom of the screen on your Zoom.

My colleague Daniel Ruske, he’s one of the Certified Financial Planners and lead advisors here as well. He’s going to be responding to your questions as best he can, and then Chris and I will actually take probably three to five minutes at the end of the webinar to answer any general questions you have.

With that being said, if you have a more individualized question that might require a little more analysis, please feel free to reach out to Chris or myself after the webinar, or reach out to our team and we’re happy to schedule a free consultation with you.

Last thing here is that at the end of the webinar, we will also have a survey that will be available just to give us any feedback, make any suggestions again for future webinar ideas. So if you have, you know, three to five minutes after this, any feedback you have would be extremely helpful for us.

So that being said, let’s dive on in here. So here’s a quick agenda of what we want to go over with you today. Now one point of clarification I just want to make here. Back in July, I wrote an article that briefly discussed some other insurance options before age 65. And these are going to be such things as Cobra, the Christian Healthcare Ministries, Medicaid, and a couple others. We will not be diving into those insurance options today. So if you have any questions again regarding those different options, please feel free to reach out and we’d be happy to discuss those with you in a more personalized setting. But today’s webinar is going to focus solely on the Marketplace insurance.

So that being said, today I’ll start off by just giving us a broad overview of what the Marketplace is, how the Marketplace insurance works, and then Chris is going to give a summary of the companies and just the plans that are available to you. And then again, I’ll just wrap up quickly by discussing how the Marketplace insurance can fit into your overall financial plan.

Overview of the Marketplace (2:47)

So what is the Marketplace? In March of 2010 the Affordable Care Act, which is sometimes known as Obamacare, was passed with the goal of just making insurance more affordable for individuals and families. Now the law provides these individuals and families with government subsidies, otherwise known as premium tax credits, that help lower the monthly premiums for households.

The federal government actually operates the Health Insurance Marketplace, or the Marketplace for short, which is just an online service that helps you enroll for the health insurance. And this is always accessible just at healthcare.gov.

How the Marketplace Insurance Works (3:27)

Now how it works, during enrollment you are going to, you or your health insurance agent I should add, will fill out an application. That’s just going to have some of your basic personal information on there.

Now included with this application, you are going to give them the best estimate of what your income will be for the coming year. Now as just a little side note here, the Marketplace uses your modified Adjusted Gross Income to define what your income is for the future year.

Now I just want to reiterate, and please note this, that the Marketplace does not use your previous year’s income. So this is a very important distinction for retirees who may be coming off a year of really high earnings before they retire. So they’re going to be using your future income.

Determining Your Subsidy Amount

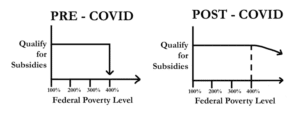

Now based off of what you are projecting your income to be, will determine the amount of subsidy that you are going to qualify for. Now it’s worth a quick note here to discuss pre-COVID versus post-COVID rules.

So before COVID, how the subsidy worked was if your income was between 100% and 400% of the federal poverty line, then you qualified for a subsidy. Now as a reference for a retired couple, so just a household of two, in the year 2022, 400% of the federal poverty level for a retired couple is about $73,000.

Now the catch here as you can kind of see in this depiction was if you made even just one dollar beyond that 400% level then you lost that subsidy completely. It was just a straight drop, a straight cliff with about a 300-foot drop-off.

However, as part of the American Rescue Plan Act, the subsidies were extended to those with income beyond the 400% poverty level. And so from 2021 through 2025, that was just extended recently to get another three years on there.

Higher-income earners can still qualify for that subsidy. So you can see in this depiction here on this post-COVID, it’s just a lot more gradual of a decline instead of that hard cliff. So the higher earners again can qualify for a subsidy.

Reconciling Income Differences at Tax Time

Now one common question we always get is, well what happens if your income doesn’t end up being exactly what you projected it to be? Which if you can get your income to the dollar, I will be completely impressed.

The answer is that you will reconcile any differences when you file your taxes. So to give you an example here, if your income was less than what you projected it to be, you’re going to actually receive a credit on your taxes because you should have been qualifying for more of a subsidy.

Again, vice versa if your income was more than what you projected, then you’re going to have to pay some of that subsidy back when you file your taxes.

So I’m going to turn the time over to Chris to just talk about some of the companies and plan options that are available to you.

Companies and Plan Options Available to You (6:30)

Chris Cutler: Perfect, thanks Alek. So if you’re coming from a company-sponsored health insurance plan, there may be some differences going into the marketplace and looking at your options.

So it is important to consider a lot of different things when you’re trying to find a health plan that’s a good fit for you.

So if you look at this kind of left-hand column there, those are all the companies currently represented on the Marketplace.

And each company has, you know, different doctors and hospital networks to choose from. And even inside each health insurance company, they have different networks to choose from.

So it can get a little bit confusing and it’s important to kind of take your time. Make sure your doctors, prescriptions, and all your needs are met when you’re sifting through these different plans.

And that’s kind of where I can come in and help you out individually if you would like to make sure to find a health plan that’s kind of tailored to your needs.

There are no PPO options on the Marketplace. Meaning when you pick a company or a network, you need to stay within that within that network unless it’s an emergency.

Open enrollment, I want to mention open enrollment, that’s currently going on right now. It started November 1st and goes through January 15th. Open enrollments a great time to just reevaluate health insurance needs for the upcoming year. During that time, you can enroll and you can change plans or make any updates as needed.

Open enrollment is not the only time you can enroll into a health insurance plan. If you retire early and it’s in the middle of the year where your benefits end, you’ll get a 60-day window from the day you lost coverage to enroll into one of these plans through the Marketplace.

Just to kind of wrap your head around, and what you’re looking at as far as options, I wanted to highlight maybe a couple scenarios that I come across. If you just hit that next slide for me Alek that’d be awesome.

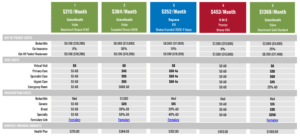

Perfect. So this may not be your exact situation. And again, I’m happy to run through your specific situation, but this is an example of a household size of two within Adjusted Gross Income of right around $100,000.

And as you can see, I picked through a few these bronze plans. The premiums are not too bad if that adjusted gross is going to be around that $100,000 mark per year. They start out, you know, right around $215, and then they go up from there.

There’s a lot more plans than this. I just wanted to grab a few of them, just so you can, just see you can see what options are and maybe you can kind of glance at these a little bit. Most of these come with, yeah, they’re going to cover your needs. And again, these plans might not be specifically what you’re looking for but should give you an idea.

If you could go to the next one Alek, that’d be awesome. Perfect, so this situation is just a household of one.

And I did an income estimate of like $20,000. I run across a scenario quite often where someone has a health insurance plan in place for their family. And then they moved to the Marketplace and they have like a 24-year-old child, maybe working part-time, going to school that was on their health insurance plan. And now they have to figure something out.

Well, this is a really good option because if that child isn’t working full-time making maybe around $20,000 a year, you can get a great insurance plan for them for next to nothing. As you can tell, it’s $9 a month. And we know in today’s world you can’t even buy a burrito for that cost. So it’s a pretty good option for a lot of people if it’s a good fit. So, again, I just wanted to reiterate that I am happy to kind of sit down with you or take a phone call and go over your unique needs and see if something like this would help. Go ahead Alek.

Daniel Ruske: And then Chris, just a quick question came up. If you go back to the last slide. What is the AD mean?

Chris Cutler: Yeah, that’s an abbreviation for After Deductible. So some of these plans won’t cover things until the deductible is met. Others will cover, you know hospital, doctor visits, specialist, or primary care visits before the deductible. It’ll just be a small co-pay.

Daniel Ruske: That’s perfect. Thank you.

Alek Johnson: And then Chris, one more question that I saw I just want to clarify right now since I think it’s a good time. The companies on here, someone just asked, are these only Utah companies? Are there more companies outside of Utah? If you want to just speak to that.

Chris Cutler: Yeah. That’s an awesome question. So these companies that are listed here in that left-hand column are the only companies represented in Utah on the Marketplace.

Now, if you live somewhere else full-time, then the Marketplace will have different companies for that state, or they have their own Marketplace platform to choose a plan.

But you know, kind of like I alluded to earlier, it’s hard to, if you have multiple addresses, it’s hard to find a plan that’s going to work across multiple states. Unless it’s like an emergency situation then you can use it anywhere in the world.

Alek Johnson: Right, thank you Chris so much for showing us that. I hope that provided some value to you to be able to see some of the numbers there. One thing I do want to highlight as well that maybe Chris is being bashful on.

It is actually no cost to you to use a health insurance agent. And so whether you do it yourself or whether you use a licensed professional, they will be compensated directly by the insurance company. And so if this is unfamiliar territory for you, please feel free to use a trusted health insurance agent that can help navigate those waters for you.

How the Marketplace Insurance can fit into your Financial Plan (13:46)

Perfect, so to wrap up I just briefly want to take a moment and explain just how the Marketplace insurance can fit into a financial plan. Healthcare is just such an important aspect of any financial plan that having a good understanding of it is absolutely critical.

Now the Marketplace is obviously a great option up until Medicare kicks in at age 65. But again, it’s important to be able to have a clear understanding of what your estimated income is going to be.

Again, because these subsidies are dependent upon your best guess of your income, having a sound financial plan in place, especially for retirees to know an idea of what your income will be, is extremely important so that you don’t have any tax surprises when you file your taxes.

Another important aspect of the Marketplace that I just want to highlight real quickly is that there may be ways, so we’ll have clients ask us, okay, I want a higher subsidy, but I don’t want to interrupt my cash flow.

And so there are definitely ways that we can report a lower modified Adjusted Gross Income while not affecting the desired cash flow that you have for retirement. Now this type of careful planning can again only be achieved by having a retirement income plan in place.

If that is something that you are interested, again we would love to sit down and discuss and see if that strategy makes sense in your situation.

Retirement Health Coverage Question and Answer (15:20)

So we’re going to turn the time to Daniel to ask us a couple of questions here. But before I do that, again I just want to thank you all for attending today. I hope you got something out of this.

Again, please feel free to reach out to Chris if you have any questions regarding getting on the Marketplace insurance or myself and more on the lines of if you have any questions regarding your financial plan and how this can be applied to it.

But we’re going to just open it up for three to five minutes here for some questions and then we’ll jump off. So Daniel any questions?

Daniel Ruske: Yeah, there’s been some awesome questions coming through the chat box here. I’ve tried to answer them, but there are a few I think that would be beneficial for you to answer for everyone.

Now I got a question here that says, the one time I looked online, I was basically bombarded with phone calls from insurance agents that continued for weeks. How do you start looking at these plans without putting all your information and getting bombarded with people trying to close business?

Chris Cutler: Want me to tackle that?

Alek Johnson: Yeah, go ahead.

Chris Cutler: Yeah, good question. And I’m not sure the exact platform that you’re putting your information on, but I will say I have a link that I can send out and I give you my word that I won’t bug you too much unless you want to approach me and have questions.

But I have a link that you’re able to put in your information and view the plans. And I believe if you go to the healthcare.gov site directly, there is a spot on the website where it will allow you to preview plans for 2023. And it does not require you to put in your email or phone number or anything like that. So you should be able to see the plans on that website without that type of hassle.

Daniel Ruske: Yeah, I can confirm that. I actually do that all the time for clients. You can go in there and instead of putting in your information, you just click a little lower down, it says view plans.

So thank you Chris. I got a couple other here, Chris do you offer, or let me just read the question exactly.

Does Chris offer to discuss options with us extended to those outside of Utah? Is he able to speak to options for those who live in other states?

Chris Cutler: I appreciate that. I’m happy to give any type of, I’m happy to talk through situations. But because I’m only licensed in Utah, I am limited as to what I can help out with. I would not be able to help someone enroll outside of Utah and I am not as familiar with the plans outside of Utah.

But if we’re looking for just general questions things like that about the Marketplace, I’m happy to try to help out where I can.

Daniel Ruske: Awesome, and we’ll do one last one here. What if I don’t know my income, what it will be throughout the year or if it’s variable?

Alek Johnson: Yeah, maybe I can start off on that one, and then Chris if you have any follow-up. So the best, obviously we want to get it as close as possible for obvious reasons, right. We want to try to just pinpoint it.

But if you can’t, anytime throughout the year, you can actually go back onto your application and adjust what it’s going to be. So let’s say you projected it was going to be $75,000, and then let’s just say you got a huge bonus at work, it bumped it up to $100,000. You can go back in and change that and that’ll adjust the subsidy that you are receiving throughout the rest of the year as well. Chris, any other thoughts on that?

Chris Cutler: Yeah, and I think you nailed it. Yeah, if you have some big income swings throughout the year, you can always adjust that. It’s important to keep in mind as well that like Alek mentioned, if you keep it as is you may need to pay some of this, the tax credit back when you file taxes if the actual reported income is higher than what the amount was estimated on the application.

Daniel Ruske: Awesome. Can I do one more Alek? I know we want to hurry and get to the survey. There’s a survey at the end that we’d appreciate all of your feedback. But if we can do one more.

Is it possible to modify a Marketplace plan/coverage if a child leaves for college or a mission or if you need to change it throughout the year? Can you change the plan?

Alek Johnson: Yeah, great question. Chris, you want to tackle that?

Chris Cutler: Yeah, I’ll go for that one. So just to clarify, and the question it was asking if you have a plan in place, the Marketplace, and then you have someone move out of the household and go to another state. You just want to change plans and make accommodations for your child that’s moving. Is that, am I getting that correct?

Alek Johnson: I think so yeah.

Chris Cutler: Okay, so in that situation, a move out of state does give you a special enrollment period. So it would probably make the most sense in that situation for that child that moved out of state to do a new application for whatever state he or she moves into because that would open a special enrollment period.

Daniel Ruske: Awesome, that is all of them. I’m going to answer a couple more here on the chat, but outside of that, that’s been most of them, so appreciate you guys.

Chris Cutler: Yeah, thank you.

Alek Johnson: Perfect, well again thank you everyone for taking the time to jump on. Again, as Daniel said there is going to be that quick survey after this. Any feedback that you have is great. Thank you for attending and we hope you have a good day.

Alek is one of our Certified Financial Planners® at Peterson Wealth Advisors. He graduated from Utah Valley University where he studied Accounting and Business Management. Alek also has earned his master’s degree in Financial Planning and Analytics from UVU.