If you’ve turned your television on in the last 6 months, you’ll know there’s been a lot of discussion on the latest tax bill barreling through Congress. The massive 800-page bill has officially been passed. Some of the questions you might be asking are: What does this mean for me? What stays the same? What’s going to change? How does this affect my retirement plan? In this blog, we’ll give you a preview of some of the critical provisions most likely to impact your current or future retirement planning strategies.

Permanent Extension of Lower Tax Brackets

Under the original Tax Cuts and Jobs Act of 2017 (TCJA), tax brackets were set to revert to their previous levels. Under the Big Beautiful Bill, the tax brackets under the TCJA are made permanent. This extends favorable tax rates for middle and upper-middle-income retirees. Not only does it affect your marginal tax brackets, but it has implications on any Roth conversions you might do, how you manage your Required Minimum Distributions, and even how you look at recognizing capital gains.

Permanent Increase to the Standard Deduction

The standard deduction under the TCJA has also been made permanent. This increases the amount of income shielded from taxation for single and married taxpayers. Below is a chart showing the difference between the standard deduction before the TJCA and now.

Pre-Tax Cut & Jobs Act

Now (2025)

Difference

$6,350 (Single)

$15,750 (Single)

$9,400

$12,700 (Married)

$31,500 (Married)

$18,800

Temporary Bonus Senior Deduction

Under the Big Beautiful Bill, individuals 65 or older will also receive an additional $6,000 deduction per person. This applies whether you take the standard or itemize your deductions. It is subject to an income phase-out of $75,000 (single) and $150,000 (married filing jointly).

This bonus deduction does not change how Social Security is taxed. That remains the same under this new law. Also, you do not need to have claimed your Social Security benefits to receive this deduction.

Example: For a married filing jointly couple both over the age of 65 who take the standard deduction, your standard deduction would be $34,700 ($31,500 standard plus $1,600 for each filer over the age of 65), then they also get the new bonus senior deduction, which is $6,000 per individual age 65 and older. This makes their total deductions $46,700.

Charitable Deduction Changes

Under the new tax law, an additional deduction was created for charitable donations for those claiming the standard deduction. This means that you can deduct up to $1,000 (single) or $2,000 (Married Filing Joint) for cash contributions made to qualified charitable organizations starting in 2026. This deduction is a welcome addition for those who are charitably inclined but don’t meet the threshold to itemize on their return.

Another change is for those who itemize their deductions. There is now a 0.5% AGI floor for deducting their charitable donations. For example, if you have an Adjusted Gross Income of $100,000 in 2026, you must donate at least $500 to charity before you can claim any charitable donations on your taxes. You need to be aware of this hurdle when itemizing your charitable donations.

Increased temporary SALT Deduction

The additional SALT (State and Local Tax) deduction offers relief for residents of high-tax states. Under the TCJA, this deduction was limited to $10,000. From 2025 to 2030, the expanded SALT deduction rises to $40,000. This $40,000 limit will increase by 1% for inflation through 2029. This deduction will most likely benefit those living in states like California or New York with upper-middle-class incomes. There is a phase-out for individuals with a modified Adjusted Gross Income exceeding $500,000, regardless of whether they file as single or married.

For example, if you itemize, with state taxes of $15,000 and property taxes of $10,000, you can now deduct the full $25,000 as an itemized deduction as long as you’re under the phaseout. Before, under the TCJA, you were limited to the $10,000 cap.

Estate & Gift Tax Exemption Set at $15 Million

Under the TCJA, the estate tax exemption was set to sunset from $13,900,000 to roughly $5 million. Under this new law, that exemption is permanently increased to $15 million per individual, or $30 million per couple. Portability, or the ability for one spouse to use the remaining estate tax exemption from their deceased spouse, also remains intact.

While most individuals will not have an estate that exceeds $30 million, this increased exemption is not a suitable replacement for an estate plan. Make sure you have a competent attorney who can help you put the necessary provisions in place to make a smooth transition of assets for you and your family.

Healthcare updates under the Big Beautiful Bill

The One Big Beautiful Bill expands the definition of a High-Deductible Health Plan (HDHP), which individuals must have to be able to contribute to a Health Savings Account. With the new rules, all “Bronze” and “Catastrophic” plans offered on Affordable Care Act exchanges qualify as HDHPs.

Additionally, the Affordable Care Act (ACA) subsidies that were extended post-COVID are ending in 2025. This affects retirees under 65 receiving subsidies under these marketplace plans. Don’t hesitate to get in touch with your financial advisor to revisit what income thresholds are affected by this change. You may also want to consider making adjustments to your healthcare plan and review your timeline for Roth conversions.

Conclusion

The One Big Beautiful Bill does provide at least one promising thing to retirees – clarity. With many of the Tax Cuts and Jobs Act provisions being made permanent, including tax brackets, an enhanced standard deduction, and the new changes to charitable giving, the future looks bright for those entering retirement. If you’d like to discuss how these new provisions will affect your retirement plan in greater detail, contact one of our retirement planning specialists at Peterson Wealth Advisors.

Information on these provisions is discussed in greater detail in a previously recorded webinar on our website. Watch the webinar here.

Most of us sacrifice and save for four decades in preparation for what we hope will be a comfortable retirement. We are laser-focused during our working years on accumulating as much as possible, and by the time we retire, many of us have refined the art of wealth accumulation in our IRAs, 401(k)s, and a variety of other investment accounts. We feel pretty confident in our retirement preparation and then something happens that shatters our confidence…we retire. We quickly come to the realization that successfully investing and managing the distribution part of retirement takes a completely different skill set than accumulating money in retirement accounts.

Besides the universal question of how to invest, there are questions regarding distributions, taxes, risk, and keeping our income up with inflation that will all have to be addressed as we transition from accumulating to distributing our retirement accounts. All these questions bleed into the single, overarching question that every retiree needs to figure out: How am I going to create an inflation-adjusted stream of income from my investments that will last for the rest of my life?

The Need for a Retirement Income Plan

The quality of the next 30 years of your life is dependent upon the decisions that you make at retirement and the plan you put in place. There is so much on the line, and mistakes made at the beginning of retirement are not forgiving. There are no do-overs. A well-thought-out retirement income plan will provide discipline, order, safety, and peace of mind. A sound retirement income plan will allow you to focus on your retirement dreams and not be obsessed with the daily movement of markets, interest rates, or how current events will impact your retirement.

A retirement income plan should be unique to you and your specific needs. So, copying your retired neighbor’s retirement income plan won’t work. Following some generic, “rule of thumb” withdrawal advice from your financial advisor won’t get it done, and buying an annuity that will never keep up with inflation over a long retirement will only serve to crush your future purchasing power. And finally, decades of investing have already taught you the futility of market timing and betting your future on guessing the direction of the stock market.

Now that I have shot down all the popular attempts to create retirement income streams, and before I show you how a professional retirement income plan is created, let’s address what it is that we need a retirement income plan to do.

A Successful Retirement Income Plan Must Address Five Objectives

It must be goal specific.

It must create a framework for investing.

It must create a framework for distributing.

It must create a framework to reduce risk.

It must create a framework for reducing taxes.

Goal Specific

A retirement income plan that is goal-driven provides detailed objectives. It is a date-specific, dollar-specific blueprint that will guide you throughout retirement. A date-specific, dollar-specific plan defines how much income will be needed during retirement, and when it will be needed. Its objective is to deliver future income to the retiree with the least amount of risk, after all risks have been considered. A properly structured retirement income plan matches your current investment strategy with your future income needs. Like any goal-driven program, the performance toward reaching the goal must be monitored to maintain discipline and allow for adjustments if the goal is to be realized.

Create a Framework for Investing

Retirees must find the proper investment mix of low-volatility fixed-income investments and higher-yielding, more volatile equities.

Fixed-income investments such as bank deposits and certain types of bonds can provide a haven to draw income from when the stock market takes its occasional dive. As valuable as these types of investments can be in the short term, they are a long-term liability that will never keep up with inflation.

On the flip side, retirees need to own some equities in their portfolios. Owning higher yielding equities is a logical way to keep ahead of inflation over the long run. But we all know that short-term volatility and unpredictability afflict all who own equities. Creating a retirement income plan that takes advantage of the opposing nature of fixed-income and equities is an essential component in creating a long-lasting retirement income plan.

It’s just commonsense to invest the money we’ll need in the short-term into fixed-income type investments and invest the money we don’t think we will need for a while into stock-related investments. But, most retirees and their advisors don’t invest this way. Unfortunately, the failed practices of chasing last year’s returns and making investment decisions based upon guessing the future direction of the stock market continue to be the prevalent methods used to determine investment allocations, even though these methods have proven to be extremely unreliable.

Following a plan that allocates retirement savings by determining short versus long-term income needs liberates the retiree from having to time the markets or beat the stock market average by superior investment selection. With an investment plan that matches current investments with future income needs, the retiree only needs to concentrate on maintaining discipline and following the plan.

Create a Framework for Distributing

When it comes to withdrawals from investments at retirement, I have noticed two types of personality traits. The first trait is manifested in individuals I will call the “entitled spenders” who think to themselves, “I have been saving all my life for retirement, and I am now retired, so I am going to spend however much I want on whatever I want.” The second type I will call the “paranoid savers”. These people are those who think, “I may have a lot of money, but it has to last a long time. And who knows what the future might bring?” These types of individuals are often afraid of spending any of their retirement funds at all.

The “entitled spenders” sabotage their retirement by spending too much, too early, as they burn through all their retirement savings in the first ten years of possibly a thirty year retirement. The “paranoid savers” likewise harm their retirement by living below their privilege by denying themselves many of the simple pleasures and opportunities of retirement. Ironically, both the spenders and the savers would greatly benefit from the same date-specific, dollar-specific retirement income plan, a plan that outlines how much money can and should be withdrawn from investment accounts and when.

Quite literally, the million dollar question is, “How much can/should I withdraw from my investments each year?” You must be able to answer this question if you’re going to have a sustainable income stream throughout retirement, and if you’re going to be able to enjoy your retirement experience to the fullest.

A sustainable withdrawal rate can be created through determining the answers to three important questions:

How much income will I need to pull from my investments to sustain my retirement lifestyle?

When will retirement savings need to be converted into retirement income?

How should retirement accounts be invested until they are needed to be converted into income?

Again, having a retirement income plan that includes date-and-dollar specifics should drive your withdrawal decisions. Adjustments in either the timing of withdrawals, the withdrawal amounts, or how retirement funds are invested between now and the future income date will impact your future income stream.

Create a Framework to Reduce Risk

A viable retirement income plan must recognize and minimize risks where possible. Retirees are particularly susceptible to three kinds of risks:

Inflation risk

Stock market risk

Behavioral risk

Inflation Risk

When it comes to inflation, you must ask yourself the following, “How do I invest to maintain my purchasing power and stay ahead of inflation?”

Inflation is the gradual but lethal loss of purchasing power. Currently, we are going through a period of high inflation but historically, the long-term inflation rate has averaged 3%. At just a 3% inflation rate, $1.00 will only be able to purchase $0.41 worth of goods and services at the end of a 30-year retirement. Unless you are willing to reduce your lifestyle and spending habits by about 60% during your retirement, inflation must be dealt with. Fortunately, the risk of inflation can be mitigated by investing in inflation-beating equities. The retirement income plan I will show you later in this blog helps by deliberately designating a portion of a portfolio toward long-term inflation protection.

Stock Market Risk

How do I maintain investment discipline throughout retirement and not make major mistakes during periods of market volatility? Market corrections are part of the investment cycle and should be planned for. Successful investors follow plans and are patient, while unsuccessful investors follow the breaking news and daily movements of the stock market and are prone to panic. Informed investors manage stock market risk by being diversified and patient because they understand every bear market is eventually followed by a bull market. Having a plan in place is the antidote to panic. Knowing what you own, and why you own it, goes a long way towards helping you stay the course during periods of market turbulence.

Behavioral Risk

Two related questions come to mind when considering the behavioral aspects of a retirement income plan:

How do I protect myself from my older self when my financial judgement is clouded by age?

How do I provide the less financially savvy spouse with a plan to follow that will provide for his or her financial needs after my death?

Retirement is not a time for investment experimentation. It’s not a time to be tossed about by every headline on the nightly news or story on the internet. It isn’t a time to change your investments based on irrational exuberance or equally irrational fear. A goal-specific income plan goes a long way toward helping to navigate the emotional roller coaster of investment management now, and especially as you age. It can also be a valuable tool to provide guidance to a spouse upon your death. A date-specific, dollar-specific retirement income plan helps protect your future from perhaps its greatest threat — you.

Create a Framework for Reducing Taxes

From which accounts, or combination of accounts, should I withdraw retirement income from to give myself the most tax-efficient income stream? Should I withdraw from my IRA, my Roth IRA, or my non-retirement accounts? How do I go about managing my Required Minimum Distributions?

Tax-saving opportunities rarely happen by accident. Rather, they come about through careful planning. This is especially true with retirees. Keeping retirees in lower tax brackets throughout retirement can be done by managing withdrawals from pre-tax versus after-tax investment accounts. In other words, the retiree can take income from IRA accounts until they reach the top of a tax-bracket and then take the balance of their needed income for the year from an after-tax account. This is an easy concept to visualize but a little more difficult to implement. What adds to the complexity is that implementing this plan has to integrate with the framework for investing and the framework for distribution sections that I just mentioned. At this point, it might sound daunting to bring all of this together. As we create the income plan in the next section, you will be able to see how all these components can integrate with each other.

Retirement Income Plan Creation

Now that I have explained the retirement income challenge, and what your retirement income plan must address, let me demonstrate how a professional retirement income plan is structured. In 2007, we created our proprietary retirement income plan that we call the Perennial Income Model™. It has helped hundreds of retired families successfully navigate their retirements during the volatile years since its inception. The Perennial Income Model is goal-based and creates the essential frameworks for investing, distributing, reducing risk, and reducing taxation, as previously mentioned.

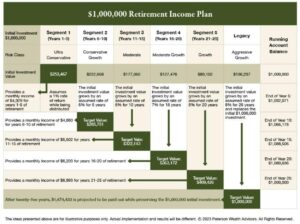

Allow me to introduce the Lee family who we will build a retirement income plan for. Tony and Kathy Lee are both 65 and are ready to retire. They have accumulated $1,000,000 in their 401(k) and their after-tax brokerage accounts. They want to know how they should invest the million dollars and how much income they should expect to receive from that sum of money. They feel a retirement income plan spanning 25 years should be sufficient, and they would like to pass the full $1,000,000 to their children upon their deaths, if possible.

When it comes to making investment decisions, the most important consideration is an investment’s time horizon. In other words, how long will the money be invested? The Perennial Income Model matches the Lee’s current investment portfolio with their future income needs by dividing their money into various investments that have different objectives based upon when a particular segment of their money will be called upon to provide future income. Therefore, the Perennial Income Model will divide the $1,000,000 they have accumulated for retirement into six different accounts. The first five of these accounts are responsible for creating retirement income for five different five-year periods of the Lee family’s retirement. I will refer to the accounts that cover the five-year period of income as segments. So, Segment 1 is responsible for providing the income for the first 5 years of retirement, Segment 2 for years 6-10 of retirement, Segment 3 for years 11-15 of retirement, and so on… until 25 years of retirement are covered.

The sixth segment, or Legacy Segment, is designed to create a fund that will replace the original investment of $1,000,000 to the Lee family at the end of 25 years. This provides money for their heirs or can serve as an insurance policy should they live longer than 25 years or experience large end-of-life expenses like nursing home costs. The accompanying chart shows the retirement income plan being built for the Lee family — I will walk you through it to make sure it all makes sense to you.

The Perennial Income Model Walk-Through

The underlying principle of the Perennial Income Model is matching current investment portfolios with future income needs. Therefore, the money that the Lee’s depend on to provide income in the short-term is invested in conservative investments that provide safety from volatile markets. The money that won’t be needed to create income for a prolonged period is invested into more aggressive investments that keep up with inflation. Segment 1 will provide income for the first five years of retirement. It will be invested into a conservative account that will systematically distribute $4,329 monthly to the Lee’s checking account.

Segment 1’s primary responsibility is safety of principle because it’s sending out a monthly payment immediately; so, this segment is the most conservatively invested. We assume only a 1% rate of return on the money invested in Segment 1. Certainly, in today’s environment retirees can, and should, expect a higher return than 1% on their conservative money. We also expect to outperform the conservative assumptions for the other segments as well. By choosing to underestimate performance, we avoid creating a false sense of security and unrealistic income expectations. Obviously, if the Perennial Income Model works with the conservative assumptions we are using, it will work better as investment performance exceeds these assumptions.

Segment 2 will take over the role of providing monthly income to the Lees once Segment 1 runs out of money at the end of the fifth year. Since the money from Segment 2 will not be needed for at least five years, it can be more aggressively invested than Segment 1, but it can’t be significantly more aggressive. A prolonged bear market could last longer than five years, so the bulk of this money should also avoid volatile investments. That’s why only a 5% return is assumed during the five years it’s invested before being turned into income in year 6.

Segment 3 will be invested for ten years before it will be called upon to create income for years 11-15. Because the money in this segment won’t be used for ten years, Segment 3 is moderately invested in a 50% stock/50% bond portfolio. A conservative 6% return is assumed for this segment.

You can see from the chart, Segment 4 assumes a 7% growth rate and Segment 5 and the Legacy Segment assumes an 8% growth rate. We use these higher growth assumptions because these segments are more aggressively invested. Investments that will not be needed for fifteen years and beyond must invest into a diversified portfolio of equities to keep up these higher growth assumptions. History has shown us that, in the long run, equities have always beaten inflation and have given us superior returns. It’s understood these inflation-fighting segments will experience occasional bouts of volatility that the stock market imposes with regularity. But given the long-term nature of these segments, short-term volatility is inconsequential. The key to making the stock market work for you is to maintain discipline and stay invested during periods of volatility. Following the Perennial Income Model will provide the discipline that is needed.

Harvesting

At first glance, the Perennial Income Model appears to become more aggressively invested as the retiree ages and gets into the latter segments of the plan. Having 80–90-year-old retirees with all their money invested in long-term, aggressive equity portfolios doesn’t make any sense. Fortunately, this is not how this retirement income plan works when the income model is properly managed and “harvested.” In financial terms, the process of harvesting is transferring riskier, more volatile investments into a conservative and less volatile portfolio once the target, or goal, of each segment is realized. The target, or goal of each segment is the number found in the dark green box associated with each segment.

For an example of harvesting, let’s look at Segment 4. You can see that the initial investment in Segment 4 is $127,476 and we know that if this initial investment grows by the assumed growth rate of 7%, it will reach its target, or goal amount by the projected fifteenth year. Segment 4 is invested in a moderate growth portfolio (70% stocks, 30% bonds). According to a study done by Vanguard, the historical return of a moderate growth portfolio has averaged an annualized return of 9.4% since 1926. So, it would be plausible, if history simply repeated itself, that the investment portfolio in Segment 4 would reach its goal of $363,172 before year 15 (at a 9% growth rate, the segment reaches its target in 12 years). Once the target is reached, no matter what year that happens, the investment needs to be harvested and preserved. That means the equities in the segment that have reached their target goal must be moved into more stable and conservative investments.

We have found, the key to successful outcomes is to begin with conservative growth assumptions and then maintain the discipline to harvest portfolios in the segments when they reach their targets.

Five Insights to Point Out:

Notice the account balance stays roughly the same throughout retirement (see the far-right column of the chart). People often assume that as segments are liquidated, the overall portfolio balance is going down, but that’s not the case. Recall that as the early segments are being liquidated, the later segments are invested and growing.

Notice that the retirement income plan is projected to automatically increase the Lee’s income every fifth year by an annualized 2.6% rate to help offset the effects of inflation.

To keep things simple and to help you to understand how the Perennial Income Model works, I have not incorporated any other sources of income such as Social Security or pensions into our example. But, for tax planning purposes, projected Social Security, pension, and other sources of taxable income should be incorporated into the retirement income stream projections. Once the income stream is created by adding all sources of income, thoughtful consideration should be made to determine which type of account (IRA, Roth IRA or after-tax account) should be allocated into the various segments for maximum tax efficiency.

Assumed growth rates are purposefully overly conservative. Historically, the S&P 500 has averaged more than 10%, and the largest assumed growth rate used in the most aggressive segment is only 8%. If you feel that these assumed growth rates are not realistic, you can always adjust the income plan to run at lower or higher growth assumptions. The Perennial Income Model uses conservative growth assumptions within the retirement income plan in hopes that the target for each segment is reached prior to the date it’s needed to provide income.

Please look at the bottom line of the chart. Based upon these conservative assumptions, the Lee family will receive $1,674,433 of income during their 25-year retirement and leave $1,000,000 to their heirs.

Conclusion

I end with the question that all new retirees and those approaching retirement need to ask themselves, “Will I outlive my money, or will my money outlive me?” Without knowing anything about your finances, I can tell you that you will be much more likely to have your money outlast you if you follow a plan. Your retirement income plan should be goal-based and should serve as a guide to your financial decision-making for the rest of your life. It should drive your investments, withdrawals, and even influence your spending and gifting decisions.

The Perennial Income Model appeals to those seeking a logical, goal-based roadmap for investment management during retirement. It reduces the retirees’ need to be anchored to the daily movements of the stock market which, in turn, will provide them with greater peace of mind and will make them less vulnerable to making the irrecoverable investment mistakes that so many retirees make.

Retirees that follow the Perennial Income Model understand why they are invested, when they will need a specific portion of their investments to provide future income, how much they can safely withdraw, and how their dollars will need to be invested to accomplish their goals. They will also realize a more tax-friendly way to navigate retirement. The Perennial Income Model is designed to provide a secure stream of income in the short-term, while providing an inflation-adjusted stream of income for the retiree’s future.

Hopefully, you can now see that there is so much more to planning retirement income streams than buying an annuity and more to consider than following generic and overly simplistic rule of thumb guidelines to manage your finances during retirement.

My hope is that this blog has opened your eyes to a better way to invest during retirement and that you might be able to incorporate some of the ideas found in this blog so you might face your financial future with confidence and have the peace of mind to free you to pursue your retirement dreams.

The Perennial Income Model is explained in greater detail in my book “Plan On Living”. You can get a complimentary copy of my book and get a better understanding of the services that we offer by visiting here.

An emergency fund is a portion of money set aside to be used as a buffer in the event of an emergency or for an unforeseen expense. During the accumulation phase of life, or the years in which a household is reliant on a paycheck and actively saving toward retirement, an emergency fund provides a safety net to balance the budget during events such as loss of work, an expensive medical bill, or a car repair. In every personal finance textbook, you will find details on how to best manage an emergency fund. However, most of these texts focus on the accumulation phase of life. They aren’t focused on applying these beneficial principles to retirees. So, let’s go over the details of an emergency fund for retirees.

How much should I have in an emergency fund?

There is a rule of thumb that is used when determining how much a household should have in an emergency fund. The guidance is to have at least three to six months’ worth of expenses set aside. This can be a good benchmark to measure yourself against. But the problem with a rule of thumb is that everyone’s individual situation is different and may require more customization.

Calculating an emergency fund during retirement is different than during accumulation. For instance, the risk of losing your job when you’re retired is zero percent. However, in most cases, this does not completely eliminate the risk of income loss. You must determine, based on your own cash flow risks, what amount is right. For example, a retiree with multiple rentals and a history of renter turnover will require more cash on hand than a retiree whose only income source is from Social Security and a steady pension.

Where should you invest your emergency fund? How much cash should I have on hand?

The goal of an emergency fund is not to earn the highest return possible. It is to have the funds accessible when needed. A common place for an emergency fund to be kept is in a savings or money market account. You can do this at your preferred bank or credit union. Online banks that pay higher interest rates can also be a good choice. Any of these options will work, as long as your money is easily accessible.

Do not keep your entire emergency fund in hard cash. Having a limited amount on hand in your home is reasonable. However, there are added risks in having large sums of cash in your home.

Once you have determined the amount for a comfortable emergency fund, you may need to add or subtract from your current account. If you need to increase your emergency fund, the best way to do this is by adding a portion of your monthly income to the fund until you have the desired balance. Anytime you use your emergency fund, immediately work toward increasing it back to the desired amount.

It can also be common for retirees to accumulate large sums of cash in savings accounts. These are much greater than an adequate emergency fund requires. During the accumulation phase, the guidance is to put 15 – 20% of our income away into savings. In retirement, this mindset changes. Keeping extra savings in the bank, in excess of your emergency fund, can be a missed investment opportunity. This will hamper your ability to keep your investments up with inflation. If you have a balance in your bank account on top of your emergency fund needs and what you might reasonably spend in a short period of time, consider investing these funds for a greater opportunity for growth. You should also consider reducing income from sources such as taxable retirement accounts to avoid paying taxes on this unspent income just to have it accumulate in the bank.

A good question to ask yourself if you are in this situation is “when do I plan on spending this money?” If it is more than five years out, investing the funds in a diversified portfolio will result in greater growth opportunities. Talk to your advisor to determine the right investment allocation.

Conclusion

Though the amount and use of an emergency fund slightly change for individuals moving from the accumulation phase to the retirement phase of life, it is still an important part of a retiree’s financial household. Having too little or too much in savings for a rainy day could cost you thousands of dollars over the course of your retirement. Talk to one of Peterson Wealth Advisors’ Certified Financial Planners with your questions about an emergency fund for retirees and start your retirement income planning with our Perennial Income Model.

Entering retirement can be both thrilling and intimidating at the same time. The thought of “hanging up the cape” and permanently leaving the workforce behind can be viewed as unburdening and relieving to one individual, but completely frightening to another. Regardless of the viewpoint you have on retirement, it will undoubtedly come with new challenges and troubles to overcome. Among the different problems to solve for retirement, one of the biggest challenges is that of early retirement health insurance options.

For those age 65 and older, or certain younger individuals with disabilities, Medicare has you covered. Medicare is the country’s health insurance program managed by the federal government. Once you enroll, there is very little management that you have to do throughout retirement.

But what about those who retire earlier than age 65? An early retirement is certainly achievable, but requires careful planning, especially when it comes to your healthcare. This article will enlighten you on the different healthcare options available for early retirees, with a focus on the Marketplace. If you are not familiar with what the Marketplace is, don’t worry, we will get to the details soon.

Health Insurance Options for Early Retirees

If neither you nor your spouse will be covered through an employer plan, fear not! There may be more options than you think. Below is a summary of a few options. I highly recommend speaking with your financial advisor about which route makes the most sense for you.

COBRA

A law that allows employees and their dependents to keep their group coverage from their former employer’s health plan. This coverage can last for 18 months after termination from the employer, but beware, this can be very costly.

Medicaid

Though unlikely for some retirees to qualify due to the low-income requirements (i.e., in Utah, coverage is available for those with household incomes up to 138% of the federal poverty level), this may be the cheapest option for those who do qualify. However, many doctors don’t accept Medicaid, so you may have to change your primary providers if you qualify for coverage.

Christian Healthcare Ministries

This is not traditional insurance, but rather a Christian-based method of sharing the costs with others around you. Each member pays a monthly premium, and those funds are used to help other members cover their healthcare costs.

The Marketplace

Finally, we have the Marketplace, which tends to be the route most early retirees take. For this reason, I want to expound upon how the Marketplace insurance really works.

The Marketplace – What is it?

In March of 2010, the Affordable Care Act (sometimes called Obamacare) was passed with the goal of making health insurance more affordable. The law provides individuals and families with government subsidies (otherwise known as premium tax credits). This helps lower the costs for households with an income between 100% and 400% of the federal poverty line. As a reference, in 2022, 400% of the federal poverty level for a retired couple is $73,240. The federal government operates the Health Insurance Marketplace, or “the Marketplace” for short. This is an online service that helps you enroll for health insurance. You can access the Marketplace at HealthCare.gov.

How does the Marketplace work?

First and foremost, I recommend you work with a trusted, licensed health insurance agent to help you navigate the waters of the Marketplace. Especially if you’ve only ever received health insurance through your employer. There is no additional cost to you to use an agent – they will be compensated by the insurance company directly. You can then tell the agent any specifics you are looking for with your coverage (such as certain doctors, hospitals, etc.). They can help narrow the available plans down to your liking.

That being said, let’s look at how this actually works.

You can enroll in health insurance during open enrollment, which generally runs from November 1st to December 15th. This is for coverage starting January 1st of the following year. You also have the option to enroll during a special enrollment period. This is based upon major life events, such as a change in household or residence.

You’ll be rewarded with a special enrollment period when you’re looking for health insurance options as an early retiree. Don’t feel like your retirement date needs to line up with the open enrollment period. During this special enrollment, you’ll have a 60-day window to enroll through the Marketplace.

During enrollment, you will fill out an application with basic personal information. Included with this application, you will give them your best estimate of what your income will be for the coming year. The Marketplace uses your Modified Adjusted Gross Income – MAGI – to define “income.”

When evaluating early retirement health insurance options, it’s important to understand how Marketplace subsidies work. The Health Insurance Marketplace bases eligibility on your projected income for the upcoming coverage year — not your prior year’s income. This distinction is especially important when considering health insurance options for early retirees, since retirement often significantly reduces taxable income.

For 2026 coverage, if your projected household income falls between approximately 100% and 400% of the federal poverty level (FPL), you may qualify for a federal premium tax credit to help lower the cost of your insurance premiums. If your income exceeds 400% of FPL, you generally will not qualify for a subsidy and must pay the full premium yourself.

The temporary subsidy enhancements created under pandemic-era legislation — which allowed households above 400% of the poverty level to receive assistance — expired after 2025. Unless new legislation is passed, Marketplace subsidy eligibility for 2026 and beyond follows the original Affordable Care Act structure. Because of this, managing your projected retirement income carefully can play a significant role in keeping your early retirement health insurance costs affordable.

What happens if your income isn’t exactly what I put on the application?

The answer is that you will reconcile any differences when you file your taxes.

If your income was less than what you projected, you’ll get a credit as you qualified for more of a subsidy throughout the year. If your income was more than what you projected, you will have to pay some of that subsidy back. Generally, this isn’t that big of an issue unless you projected your income to be less than 400% of the poverty level, but it was actually more. In this case, you are required to pay back the entire subsidy. Even if your income was only $1 more than the threshold.

For this reason, I suggest consulting with your financial advisor to pinpoint what your income will be through your early years of retirement. I also suggest you speak with your advisor about potential planning strategies available to control your Modified Adjusted Gross Income, as there are certain strategies that can help you qualify for a subsidy while enjoying the income you desire throughout retirement. For an example of how this might work, Mark Whitaker wrote an article in 2020 describing a case study that explored these strategies.

As far as the plans that are available, the Marketplace ranks them in four different categories. These categories are Bronze, Silver, Gold, and Platinum. The Bronze plans typically tend to have the lowest premiums, but they are also the most catastrophic plans. This means they have high deductibles and out-of-pocket maximums. Gold and Platinum plans typically tend to be better plans as far as coverage, but have higher premium costs. Again, working with an agent can help you navigate which plan is best for you.

Frequently Asked Questions About Early Retirement Health Insurance Options

Choosing the right early retirement health insurance option can significantly impact your long-term retirement plan. Below are answers to common questions about health insurance options for early retirees and how to manage coverage before Medicare eligibility.

1. What are the best early retirement health insurance options before Medicare?

If you retire before age 65, you’ll need coverage until Medicare eligibility. The most common early retirement health insurance options include:

COBRA continuation coverage from your former employer

ACA Marketplace (Affordable Care Act) plans

Coverage through a spouse’s employer plan

Part-time employment with health benefits

Private individual insurance plans

For many early retirees, the ACA Marketplace is the most flexible and potentially affordable option, especially if income qualifies for premium tax credits.

2. How do health insurance options for early retirees work with the ACA Marketplace?

Marketplace plans determine subsidy eligibility based on your projected income for the upcoming year, not your prior year’s earnings.

For 2026 coverage, households with income between approximately 100% and 400% of the federal poverty level (FPL) may qualify for premium tax credits. If income exceeds 400% of FPL, subsidies generally are not available under current law.

Because retirement often reduces taxable income, careful income planning can significantly lower health insurance premiums.

3. Can early retirees qualify for government subsidies?

Yes — many early retirees qualify for premium tax credits through the ACA Marketplace.

Subsidy eligibility depends on:

Projected Modified Adjusted Gross Income (MAGI)

Household size

Federal poverty level thresholds

Strategically managing withdrawals from retirement accounts (such as IRAs, Roth IRAs, and brokerage accounts) may help maintain income within subsidy-eligible ranges.

4. Is COBRA a good health insurance option for early retirees?

COBRA allows you to continue your employer-sponsored coverage for up to 18 months (sometimes longer in certain circumstances).

However:

You pay the full premium (including the employer portion)

It is usually more expensive than Marketplace options

It is temporary and not a long-term pre-Medicare solution

COBRA can serve as a short-term bridge to Medicare or to the next Marketplace enrollment period.

5. How much does health insurance cost in early retirement?

Costs vary widely depending on:

Age

Location

Plan type (Bronze, Silver, Gold)

Income (which affects subsidy eligibility)

Without subsidies, premiums for early retirees can be substantial. With subsidies, however, coverage may be significantly reduced — especially for households near the lower end of the income range.

This is why income planning is one of the most important factors when evaluating early retirement health insurance options.

6. What happens when I turn 65?

Once you turn 65, you become eligible for Medicare.

Many early retirees structure their health insurance decisions as a bridge to Medicare, choosing options that provide stable coverage until Medicare enrollment begins. Planning ahead helps avoid coverage gaps and late enrollment penalties.

7. What is the biggest mistake early retirees make with health insurance?

One of the most common mistakes is failing to coordinate retirement income planning with Marketplace subsidy rules.

Large IRA withdrawals, Roth conversions, or capital gains in a single year can push income above the subsidy threshold — dramatically increasing premium costs.

Proactive tax planning can help maintain eligibility and reduce overall healthcare costs during early retirement.

What Health Insurance is Available for Early Retirees?

There is more to the Marketplace and the other health insurance options for the early retiree mentioned than can be discussed in this article. Hopefully, this provides you with a framework of the options you have as an early retiree. Early retirement is achievable for those who are prepared and understand how their healthcare needs can be met.

Warren Buffet once called the babies born today “the luckiest crop in history” because they are expected to live longer and enjoy greater prosperity than any previous generation. I believe it would be a fair assumption to add that the baby-boomer generation is the “luckiest crop” of retirees to have ever lived. Today’s retirees are healthier, wealthier, happier, safer, freer, more educated, more equal, more charitable, and more technologically advanced than any previous generation.

4 Common Threats to Retirement Savings

Ironically, the wonderful advancements that current retirees are blessed with are also the root of the problems that retirees will face. Longevity, inflation, and the retiree’s individual responsibility to manage their own investments will be the challenges that this generation of retirees will have to grapple with.

1. Longevity

Not only are we living better, we are also living longer. Therein lies the challenge: We are living too long. Life expectancies are steadily climbing. According to the Social Security Administration, a couple who is currently 65 years old have a 48% chance that one of them will live to be the age of 90.

Because of long life expectancies, many retirees face the very real risk that they will outlive their money if they don’t plan for a lengthy retirement. Planning on living to the average life expectancy is not enough. It is best to plan on living longer than your life expectancy, because life expectancy estimates the average time a person will live. To be certain, some people will die before their life expectancy, but some will live beyond, sometimes many years beyond, their projected life expectancy.

2. Inflation

Longevity is the catalyst for today’s retirees’ second challenge: their dollars are shrinking.

Every day, the purchasing power of the retiree is eroding as goods and services are getting more expensive. Although inflation has always existed, no previous generation has had to deal with it to the extent that today’s retiree does. Our parents and grandparents lived ten or fifteen years past retirement, inflation never had time to develop into a problem for them.

A retirement lasting thirty years or more is a game-changer. Inflation isn’t something that may happen, it will happen. In our opinion, inflation has confiscated more wealth, destroyed more retirements, and crushed more dreams than the combined effects of all stock market crashes. Historically the average inflation rate has been more than 3% annually. To put that into perspective, at a 3% inflation rate, a dollar’s worth of purchasing power today will only purchase forty-one cents worth of goods and services in thirty years from now.

Inflation poses a “stealth” threat to investors as it chips away at real savings and investment returns. The goal of every investor is to increase their long-term purchasing power. Inflation puts this goal at risk, because investment returns must match the rate of inflation just to break even. An investment that returns 2% before inflation in an environment of 3% inflation will actually lose 1% of its purchasing power. This erosion of purchasing power might seem incidental, but this type of loss, compounded over the duration of a retirement, is life-changing.

Dollars invested into money market accounts, certificates of deposits, fixed annuities, and bonds, never have, and never will, keep up with inflation. Uninformed, anxious, stock market-leery investors that depend on these types of investments for long-term growth may be insulating themselves from stock market volatility, but they are committing financial suicide, slowly but surely. To make matters worse, the paltry gains associated with these products must be taxed, which makes it that much more unlikely that they will be able to preserve purchasing power.

In the current environment of huge government budget deficits and spending, it is likely that inflation will continue to rise at least at the same pace as its historical average. Given the one-two punch of longevity and inflation, it is imperative that retirees are mindful of inflation as they invest and plan for the future.

3. Investment Management Risk

A third challenge for retirees to be aware of is the personal responsibility they now have to manage their own investments.

During the last couple of decades, a subtle transfer happened. The responsibility to provide retirement income shifted from the employers to the employees. The popular pension plans of the past, which guaranteed a lifetime of monthly income to retired employees and their spouses, are disappearing. Pensions have been replaced by 401(k)s and other similar plans that all place the burden of funding, managing, and properly distributing investments to last a lifetime, squarely on the backs of the unprepared employee. Like it or not… you, not your employer, hold the keys to your financial future.

An annual study done by DALBAR, Inc. shows that the average stock fund investor managed to capture only 60% of the return of the stock market over twenty years. Ouch! The largest contributing factor that explains this blatant underperformance was the investor’s own behavior. It appears that the typical investor followed the herd mentality, buying when stocks were high and selling in a panic when stocks were low. Seldom was the investor guided by a comprehensive investment plan. Consequently, little or no discipline was demonstrated. What is most concerning, is that for the most part, the investor failed at the easy part of investment management: the accumulation phase.

4. Retirement Income Distribution Risk

When people enter retirement, they also enter the distribution phase of investment management. In other words, they start withdrawing their investments. The distribution phase is much more difficult to manage than the accumulation phase. In the distribution phase, it is still crucial to know how to properly allocate and invest a portfolio, but additional complexity is added to the mix. Therefore, income-hungry retirees need to know how to create a distribution plan that will provide a stream of income that will last until the end of their lives. They need to create and then follow a Retirement Income Plan.

Retirees need to be kept informed in order to make the best financial decisions. It is also important to work with a financial professional that specializes in retirement issues and that is a fiduciary who puts the retiree’s best interest ahead of their own.

Is there any way to make sure our heirs use the money wisely?

All these questions can be answered by crafting a good estate plan. Many people are familiar with, or have at least heard of, the legal documents that are used in an estate plan such as a will, trust, or power of attorney. These legal documents are critical to a good estate plan. However, if these documents are hastily thrown together without first defining what it is you are trying to accomplish, and who it is that you want to carry out your wishes, the outcome can be less than desirable.

Five things to consider when creating an estate plan

1. Questions that need to be answered to create an estate plan

If I become incapacitated, who do I want to appoint to look after my financial and legal affairs?

Who would I want to make medical decisions for me if I get to the point where I can’t make them for myself?

What end-of-life decisions do I want to make now and/or who would I want to make life-ending decisions for me?

When I pass away, what do I want to happen with my possessions and assets?

Are there any special considerations (needs of a disabled child) or preconditions that I want to put in place for my beneficiaries?

2. Choose one or more people that you fully trust to follow your instructions and carry out your wishes

You should choose someone with integrity. When choosing one of your children to fill an important role in your estate plan, it is helpful to choose one who works well with others and can build consensus. Conflict and hurt feelings are common between siblings after the death of a parent. Therefore, choosing the child who can cross divides with maturity and grace is more important than one who happens to be good in business or simply choosing a child because they happen to be the oldest.

Roles in a typical estate plan:

Executor: The person who administers your estate/will

Trustee: The person responsible for trust administration

Power of attorney: The person responsible to act on your behalf for legal and financial matters when you are unable to do it for yourself

Medical power of attorney: The person designated to make medical decisions on your behalf when you are incapable of making them yourself

These roles can be filled by a single person, or by multiple people working together on your behalf. Additionally, each of these roles can be filled by different people. It is also wise to consider choosing a backup for each of these roles if your first choice is unable or unwilling to serve in that capacity.

3. Meet with qualified professionals to help you implement your estate plan

You will need to work with a licensed attorney to draft any legal documents that are required to carry out your wishes. In partnership with an attorney, your financial planner can help coordinate the attorney’s advice with other areas of your financial plan. Your financial planner can be very helpful by making sure you update your retirement account beneficiaries and that your investment accounts are properly titled to make sure they are in accordance with your overall estate plan.

4. Clear communication is a must when it comes to estate planning

Your son or daughter shouldn’t learn that you have chosen them to decide when to end lifesaving medical care when you are in the hospital. There may be good reasons to not share all the details of your estate with your family before your death, however, walking through your general intentions and the roles each person is being asked to fill will help prepare those involved for the great responsibility you are asking them to carry out.

5. Review your estate plan often

There are common reasons why you should consider regularly updating your estate plan:

It has been several years since you last reviewed your estate planning documents

There have been major changes in estate or tax law

There have been changes in your family like deaths, divorce, or disability that could impact your beneficiary’s designations as well as your potential choices for trustee, executor, etc.

After major changes in your financial situation

Spending a small amount of time to periodically review your estate plan can help you avoid major mistakes down the road. Reviewing your estate plan will also ensure your plans still make sense amid life changes.

It is uncomfortable for most of us to have to make decisions regarding our own death or disability. Additionally, finding an attorney, dealing with all the documents, changing beneficiaries, and transferring titles to property can make the estate planning process overwhelming, and therefore it is often put off. Your estate planning attorney and financial advisor have been through this process many times before and can carefully, and easily, walk you through the steps of creating an estate plan.

An estate plan outlines the wishes for your care while you are alive and frees your family members from the burden of second-guessing what you would have done with your estate after you are gone. A well-thought-out estate plan is truly a gift to your family and helps with retirement income planning.

Questions? Learn more about our Perennial Income Model™ or click here to schedule a complimentary consultation to review your situation with one of our experienced advisors!

A fiduciary is a person or organization that acts on behalf of another person or persons, putting their client’s interest above their own in all instances. Being a fiduciary requires being bound, both legally and ethically, to act in their client’s best interest. In essence, they are the guardians of their client’s money.

Can a fiduciary receive commissions?

Commissioned salespeople are not considered fiduciaries because they are representing a product or a company, not the individual to whom they are selling a product, and they are not bound by the higher ethical standard of a fiduciary. Commission salespeople follow a different suitability standard in which the transaction must be suitable for a client, not necessarily the best solution. The commissions they earn can create a huge conflict of interest which effectively eliminates them from the fiduciary standard.

All too often, individuals trust advisors that promote themselves as fiduciaries, only to get talked into buying high-commission/high-fee annuities or real estate investment trusts by these same advisors as these advisors fail to live up to fiduciary standards. Sadly, many investors fall prey to the unethical, yet legal, practices of financial advisors who promote themselves as trusted fiduciaries as a door opener to selling expensive, inappropriate, big commission products to the unsuspecting public.

Are all financial advisors fiduciaries?

No, not all financial advisors are fiduciaries.

Unfortunately, some investment advisors are allowed to wear multiple hats at the same time, which allows them to be fiduciaries for a part of a client’s money that they manage, and a commissioned salesperson for the balance of the client’s money. It is not right, it makes no sense, but that is how it works.

Who regulates – or better said, doesn’t regulate – Advisors?

The Securities and Exchange Commission (SEC) typically oversees the activities of the fee-based fiduciary while another regulator, the Financial Industry Regulatory Authority (FINRA) oversees the activities of the broker-dealers who are typically those persons and firms that are commissioned salespeople. Additionally, the State Insurance Commissioners oversee the sale of commission-paying insurance products such as annuities within their respective states.

The problem lies in the fact that the SEC is only interested in the activities of the advisors relating to the advisor’s roles as fiduciaries and does not pay any attention to the non-fiduciary sales activities that are being carried out by the advisors.

So, the sale of commissioned securities and insurance products by a fiduciary is not their concern as they view these activities outside of the scope of their jurisdiction. The deception takes place when advisors advertise themselves as fiduciaries, draw clients into their offices, then act as fiduciaries for a small amount of the client’s assets (10%) and then proceed to sell the client big commission products that are not in the best interest of their clients with the rest (90%) of the client’s money.

As I listen to the radio and see advertisements online, it is usually these bait and switch types of advisors that are promoting themselves as fiduciaries. Buyer beware, you need to do your homework.

Is my advisor a Fiduciary?

1. Check out the firms Form ADV and CRS

Form ADV and CRS are the uniform documents filed by investment advisors to register with the SEC. They will let you know how a firm is compensated and will identify conflicts of interest such as receiving commissions in the sale of investments and/or insurance products. You can find a firm’s Form ADV and CRS on the SEC website. If the firm, or advisor you are investigating, earns a commission by the selling of an investment or insurance product then I would suggest avoiding that advisor. They may be “fee-based” which means they act as a fiduciary for some of the client’s money they manage but in the end, they are commissioned salespeople.

2. Know that any product that has a surrender charge, or limits your access to your own money, pays a commission to a salesperson

When an insurance agent sells an annuity, they get paid an upfront commission typically of 6-7%. So, if the agent talks somebody into investing $100,000 in an annuity, the insurance company pays the agent a 6% commission or $6,000. So how does the insurance company protect themselves from losing money on this transaction?

Insurance companies place a surrender charge on the annuity that keeps the purchaser from liquidating the annuity for a specified number of years, or at a large cost if the annuity is surrendered prior to when the stated surrender charge expires. This allows the insurance company to recoup the upfront $6,000 commission they paid by collecting large management fees for a number of years or the investor reimburses the insurance company in the form of a surrender charge if they surrender the product early.

You are unlikely to get stung as long as you never place your money into a product that charges a fee to withdraw your own money or that imposes a timeframe that limits your ability to withdraw your money.

3. Search Google for a list of “fee-only” investment firms in your area

“Fee-based” advisors are not always true fiduciaries as part of their income comes from selling commission-paying products. Fee-only advisors are compensated by an agreed upon fee and don’t accept, or are even licensed to receive, commissions.

Unfortunately, I don’t see the regulatory environment changing anytime soon and vulnerable investors will continue to be duped by advisors, who claim to be fiduciaries but fail to act as fiduciaries by selling high commission investments and annuities to the public. This travesty will continue as long as the multiple regulatory bodies and insurance commissioners limit their focus on their own perceived jurisdictional responsibilities while ignoring the big picture of what is taking place with the client’s investment portfolios.

If you want an advisor that is truly a fiduciary, one that always acts in your best interest, then it’s critical to understand the potential conflicts of interest that exist in the investment industry before hiring any advisor. My best advice is that you should limit your search for a fee-only advisor whose investment philosophy matches your own.

Bob and Patricia are 60 years old and would love to retire as soon as possible. It’s not uncommon to meet people like Bob and Patricia who have been saving diligently, setting money aside into their 401(k)s, making wise investments, and living below their means with a desire to transition into retirement as early as possible. Unfortunately, health insurance for them to retire before age 65 can now cost as much as $2,000 per month for a high deductible health insurance plan, even for someone who has significant savings, this additional expense can make early retirement unaffordable.

In the past, many people were able to leave the workforce and continue to receive health insurance through a former employer. These retiree health insurance plans would bridge the gap between the time that someone left the workforce and the time they began receiving Medicare benefits at age 65. Unfortunately, most of these benefits, along with other retirement benefits like generous pensions, have gone the way of the Dodo bird.

How to Pay for Insurance in Retirement

If you are one of the few that still have these benefits available to you, count yourself very fortunate. So, is there a way to retire before age 65, and purchase affordable health insurance? The answer is yes! But it requires special planning.

The Affordable Care Act

The Affordable Care Act, also commonly known as, “Obamacare” contains a provision that provides health insurance subsidies to Americans below certain income levels. To qualify for a health insurance subsidy or discount, your household income cannot be more than four times the federal poverty line. The federal poverty line is based on the number of people in your household. Looking at Table 1., four times the federal poverty line ranges from $49,960 in 2020 for a household of one, all the way up to $138,360 for a household of six. Since Bob and Patricia have a household of two, they would need to have an income below $67,640 in 2020 to qualify for a subsidy, and the subsidies are significant.

For example, Bob and Patricia, Utah residents, would receive $1,345.29 per month if they reported an income of $65,000 for the year. If Bob and Patricia were to choose a high deductible Bronze plan (See Table 2.) that would typically cost about $1,227 a month. Applying their subsidy of $1,345.29, they wouldn’t have to pay a monthly premium. Now let’s say they select a gold plan that costs $2,403 per month; they would only have to pay $1,058 after their subsidy is applied. That’s a savings of over $16,000 a year in healthcare expenses.

Table 2. EXAMPLES OF HEALTH INSURANCE PLANS AND IMPACT OF SUBSIDIES

Plan

Bronze Plan

Silver Plan

Gold Plan

Monthly Premium

$1,227.40

$1,856.76

$2,403.36

Subsidy

$1,345.29

$1,345.29

$1,345.29

After Subsidy

$0.00

$511.47

$1,058.07

Quotes ran August 2020 at www.healthcare.gov. Based on a household of two with an annual modified adjusted gross income of $65,000

You might be thinking, this sounds great, but I’m not sure I’m willing to restrict myself to only living on an amount that’s below the threshold to qualify for these discounts.

Well, here’s where the planning comes in. The discounts are based on your modified adjusted gross income (MAGI). We need to be careful not to confuse this with cash flow coming into the household.

Modified Adjusted Gross Income (MAGI)

Let’s look at how the tax code defines modified adjusted gross income for health insurance – to determine your modified adjusted gross income, the tax code looks at your adjusted gross income (AGI) and adds back in a few income sources that are normally not included. Three of the most common income sources that must be added back into AGI to come to the MAGI calculation are:

Excluded foreign income

The Non-taxable portion of Social Security

Tax-exempt interest

Once MAGI is calculated, there are ways to keep your income below the 400% of the federal poverty line income limit that would allow you to qualify for subsidies and still have the monthly cash flow you would like.

Let’s return to the case of Bob and Patricia and see how this would work. Let’s say that Bob and Patricia have saved $3,000,000 for retirement. These savings include pre-tax accounts like 401(k)s and IRAs, tax-free accounts like Roth IRAs, and after-tax brokerage investment accounts. Bob and Patricia decide that they would like to have $100,000 per year in income. Bob and Patricia can control how much of their $100,000 income are included in their AGI by choosing which accounts they take distributions from.

Example: Bob and Patricia decide to take out $50,000 from Bob’s IRA over the year for income. They then supplement their IRA income by taking out $50,000 from Bob’s after-tax brokerage investment account. Bob is careful not to sell stocks that have embedded capital gains, which would be added to their MAGI. This means that Bob and Patricia will be able to enjoy $100,000 per year of income but only report about $50,000 on their taxes. This would allow them to then qualify for the significant health insurance subsidies.

This example doesn’t consider things like capital gains, interest, or dividend income that would likely be applicable in their case. These items need to be considered, so careful planning is required. However, the point remains that this strategy would allow someone to enjoy the amount of income they prefer, while simultaneously qualifying for significant subsidies for health insurance.

One last note on health insurance subsidies for early retirees. When you apply for health insurance during open enrollment, you will have to estimate your income or MAGI for the following year. For Bob and Patricia, this means that they would state their income on the application as $50,000 using the numbers from the example above. You might ask, what if my income ends up being different from my estimate? Any difference in income between your estimate and actual income will be reconciled when you file your taxes for the following year. If your actual income is higher than the estimate you used on your application, you would be required to pay back a portion of the subsidy you received. If your actual income is lower than your estimate, you may be eligible for a higher subsidy, which would be paid to you as a tax credit.

In my experience, this isn’t much of an issue unless your actual income is so high that you wouldn’t have qualified for a subsidy at all. In this case, you would be required to pay back the entire subsidy you received throughout the year. In Bob and Patricia’s case, this would mean coming out of pocket $16,000 to pay back the subsidies they received based on their income estimates.

Careful planning is the key. If you understand and follow the rules you can receive significant benefits, if you mess up, you’ll go from thinking you’ve saved money to having to pay out large sums at tax time.

There are other aspects of this planning strategy for early retirees that I haven’t mentioned in this article, but this is a good start. I would recommend you consult with a qualified financial professional that is knowledgeable in the detailed tax rules associated with the Affordable Care Act before attempting to implement this strategy. If you’ve prepared well, early retirement is an achievable goal. Health insurance is a significant expense, that can derail your ability to retire early. However, there are powerful retirement income planning strategies available to the well-informed to help you retire with confidence.

Social Security is the anchor of a retirement income plan

Past generations took little thought regarding how they would maximize their Social Security benefits. After all, it really didn’t matter how and when benefits were claimed if the retiree lived only a short time after retiring. Today, with the real possibility of living three decades without a job or paycheck, retirees need to do all they can to squeeze the most out of Social Security.

Over its almost eighty years of existence, Social Security has evolved. It now consists of hundreds of codes, and tens of thousands of pages of rules and regulations. Because of this, most eligible recipients do not understand the benefits they are entitled to receive. Consequently, there are millions of dollars of Social Security benefits left on the table each year.

While Social Security is complicated, it is essential to make informed choices regarding both when and how to apply. This will ensure you will get the most from the system. After all, you and your employers have contributed to this future source of monthly income since the day you started working. Understanding how the system works and creating an individualized plan to maximize this valuable benefit could mean the difference in hundreds of thousands of dollars of retirement income.

Five important benefits of Social Security:

1. Predetermined amount of income

By the time you come to the end of a career, your Social Security income amount is pretty well known. The benefit amount is based on both your earnings history and when you decide to apply for benefits. The accuracy of the benefit estimation makes it easy to build the rest of your retirement income plan around a reliable number.

2. Reliable income

Once you start getting Social Security benefits, the amount of income you will receive is set. It is highly unlikely that reforms to the system will cause benefit cuts.

3. Income that lasts for a lifetime

Social Security is one of the few sources of income that can be relied upon for a lifetime. It is an especially valuable benefit considering the long life expectancies of today’s retirees.

4. Inflation-adjusted income

Social Security benefits are increased each year based on the previous year’s inflation rate, which is measured by the consumer price index. These cost-of-living adjustments help retirees keep up with the ever-increasing cost of goods and services.

5. Survivor benefits

Although Social Security checks stop at the death of the recipient, monthly benefits can continue to be paid to surviving spouses and minor dependents.

The Sustainability of Social Security

There is a lot of misinformation that surrounds the sustainability of Social Security, but the boring truth is that Social Security is not going away anytime soon. Each year, the Congressional Budget Office (CBO) reports to Congress the fiscal status of Social Security. The latest report states that if no changes are made to the system, the Social Security Trust Fund, along with income collected from our taxes, will allow Social Security to pay all its obligations until the year 2034. If no adjustments are made to the Social Security system between now and 2034, there will only be enough money in the system to pay 79% of the promised obligations after 2034.

Minor adjustments to the system now could extend the viability of Social Security for years into the future. Raising the age requirements of future claimants, changing how the cost of living adjustment is calculated, or raising the maximum earnings subject to the Social Security tax are all viable measures that should be considered to strengthen Social Security. To date, these common-sense solutions have not been implemented because anytime a politician has suggested a change to Social Security it has proven to be a political boondoggle. Like any financial problem, the sooner the future projected shortfall is addressed, the easier it will be to manage. Making decisions about claiming Social Security benefits based on the false assumption that these benefits are disappearing is both dangerous and irresponsible.

With the ever-changing rules and regulations of Social Security, a list of commonly asked questions such as how much you can expect to receive, spousal benefits, and when to apply can be found here. The answers to these questions will frequently be updated to help you navigate the minor changes to the current Social Security system.

You can also visit the government Social Security website and select the ‘Retirement’ tab to receive assistance on things such as estimating your benefits, requesting a Social Security Statement, and applying for benefits online.

Social Security is responsible for 42% of today’s retirees’ income. While it does not provide enough income to retire on, it does provide a solid foundation upon which a sound retirement income plan can be built. A little time and effort can pay significant dividends when deciding when, and how, to receive Social Security benefits.

If you’re approaching retirement age, you may be considering a move to a more retirement-friendly state, particularly if your current state of residence imposes numerous taxes on social security, pensions, and other retirement income. While making the decision to relocate is not something that can be done lightly, there are a variety of options available nationwide that may allow you to retain more of your retirement income.

Of course, taxes alone are not the only reason to relocate; climate, proximity to health care, cost of housing, ability to create an emergency fund, and property taxes all need to be taken into consideration.

What are the Most Tax-Friendly States for Retirees?

What are the most tax-friendly states for retirees? Below, we’ve gathered a list of states that provide a great environment for those looking to retire.

Alaska – While it may not be the first choice of retirees, Alaska offers an excellent environment for retirees with neither Social Security nor pensions taxed. Another advantage is the lack of state income tax and sales tax.