Smart Year-End Tax Moves for Retirees – (0:00)

Alek Johnson: Welcome, everyone. Excited to be here with you today.

Tax planning is always one of those topics that everyone wants to know more about, because understanding it directly results in more money in your own pocket. But over time, I have found that the interest level in the topic can vary dramatically.

For example, I really eat this stuff up, but when I told my wife that I was doing a webinar on fun tax topics, she said, “Well, that will probably be a very short webinar then, won’t it?”

So, whether you love tax planning or you are just here to get the job done and get out, thank you for jumping on. For those of you who don’t know me, my name is Alek Johnson. I am one of the lead advisors here at Peterson Wealth Advisors. I’m a Certified Financial Planner™.

As always, I do have a couple of quick housekeeping items.

First, just so you all know, and I’m going to apologize in advance, this will be a little bit longer presentation today, probably around 45 minutes. I know, big red flag. Alek is your classic 20- to 30-minute presentation kind of guy. Believe me, I would love nothing more than to keep this one shorter, but in my experience when I’m dealing with tax planning, I’ve just come to find that people really want and need the details.

So we’re going to spend some time today to make sure you’re well-equipped to do your own end-of-year tax planning. And in the future, I promise a 20-minute webinar to compensate for this.

Next, if you have any questions during the presentation, please feel free to use the Q&A feature at the bottom of your screen. My colleague Jeff Sevy, who is another one of our great advisors here at the firm, is on with us right now and will be answering your questions the best that he can as we go throughout the presentation.

At the end of the webinar, I will take some time to answer just a few general questions, probably five minutes or so. As always, if you have a more individualized question, please feel free to reach out to your advisor here at the firm if you are one of our clients. If not, please feel free, you can always schedule a free consultation with us as well. We’d be happy to meet and answer any specific questions you may have.

And then last but not least, at the end of the webinar, there will be a survey sent out to give us some feedback as a team, and feedback for me as a presenter. Please utilize it. It’s very helpful to see what questions you have for future topics so that we can best help you out.

All right. And a quick disclaimer here before we do dive in, especially today, I think this one is important. I want to say that this is not tax advice. Clearly, I do not know all of your tax situations, so please use caution when determining if what we cover today makes sense for you and your particular situation.

If you are a client of ours, a lot of what we’ll be talking about today you’ve probably already heard at your end-of-year planning meeting with your advisor this year. But please feel free to reach out to them if you do have any questions that I don’t answer today.

All right, quick agenda for the day. I’ll just tell you, today is not about turning you all into tax experts by any means. It’s more about giving you a short checklist of moves to consider before December 31st, so less of your money goes to taxes and more goes to support your own goals, whether that be retirement income, family, charitable giving, or whatever it may be.

A big reason I want to talk about this today is that I have found, in my experience, many retirees are just unaware of the savings that could be created by utilizing these strategies, and I truly think that they are very underutilized in general. We want to make sure to get the word out to you, as sometimes this can create multiple thousands of dollars worth of tax savings, just depending on your situation.

Taxation 101 – (4:14)

Now, before we dive into year-end tax planning strategies that I want to discuss today, I think it’s important that we first discuss the taxation of different account types, as well as just how we’re taxed in the first place.

Knowing the different account types that you have is vitally important to manage your tax brackets, so I want to start there. And then at the end of this slide, just so you know, I’m going to have you take a picture of it, so if you want to have your phone handy, I’ll give you the cue on when to do it. I’m going to refer back to this slide quite a bit as we go throughout the day.

So, broadly speaking, you have three different account types, each of which is going to have its own unique tax advantages.

The first account type is your tax-deferred accounts. This will be things such as your 401(k)s, 403(b)s, traditional IRAs, thrift savings plans, whatever it may be. Generally, contributions to tax-deferred accounts will reduce your taxable income in the year that you make the contribution.

Once you make the contribution, those savings are going to grow tax-deferred, basically meaning that you’re not going to pay any taxes on any gains, any interest, or any dividends that you earn over the course of your working career.

Now, the catch here is that once money is distributed from these accounts, generally to your checking account so that you can spend it, it is 100% subject to income taxes.

Another thing to note is that you generally have to wait until age 59½ to pull any of these funds out of these accounts without incurring a 10% early withdrawal penalty.

Now, unfortunately, with these accounts, this first bucket here, you cannot just leave your money in there forever. The IRS requires you to take what’s called Required Minimum Distributions, or RMDs for short, from your tax-deferred accounts each year starting at either age 73 or 75, depending on the year that you were born.

The exception to that, just so you know, if you are still working beyond age 73 or 75, is if you have a 401(k) that you are actively contributing to.

Now, a Required Minimum Distribution is the minimum amount of money that must be withdrawn from a retirement account by the end of each year to comply with federal tax laws. We know how patient our federal government has been to get this tax revenue, so this is how they ensure that they get the money taken out of these accounts.

Second, we’re moving to tax-free accounts. So, unlike tax-deferred accounts, contributions to your Roth 401(k)s or Roth IRAs are made with after-tax dollars, so they won’t reduce your current taxable income.

That kind of begs the question: why would you want to do that if there’s no immediate tax benefit? Because as contributions go into these accounts, they grow completely tax-free.

And then the punchline here is that when you withdraw money from these accounts, you won’t owe any taxes on that income, which includes any appreciation or growth over the years that you were contributing and working. It’s all completely tax-free.

Now, some things to note on these accounts, like the tax-deferred accounts, is that you’re also subject to waiting until age 59½ to avoid the 10% early withdrawal penalty on any of the growth within these accounts.

But unlike that first bucket, Roth IRAs and Roth 401(k)s are not subject to Required Minimum Distributions. Your money can stay in those accounts until the day that you die, if you’d like.

All right, and lastly, our taxable accounts, otherwise known as brokerage accounts. If any of you have a bank account, a high-yield savings account, a CD, whatever it may be, the taxation is going to be the same as those accounts when it comes to these brokerage accounts. These accounts are funded with after-tax dollars, and the flexibility here is that they provide you the ability to take money out at any point, for any reason, at any time, without penalty. You can buy and sell, trade, and earn money, but you can take it out whenever you want. So you’re not subject to that age 59½ restriction when it comes to your brokerage accounts.

The bummer with these account types is that any income like interest, dividends, and capital gains that you earn year over year is taxable in the year that you earn it.

So, that being said, this is the time if you want to take out your phone and just take a quick picture of this slide, or refer back to it as we go throughout.

It’s important because each of these account types can play a very significant role when it comes to tax planning. We just want to make sure that you can clearly identify which account types you have as you enter or are in retirement.

Okay, moving on here. Now that we’ve covered the different accounts, I also want to make sure you have some understanding of the basics of how we are taxed in the first place, how your tax liability is calculated, as that will help lead into our tax strategy.

That being said, if any of you are CPAs or accountants online today, please do not hold it against me how simple I am going to try and make this.

So here’s a high-level view of the individual income tax formula. You’re going to start off by adding all of your income to get your gross income. This will be wages, salaries, rental income, dividends, interest. Everything will go into your gross income.

Once you’re here, you are allowed to subtract certain deductions called above-the-line deductions. Examples of these include things like IRA contributions, 401(k) contributions, HSA contributions, student loan interest, anything there goes above the line and brings you to your Adjusted Gross Income, or your AGI for short. Many of you are probably familiar with that number on your previous tax return.

Now, once you have your AGI, you get even more deductions called below-the-line deductions. The line, just so you know if you’re wondering, is the AGI. Above the line and below the line is AGI.

To determine what you’re going to deduct below the line, you will add together all of your itemized deductions and compare that with the standard deduction. You’re allowed to deduct whichever one is higher. I have this highlighted in red because I’m going to talk about it further in just a minute. We’ll dive into what those deductions are.

For now, just know you’re going to subtract the greater of the two, and that will get you to your taxable income. This is the number that you will actually pay taxes on. So when you see the brackets, this is the number that you’ll actually use.

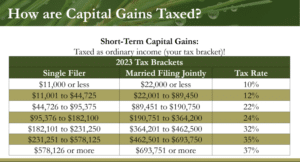

So that being said, you’re going to take that taxable income and multiply it by your ordinary income tax rate. Currently, there are seven brackets ranging from 10% to 37% federally.

Once you have multiplied it by those brackets, it will give you your tax liability. Now, that being said, we are still not done.

Next, you’re going to subtract any tax credits that you are entitled to, like the child tax credit, education credits, and previously there have been energy credits. Whatever those credits are, that’s going to go dollar for dollar against your tax liability, which finally brings you either to your taxes due or your tax refund, okay?

So what I want to focus on for just a minute, hopefully that was helpful to go through as a refresher, but I want to focus in on what I mentioned I have highlighted there in red, which is where we get those below-the-line deductions.

When it comes to these below-the-line deductions, as I mentioned, you get the greater of your itemized deductions or the standard deduction. The IRS has a list of things that we can count toward your itemized deductions, included on the screen here. So you have mortgage interest, state and local taxes, property taxes, medical expenses (kind of a funny one that it has to exceed 7.5% of your Adjusted Gross Income), and then the big one here is your charitable donations.

Included in this charitable donations deduction, if you are a member of The Church of Jesus Christ of Latter-day Saints, would be tithing, your fast offerings, humanitarian contributions, whatever else it may be, and then donations to any 501(c)(3) charity.

Now, if you add up all these deductions and they are not higher than the standard deduction, then you’ll just take the standard deduction. If the total is higher than the standard deduction, then you will itemize.

In 2017, the tax laws changed as part of the Tax Cuts and Jobs Act that President Trump signed into law. Part of what was changed, if you remember, was the standard deduction actually doubled. The One Big Beautiful Bill Act, which was just signed into law back in July, permanently extended these higher deductions.

So you can see here on the screen: in 2025, the standard deduction for a single filer is $15,750, and for a married couple, it’s $31,500. You get some additional deductions if you’re blind or over the age of 65. But again, for a married couple, if your itemized deductions don’t add up to more than $31,500, you will just take the standard deduction.

What this essentially means is that with the larger standard deductions, most of us will forego itemizing our deductions and we’ll end up taking the standard deduction.

Now, previous to the law change in 2018, about 30% of Americans itemized. We don’t have the most recent data, but as of 2022, it was around 10% of Americans itemizing their deductions. I would be shocked if this hasn’t gone up just because interest rates have gone up on the mortgage interest side, but it knocked about 20% off the amount of people who were itemizing at the time.

So how did that impact, or how does that impact those who give to charity?

Well, although gifts to qualified charities are still available as an itemized deduction, most charitable donors will not receive any tax benefit for their donations because few will donate enough to take them over that standard deduction. So for the 90% of taxpayers who don’t itemize, they’re out of luck.

Now, the good news is that there are still actions we can take to reduce your taxes, and that’s going to lead us to our first strategy.

Charitable Giving Strategies – (15:28)

So, real quick, I’m going to let you know the next three strategies we’ll talk about are all charitable giving strategies. The first one I’m going to focus on is what we call bunching, and then the use of Donor-Advised Funds.

So, I want to start off with bunching first. Bunching is a strategy used to maximize your deductions, and you’re probably very familiar with it already, because it’s something we do in other areas of our lives.

For example, we bunch our medical expenses. Let’s say you have a $5,000 deductible on your health insurance policy, and you know that you’re going to have a knee replacement surgery coming up in the next year. Well, you’re probably going to wait until that year to do all of your other medical things that you need to take care of, because you’ll know you’ve already hit that $5,000 deductible with the surgery.

Another example is credit card reward points. Many of us will earn reward points when we’re spending, and we redeem them for airline tickets. We don’t usually redeem these points when we’re making shorter, less expensive flights. So, if we’re going from Salt Lake City to Las Vegas, for example, we’ll usually just pay the normal airfare. However, we save up or bunch these points so that when we go to Hawaii, we can get the help when we’re incurring the larger cost for that airfare. We’ll usually spend the points at that time.

So, just as we can reduce our medical costs and our travel costs through bunching, we can likewise minimize our taxes through a similar strategy.

The goal of bunching is to exceed that standard deduction. That’s what we want to do, by piling on all of your itemized deductions to get those greater tax savings.

In years that bunching does not occur, you’re just going to revert to taking that standard deduction. So, in the year that you do itemize, it is very important to pay every tax-deductible bill and every tax-deductible expense, incur everything you can there. And then the big thing is that you want to donate two, potentially even three, years’ worth of donations to your favorite charity all in one tax year, which will result in a higher itemized deduction.

Practically, to give you an idea of how this might work, during the year you are planning to itemize, if you’re donating to the Church, you might pay your regular tithing, donations, and other humanitarian contributions monthly or bi-weekly as you get paid throughout the year. Then, come December of that same year, you will prepay all of your next year’s donations through one big lump sum.

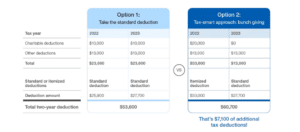

Let me give you a quick glimpse of how this would look. We’re going to take the Millers.

In option one, we can see the Millers year over year have $26,000 of total deductions. $14,000 of those deductions are from things like mortgage interest, potentially property taxes, state income taxes—things like that. And then they are giving $12,000 a year to charity.

So, in option one, if they just give the $12,000 a year over the two different calendar years—2024 and 2025—you’ll see they don’t have enough deductions to exceed the standard deduction those two years. And so they end up just taking the standard deduction in both years, which results in a two-year deduction of $60,700.

Option two is the tax-smart approach, where they’re going to bunch their giving in 2024. You can see they have $24,000 of donations now, plus the $14,000 of other deductions gets them to $38,000, which does exceed the standard deduction. So they’re able to itemize that year. In 2025, they’ll still have that same $14,000, but now they won’t have any charitable donations to deduct, and so they will revert to taking the higher standard deduction.

Now you can kind of see the difference. This results in an additional $8,800 of tax deductions, but it was not done by changing how much they donate. It’s simply by the timing of when they made those donations.

A common question we get is this: Is there a way to bunch deductions and still pay my charitable contributions on a more frequent basis? It’s that thought of, “I don’t love doing it annually—one big chunk up front all at once.”

And the answer to this question is yes. That is where a Donor-Advised Fund comes in.

Donor-Advised Funds, or DAFs for short, have been around for years, and there are a lot of them. They’ve become increasingly popular over the last decade, and you can open them up at really any major financial services company—Fidelity, Schwab, Vanguard, whatever it may be.

So what are they, and how do they work?

The best way to describe a DAF is that it is an account, just like your IRA account or just like your 401(k). It’s an account specifically designed to hold your charitable contributions until you decide when, and to what charity, you ultimately want to donate.

So how this works is that you, as the donor, will make a charitable donation to the Donor-Advised Fund. That can be made in cash. Better yet, it could be in the form of appreciated shares of stock, which we’ll talk about in just a minute. You, as the donor, are then going to get that tax deduction in the year that the contribution was made.

Your donation will then sit inside of that Donor-Advised Fund. You can invest it in there, and it can continue to grow until you decide to give it—whether it be to the Church or another charity—on your own schedule and on your own time.

So essentially, the timing of the donation from the DAF is up to you as the donor to decide.

Here are some practical applications that we have seen with Donor-Advised Funds. First and foremost, it just makes bunching easier to do and charitable giving a lot more flexible and easier to accomplish.

Second, it helps you get a deduction when it’s advantageous to you as the donor. One thing I want to point out here is that we often have clients who have higher income in the years before they retire, or they may be selling their business, or selling a second home, whatever it may be. Donating to a Donor-Advised Fund during those big income years can help you get a big deduction when you need it. And then you can essentially prepay for certain charitable endeavors.

I have plenty of clients who funded a Donor-Advised Fund before they served their senior mission, for example, and they paid for the housing portion of their mission with their Donor-Advised Fund.

Next, a Donor-Advised Fund can create a legacy for future generations. Many of our clients will use it for something like a missionary account for their grandchildren who will go and serve. Others pass it on even after they die for children and grandchildren to continue to donate from.

Donating Appreciated Assets to Charity – (23:09)

All right, our next strategy is donating appreciated assets to charity, appreciated meaning the investments have gone up in value.

This is a good one because, again, there are huge tax savings that can be realized by donating, and yet many taxpayers just fail to recognize it.

Now, one quick thing before we talk about it, if you think back to that image or pull out your phone and look at the picture, this is going to be pertinent to that third bucket, or the taxable accounts, such as brokerage accounts. This is not going to be utilizing 401(k)s or IRAs, Roth IRAs, anything like that.

This is only that third bucket.

Donations in kind are gifts of non-cash assets. You are giving the actual thing, not money. So think of a community food drive. Instead of writing a check, you’re donating canned goods, and then the charity immediately puts that to work.

Many charities, including The Church of Jesus Christ of Latter-day Saints, accept donations in kind. Charities accept almost all marketable securities such as stocks, mutual funds, and exchange-traded funds. Sometimes they’ll even accept more one-off things like gifts of real estate, life insurance policies, or potentially partnership interests. So it’s always good to check with the charity to see what they will and won’t accept before you donate. But this is a great strategy.

With investments, the “canned goods,” so to speak, are shares of investments that have gone up. If you sell those shares first, you may owe capital gains tax and the charity gets what’s left. If you donate the shares themselves, the charity can then sell them completely tax-free and keep the full value of the donation. And you typically get a deduction for the fair market value while you avoid paying that tax.

So let me give you another quick example here. We’re going to take the Andersons.

The Andersons have saved for retirement and now have a portfolio of individual stocks. One of the stocks that they own is Apple. So we’re going to assume they bought it for $10,000 ten years ago, and those same shares today are worth over $70,000.

If the Andersons were to sell $25,000 of Apple stock because they want to make a donation, and then donate that cash to the Church, for example, they would end up paying $5,000 in federal and state taxes, and the Church would end up getting $20,000.

As you can see in the right column, if the Andersons donate the $25,000 of stock, they won’t pay any tax whatsoever.

So here are the benefits that the Andersons get for donating their appreciated stock:

First, the Church that they donated to gets an additional $5,000, or a 20% greater donation.

Second, the Andersons don’t pay any tax on the gain of the stock.

Third, they also get to deduct $25,000 on their itemized deductions instead of $20,000, so they get that $5,000 bump.

And then any of the cash that they otherwise would have used to make a donation, they can buy right back into the market into a more diversified portfolio of stocks.

So before you write your next check to your favorite charity, you may just want to ask yourself: “Do I have any appreciated assets that I can donate to my charity that will be more beneficial than me writing this check?”

Now, this strategy by itself obviously saves you from paying capital gains tax and it’s great on its own. But when you couple this with bunching and with the use of Donor-Advised Funds, then we really start to pile on those tax savings.

The Use of the Qualified Charitable Distribution – (27:02)

All right, our next strategy is what’s called Qualified Charitable Distributions, or QCDs for short. I apologize for all the acronyms in the financial industry.

So again, if you refer back to the image of the three buckets that I showed you, we’re now just going to be looking at that first one, the tax-deferred bucket. Specifically, we’re going to be talking about IRAs. That’s the one we want to key in on here.

This is the most tax-effective strategy that I know to save you tax dollars. Unfortunately, there are some strict rules surrounding it, but when done correctly, it is amazing.

So what is it?

It is a provision of the tax code that allows a withdrawal from an IRA to be 100% tax-free, as long as that withdrawal is paid directly to a qualified charity, like the Church.

There are huge tax savings that can be realized, but these are not brought about by how much is paid to the charity, but by simply altering the way the contributions are made to the charity.

I always like to point this out:

First, you didn’t pay any income tax when you earned the money that you put into your IRA, your 401(k), your 403(b), whatever it may have been.

Second, you didn’t pay any taxes on the compound interest that your IRAs earned over 30 or 40 years of your working career.

And then last, any money paid directly to a charity through a QCD from your IRA will not be taxed. So this is one of those rare occurrences, similar to an HSA, where you get triple tax benefits.

So what other benefits are there?

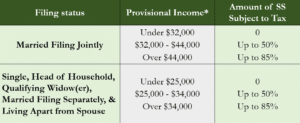

One, it can potentially reduce the amount of your Social Security benefit that’s going to be taxed.

Second, it will reduce the overall amount of income that is taxed.

Third, it will enable you to get a tax benefit by making a charitable contribution regardless of whether or not you itemize your deductions. This is a big one: you don’t have to itemize in order to get a benefit for doing QCDs.

And then lastly, these QCDs count toward satisfying your RMDs, or Required Minimum Distributions. So again, at age 73 or 75, when the government says, “Hey, we need you to take this money out,” you can just donate that instead. We have plenty of clients that, year over year, all they do is donate their Required Minimum Distribution so that there’s no tax due.

Now, as beneficial as QCDs are, they are unfortunately not available to all taxpayers, and the rules must be followed with exactness or the QCD will be considered a taxable event.

So here are the rules.

First and foremost, and probably the most unfortunate one, is that they are available only to people older than age 70½.

Now, why 70½? I do not know. (laughs) Talk to your local congressman. But it is specifically age 70½. What I mean by that is it can’t even be the year that you’re turning 70½, it has to be that you are 70½ years old.

Next, they are available only when distributions are from IRA accounts. So withdrawals from 401(k)s and 403(b)s are not QCD-eligible.

Now, that’s not that big of a deal, because you can always roll over your 401(k) or TSP, or whatever it may be, into an IRA, but it is something to be aware of. It can only come from the IRA.

Next, it must be a direct transfer from an IRA to a tax-qualified charity. Typically speaking, we don’t want the check to pass through your hands. If you were to deposit it by any means, that would become a taxable event.

There is a maximum of $108,000, this does adjust for inflation, of IRA money that is allowed to be transferred through a QCD.

So I know what you’re thinking: this is just a huge bummer. It’s capped at such a small amount, and we’re a big giving family here. I’m totally joking, hopefully that came across as a joke.

And then the last one here: the IRS has special reporting requirements for QCDs. You should check with your CPA to ensure that they report your donations correctly.

We have spent months and months in the past unwinding how a QCD was reported by someone’s CPA, so it’s important to know that it does have to be reported correctly. Otherwise, it could again be seen as a taxable event.

That being said, I believe that every person over the age of 70½ who has an IRA and who gives to charity regularly should absolutely investigate this strategy. You are your tax professional. You can run the numbers, do some comparisons, whatever it takes. I think that many of you, if not all of you, will find that the tax savings will be very significant.

Consider the Possible Benefits of a Roth Conversion – (32:14)

All right, so pivoting away from charitable donations brings us to our next tax strategy, which is considering the benefits of a Roth conversion.

Now, you may notice I did not say “do a Roth conversion,” but rather “consider the benefits of it,” and I am very intentional about that, because this may or may not be for everyone. A lot of people—whether it’s from the media, their friends, their family, their HR departments, whatever it may be hear that Roth is better, that Roth is king, but it isn’t always the case. So use caution with this strategy.

Now, if you are interested, I’ll just tell you too, I have done an entire presentation on Roth conversions specifically before. I’ll cover very similar content to what I did in that one, but if you ever want to really deep dive, just know that is available to you.

So, what is a Roth conversion?

Again, let’s refer back to the picture of the buckets on your phone here. As I mentioned earlier, virtually all retirement accounts are classified into one of two categories, meaning pre-tax or post-tax accounts, the first and the second bucket. For most retirees currently, it is much more common to have retirement accounts that are pre-tax money.

What a Roth conversion allows you to do is take a traditional IRA, or pre-tax retirement account, and convert it—either all of it or just a portion of it—to a post-tax Roth account. Essentially, you take it from bucket number one and put it into bucket number two. You are moving it from an account where you pay taxes into an account where it will grow completely tax-free.

So what’s the catch, then? Why not just convert everything and never pay taxes again?

Well, keep in mind that, just as the name suggests, any money in a pre-tax account has never been taxed before. That being said, any amount that you choose to convert becomes taxable to you in the year the conversion is performed. So as you take it out of that account, you are actually creating a tax liability.

For this reason, it is very uncommon to convert an entire account all at once, as it would likely push you into a higher tax bracket and make your tax bill unnecessarily large.

Quick example: if you have $1 million in a 401(k) or IRA, you can expect to pay 40% in taxes if you converted the whole thing over. So generally, the advice that we give clients is that we want to convert enough to get the future benefits of a Roth conversion, but not so much that it pushes you into a higher tax bracket.

Here are some quick key facts of Roth conversions.

First, there is no income limit. You can make a dollar a year, you can make a million a year, and you can still convert to a Roth.

Second, there are no age restrictions for conversions.

Third, there is no limit on how much you can convert. Again, I don’t usually say you want to convert everything, but there is no limit. You’re not capped. Sometimes it gets confused with contributions into IRAs, which are limited to usually $7,000 or $8,000 a year. You could convert the entire account if you really wanted to.

Fourth, the conversion must be completed within the tax year.

And then fifth, if you are 73 or 75 or older, you’re subject to those Required Minimum Distributions. You have to take the RMD first before converting any of the remaining funds. So the RMD itself cannot be converted to the Roth IRA.

So knowing it’s all taxable, it kind of begs the question: why would we do it? Why should we do a Roth conversion, or how do I know it’s beneficial for me? Well, despite the immediate tax liability, there are several potential benefits to doing a Roth conversion.

Number one is tax-free withdrawals. We already talked about this, but once it’s in there, it’s going to grow completely tax-free.

Second, there are no Required Minimum Distributions, so you’re not forced to take this money out as you continue to get older.

Third is what we call tax diversification. You’ve probably heard of investment diversification. Tax diversification provides a lot of flexibility in managing your tax brackets throughout retirement. You can strategically withdraw from each account to help minimize your overall tax burden.

Or if you needed a lump sum of money down the road, you wouldn’t have to pay a higher tax on that money if you took it from a Roth account.

Next is estate planning benefits. Roth IRAs can be really advantageous for estate planning. Your beneficiaries who inherit Roth IRAs will also have an additional 10 years of being eligible to keep it inside of those Roth IRAs for an extra decade of tax-free growth.

Now, in my experience, I will tell you there are not many children that are patient enough to inherit that lump sum of money and not take it out. But if they’re diligent, they absolutely can leave it in there for another 10 years.

A future tax rate hedge: if you expect tax rates to increase in the future, converting to a Roth IRA now can lock in the current tax rate. It’s particularly useful if you anticipate being in a higher tax bracket later on due to income increases, legislative changes, or whatever number of other factors.

And then the last one here: reduction of future RMDs. Again, by converting some of your traditional IRA now, you’re reducing what your account will be subject to in the future, which can help potentially lower your taxable income in coming years.

Now, a common misconception is that it is better to pay taxes now and let them grow tax-free than vice versa. The truth of the matter is that it does not matter when you pay the tax—now or later—if the tax rate is the same.

So often, deciding which one is more advantageous to your specific situation comes down to a variety of factors. Here are some of the things you do need to consider: How long are you planning on working? How long are you planning on living? What tax bracket are you currently in right now, and which one will you be in during retirement?

What types of income sources will you have—Social Security, pensions, rentals, anything else?

Whether the government changes tax rates, and in which direction they are going to change tax rates.

And the final one here is what state you live in, and when.

I’m going to give you some scenarios of both when you should and when you should not consider doing a Roth conversion. But again, let me reiterate: even though this may or may not make sense for someone else doesn’t mean it makes sense for you. So even with these examples, please be cautious about how you approach it.

First and foremost, if you have a year with unusually low income, potentially if you retire, you go serve a senior mission, during a job transition, early retirement, you get laid off, whatever it may be, converting to a Roth IRA can be advantageous. You’ll pay taxes at that lower rate on the converted amount.

Second is higher tax brackets in retirement. If you anticipate being in a higher tax bracket then than where you are now, paying taxes now at a lower rate can save you money in the long run.

Third, managing Required Minimum Distributions. Hand-in-hand with this one, if you can foresee that come age 73 or 75 you will be forced to take out massive amounts of money that will bump you into higher tax brackets, converting some of your assets to a Roth IRA can help lower your traditional IRA balance, thus reducing those required distributions.

Again, I kind of already mentioned this one, but if you expect your tax rate to be higher in the future due to changes in tax laws or just income, converting now means you’re locking it in.

And then that state example I mentioned earlier: if you live in a low-tax-rate state and plan to move in the future, it would be more advantageous to do it in the lower-tax state. For example, I come from the beautiful state of Wyoming, with no income tax. If you live there and you plan to move to Utah soon, you would be saving an additional five cents on the dollar by converting in Wyoming before you move to Utah. So state taxes also matter when it comes to this.

Likewise, here are some times you should likely not consider doing a Roth conversion.

If you are currently in a high tax bracket and, in the future, you’ll be in a lower tax bracket, it would not make sense to pay the taxes now. Generally speaking, most of the time when you are working, it does not make as much sense as when you’re retired.

Second, you have insufficient funds to pay the taxes. One of the key things with the Roth conversion is that whatever amount we decide to do—$30,000—we want that full $30,000 to go into the Roth to get the most benefit we can. But that means you need to have some funds on the outside to be able to pay that tax liability. If you don’t have those funds and you need to withhold from the $30,000, so only $25,000 ends up going in, then it may start to lose some of its appeal.

Third is if you have a near-term need for the funds. If you think you’re going to need to spend it for whatever reason, it may not be advantageous. It’s best when you can leave the money in there to grow tax-free for a long period of time.

Fourth is you’re close to your RMD age. Again, just because you have to take that Required Minimum Distribution first before you can convert, sometimes it makes less sense.

This one, though, use caution. I have several clients that are still above age 73 or 75 and we are doing Roth conversions.

Fifth is there’s a negative impact on financial aid. For some of you that may still have children in college and they’re basing aid on your income levels, this will increase your taxable income and it could have an impact there.

Next is tax credits and deductions, things like the child tax credit and education credits. Most have phase-outs, and so the higher your income is, you may phase yourself out of those credits or deductions. So keep that in mind.

Seven, you are very charitably inclined. Even if we can do Roth conversions at the lowest tax rate, 10% or 12%, QCDs are done at a 0% tax rate, as we already talked about. So just keep that in mind if you’re very charitably inclined, it may not make as much sense to do these conversions.

And then lastly here: Medicare and Social Security, and really the marketplace. Increasing your taxable income through a conversion can also make more of your Social Security taxable. It can also increase your Medicare premiums. If you’re on the marketplace and receiving a government subsidy to help cover your health insurance, it can affect that and you would owe taxes come tax filing time.

So really pay attention to all the extracurriculars going on outside of just your income, as it can affect even health insurance.

All right, so let’s just give you a quick example here.

I want to show you why, for example, a senior mission could be a really advantageous time to convert. We’re going to take the Parkers, age 63 and 62, and assume they are retired and going to serve a two-year mission in ’25 and ’26.

Before the Parkers leave on their mission, and then when they return home in ’27 (or ’28, I guess, in this example—I’m sorry, I should have updated those years), their income needs are going to be $12,000 a month before and after they serve.

Mr. Parker has a $7,000 monthly pension, and so he’s pulling $5,000 out of his IRA to sustain the Parkers’ lifestyle. At $12,000 a month, they will find themselves squarely in the 22% bracket. That means if they were to convert any money from a traditional IRA to a Roth IRA, it would cost them about 22% in federal tax.

When they go on their mission, they will only need $7,000 a month, essentially his pension. So at $7,000 a month, they will be squarely in the 12% federal tax bracket, which means they only pay the 12% tax if they do a conversion at this point.

So how much can they convert before they jump from the 12% to the 22% bracket? That’s about $44,000 to fill the 12% bracket, which would create a tax bill of $5,280.

If they were to convert that same $44,000 when they’re at home—before or after they leave—because they are still taking the extra $5,000 of income, now they have to pay it all at the 22%, which creates a $9,680 tax bill.

So that’s a $4,400 a year, $8,800 total, tax savings created from serving a mission if they served for those two years.

Now, just one quick reminder: if they had been in the same bracket before and during the mission, it really doesn’t matter. The Roth conversions start to lose their appeal at that point.

Tax Loss Harvesting – (46:37)

All right, final strategy I want to talk to you about today, and I apologize, I think we’re already at 45 minutes, so bear with me here. Hopefully it’s helpful. The last one is tax-loss harvesting.

Tax-loss harvesting is a strategy to help lower your tax bill by selling investments at a loss to offset capital gains, and then reinvesting those assets to maintain market exposure.

So again, back to your picture of those three buckets: we’re again just going to be talking about that third one. So this will not be for IRAs, Roth IRAs, or 401(k)s, but just those taxable accounts.

So let’s take a look at how this works.

First, you’re going to identify losses, find investments or stocks that have lost value in the account. At that point, you sell it. You sell the loss, and when you sell those losses, you can then use that to cancel out any gains from other profitable investments.

Now, if your losses exceed your gains, you can deduct an additional $3,000 a year against your ordinary income. What I mean by that: if you’re still working, your salary, your wages that you are continuing to earn.

After that, you can carry forward any losses. So if you hit that $3,000 and you still have some losses that you recognized, you can carry that forward indefinitely to offset future gains or income in coming years.

And then again, immediately, you’re going to buy into a similar investment to maintain your desired market exposure so that you don’t miss out on potential upturns in the market.

Let me give you a quick hypothetical example.

Let’s say you bought Coca-Cola stock two years ago for $50,000. Since you bought it, it’s gone down about $10,000 in value, and it’s now worth $40,000. If you sell it, you would be creating that $10,000 capital loss, which will now benefit you tax-wise. No one ever likes losses until it comes to tax time, then we’re all pretty big fans.

With that $40,000 of cash you now have, what do you do? Well, we want to stay invested, so generally you’re going to invest in a company or fund that you think will perform similarly to what Coca-Cola would do. So in this example, I’m just saying Pepsi.

Now, please note: this is 100% hypothetical. Coca-Cola has actually gone up the last two years. I’m also just comparing two companies based on the products they sell, not necessarily any other category. But hopefully you get the idea here.

Now, one big rule with this is called the wash sale rule. It simply states you cannot claim the tax loss if you buy the same or substantially identical security within 30 days before or after the sale. So you essentially have this 61-day window where you can’t buy or sell the exact same thing that you are selling. If you do that, you’ve triggered the wash sale and you no longer get to claim that tax loss.

Summary – (49:47)

All right, so wrap-up here—just a quick review.

Some questions that I would encourage you to ask before December 31st are:

- Would bunching my deductions help me itemize this year?

- Next, if I do bunch, should I consider using a donor-advised fund?

- Do I have any appreciated assets that I can donate in kind?

- Have I taken my Required Minimum Distribution, and am I eligible for a Qualified Charitable Distribution?

- Should I consider a Roth conversion this year?

- And are there any tax-loss harvesting opportunities in those taxable accounts?

I would strongly encourage you to meet with your tax advisor and see if any of these strategies could be beneficial in your situation.

Now, I also wanted to quickly go through a couple changes brought about by the One Big Beautiful Bill that was signed back in July. I know we’ve done a webinar on this, but I want to cover some of those high-level things again.

One, it expanded the Tax Cuts and Jobs Act. I think this is maybe the most undervalued or underrated piece of this that people kind of miss. 2026 would have been much worse had it not been extended for tax purposes. So that was a huge thing on the tax side of it.

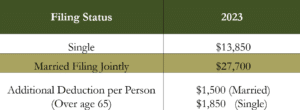

Next, individuals over the age of 65 can receive an additional $6,000 deduction, so married couples can get $12,000 collectively. If you remember, this was kind of the middle ground they came to. They were trying to make Social Security not taxable at all. This is where they settled: an extra $6,000 for those over the age of 65.

Now, just so you know, that does have a phase-out. For single filers, once your income hits $75,000, you begin to phase out. For single filers, you’re completely phased out of that at $175,000 of your MAGI, your Adjusted Gross Income for most people. For couples, it starts to phase out at $150,000 and completely phases out at $250,000.

One thing here, just as a reminder: you do receive this in addition to either the standard deduction or your itemized deductions.

Next, you have your SALT cap, your State and Local Taxes. That did increase from $10,000 to $40,000. So this could help many of you this year potentially itemize, just because property taxes, income taxes, and all of that has a much higher cap now.

Two other quick things here, just starting in 2026:

If you do not itemize your deductions, they are kind of throwing you a bone here to say you get an extra $1,000 of a charitable donation deduction per person, $2,000 for a couple. So it just helps a little bit if you do end up taking the standard deduction.

And then also starting in 2026, just know that your charitable donation deductions only kick in to the extent that they are over half a percent of your Adjusted Gross Income. So if you make $100,000 for your AGI, the first $500 that you donate is not deductible. It would be only everything in excess of that.

Well, that wraps up the tax side of things.

So before I open it up to questions, I did just want to throw this out there: if you don’t have this book yet and you would like a copy, please request one. We’ll send it out to you for free.

When it comes to good tax planning, you really are only as good as your income plan. You’ve got to have a retirement plan first, in my opinion. Think about Roth conversions, how are you going to know what your income level will be now compared to then if you don’t have a plan?

Scott Peterson, the founder of our firm, in this book, details what that plan is like. So if you don’t have it, please feel free to request one. I think it would be very helpful for you.

Okay, and before I turn it to Jeff for any questions, first of all, thank you for bearing with me. I know we went almost 55 minutes, so it’ll probably be an hour-long webinar here. So thank you for attending today.

And then also, if I can, a quick plug for the survey: right after the meeting ends, if you wouldn’t mind filling that out, it’s very helpful for us to know what you want to hear about in coming webinars.

Question and Answer Session – (54:16)

That being said, Jeff, I will turn it to you. Any questions we want to go through?

Question: Awesome. Yeah, we just got three here. So, the first one: “If you donate stocks to a QCD”, I’m assuming they mean a DAF. “Does that change your above-the-line income at all, even though you get to deduct it?”

Answer: No. Donations in kind into a Donor-Advised Fund are a below-the-line deduction. So your AGI would not really change, but your taxable income would change.

Question: Awesome. Also, kind of going along with the DAF: “Are you limited to cash and stocks when donating to a DAF?”

Answer: No, you are not limited. It’s always important to check with the donor-advised fund as to what they can accept. But just outside of stocks and cash, you have bonds, mutual funds, and exchange-traded funds. They will also sometimes accept business interests. Sometimes we’ve had clients who, when they’re selling a business, donate a piece of it into the donor-advised fund. So there’s a lot of opportunity there, and it would be worth exploring.

Question: Awesome. Then last one here: “How do Roth conversions play into estate planning?”

Answer: Yeah, it’s a really good question. Oftentimes when someone has this goal of, “I want to leave a legacy,” when you think of the pre-tax accounts, any money in there generally is going to be taxed before it reaches your beneficiaries in one way or another. If you leave it to a trust, there’s the potential that it could be taxed there. If you leave it to them outright, they have a 10-year window of time, and whenever they take that money out, they have to pay taxes at their own tax rate.

So by you doing Roth conversions and leaving the Roth IRA, they can receive that money completely tax-free and not have to worry about the tax implications. So oftentimes, if your goal is focused on your children or your grandchildren receiving the best outcome for them, that’s when Roth conversions can really make a big impact on the estate planning side.

Awesome. And that’s it for us.

Okay. Awesome. Well, thank you again, everyone, for attending. I’m going to stop sharing my screen, and we look forward to working with you. If you have any questions, please feel free to reach out, and we will see you all again likely in January for our next webinar.