Psychology of Money for the Retiree – Welcome to the Webinar (0:00)

Alex Call: Hello, everybody. Welcome to the webinar today. It looks like a few people are still taking some time to join, so we’ll give it another minute or so to let everyone trickle in.

I’m looking forward to discussing the psychology of money for retirees today. While people are joining, I’ll go ahead and introduce myself. My name is Alex Call, and I’m a Certified Financial Planner™ at Peterson Wealth Advisors.

Before we dive in, a couple of quick housekeeping items: If you have any questions during the webinar, please feel free to use the Q&A feature located at the bottom of Zoom. Zach, another financial advisor here at Peterson Wealth, will be answering your questions as they come in. If we have any questions left at the end, I’ll set aside some time for a Q&A session.

Additionally, you’re always welcome to send us an email if you have more individualized questions or need a more personal response. We’re happy to help.

Finally, at the end of the webinar, there will be a survey sent out. Please provide feedback and suggestions for future topics. Your input is invaluable in helping us improve and better serve your needs. With that, let’s jump right into it.

As with all our webinars, just a quick disclaimer: The information provided in this presentation is not intended to constitute legal, investment, or tax advice. It is provided for general informational purposes only.

Understanding the Psychology of Money for Retirees

Now, let’s dive into the psychology of money for retirees. The purpose of this presentation is to highlight that managing money relies much more on your temperament and behavior than on any intelligence or intellect you may have. Don’t just take my word for it; Warren Buffet said, “The most important quality for an investor is temperament, not intellect.” Napoleon expressed a similar idea, saying, “Genius is the man who can do the average thing when everyone else around him is losing his mind.”

Why is that? Because money is tied to emotions, and the better you can manage your emotions, the better you can handle your finances. Understanding how you think about money can significantly improve your financial decisions throughout retirement.

We make hundreds of decisions every day. Sometimes, we can think about them carefully, but other times, we make them on the fly using very little information. This is where heuristics, or mental shortcuts, come into play. These mental shortcuts are tools that help us make quick decisions or judgments. We use them not because we’re lazy or our mental resources are limited, but because there’s an overwhelming amount of information in the world. Life would be exhausting if we had to deliberate on every choice we make, so instead, we use these shortcuts to navigate the world around us.

For example, when you go out to eat at a place like Cheesecake Factory, where the menu is 10 to 15 pages long, instead of going through every possible option, you might order something you’ve enjoyed in the past or something a friend or server recommended. These shortcuts aren’t about making perfect decisions; they’re about making decisions quickly and efficiently.

However, sometimes these mental shortcuts can get us into trouble when they’re left unchecked. When this happens, they can turn into cognitive biases—errors that arise from our mental shortcuts and often go against logic or probability. Although we like to think of ourselves as rational beings who process all the information before making a decision, this is often not the case. Everyone is prone to cognitive biases to some degree.

For example, you rarely hear about shark attacks, so you assume swimming in the ocean is safe. But then, one day, you click on a shark attack video on Instagram, and suddenly the algorithm is sending you more and more shark attack videos. Now, you believe that shark attacks are much more common, and you may develop a fear of going into the ocean, even though millions of people swim in the ocean every year and there were only 69 attacks worldwide in 2023.

This illustrates how, if our mental shortcuts are left unchecked, they can lead us to perceive the world in ways that don’t reflect reality. These biases are largely based on our experiences. Everyone has their own unique experiences that shape how they view the world, and what you experience firsthand is always more compelling than what you learn secondhand. As a result, we all go through life anchored to a set of views about how money works that can vary significantly from person to person. What seems crazy to you might make perfect sense to me.

The person who grew up in poverty thinks about risk and reward in ways that the child of a wealthy banker never could.

As Charles Dickens said, “It was the best of times, it was the worst of times.”

John F. Kennedy was once asked about his memories of the Great Depression while he was running for president. His response was, “I have no firsthand knowledge of the Depression. My family had one of the great fortunes of the world, and it was worth more than ever. I really did not learn about the Depression until I read about it at Harvard.”

Clearly, his experience of the Great Depression was vastly different from the millions of Americans who struggled to provide for their families during that time. Because of this, their views and biases about money are also very different.

Common Financial Biases Retirees Face

These biases, developed over time, will follow you into retirement. So, we’re going to examine them from a retiree’s perspective, focusing on the most common biases I have encountered while working with retirees.

The first are loss aversion and negativity bias. Next, we’ll discuss optimism bias and recency bias.

As we go through these, you might notice these biases more in others than in yourself. That’s normal because it’s often harder to recognize these biases in ourselves.

While we can’t cover all the biases out there—there are hundreds of them—we will explore strategies for mitigating their impact on money management, both before and during retirement, by developing a framework for how to think through these biases.

Loss Aversion and Negativity Bias (9:03)

Let’s start with loss aversion and negativity bias. I group these together because they are closely related.

First, loss aversion.

Loss Aversion

Loss aversion is the tendency to prefer avoiding losses rather than acquiring equivalent gains. In other words, losing feels worse than winning feels good. As Larry Bird once said, “I hate to lose more than I like to win.”

Let’s try a thought experiment. Imagine I come up to you and say, “I’m going to toss this coin once. If it lands on heads, you get $1,000. If it lands on tails, you have to give me $1,000.” Would you take that bet? Or, how much would I have to offer you to make it worth the risk of losing $1,000?

Studies have shown that, on average, people would need to win twice as much to take the risk of losing. In other words, I would have to offer you $2,000 to get you to take the risk of losing $1,000. This suggests that people are willing to leave a lot of money on the table to avoid the possibility of losing because losses can hurt twice as much as wins feel good.

It’s the same thing with investing. It hurts more when the market goes down than it feels good when the market goes up. This is called loss aversion. Understanding loss aversion can help us see how the fear of losing money can strongly influence our decisions, often more than the chance of gaining money.

Negativity Bias

Now, onto loss aversion’s cousin, negativity bias.

Negativity bias means we give more weight to negative experiences or information than to positive ones, leading to an overemphasis on negative events.

Imagine you’re at dinner with your significant other, like I will be tonight, celebrating my 10th anniversary with my wife. Picture this: as we’re sitting there, I start complimenting her, saying, “Kim, you have the prettiest eyes. I love your outfit. Your nose is a little crooked, but you have a smile that lights up the room.”

What do you think she’s going to focus on? Probably the crooked nose. How many compliments will it take to get me out of the doghouse—five, ten? There’s probably not enough. And that’s normal because we tend to focus more on the negative things people say to us than on the positive things.

The Impact of Loss Aversion and Negativity Bias on Investing

This isn’t any different in investments. Retirees and investors tend to focus on negative market outcomes more than positive ones. When you combine loss aversion and negativity bias, it gets even worse. Not only are you more likely to focus on the losses in the market, but those losses feel much worse than the gains do, leading to an even stronger bias towards avoiding loss.

There’s one more reason why it’s so easy to focus on negativity instead of the positive: progress is slow, while destruction is fast. Growth is driven by compounding, which always takes time. Destruction is driven by single points of failure, which can happen in seconds. It takes years to build a reputation and seconds to destroy it.

Consider the progress of medicine. Looking at the last year won’t show much, and even a single decade might not reveal much more. But if you look at the last 50 years, you’ll see something extraordinary. For example, the age-adjusted death rate per capita from heart disease has declined by more than 70% since 1965. That’s enough to save roughly half a million American lives every year—the equivalent of the population of Atlanta being saved every single year.

But because that progress happens so slowly, it captures less attention than quick, sudden losses like terrorism, plane crashes, or natural disasters. This same mentality applies to investing, where we tend to focus more on the negative things happening around us.

So, let’s look at some of the negative events and turmoil that have occurred in the past hundred years in the U.S.

If we look back, we had World War I, then the Spanish flu, the Great Depression, World War II, the Cold War, the Korean War, the Vietnam War, the Cuban Missile Crisis, the assassination of John F. Kennedy, followed by the assassination of Martin Luther King, double-digit inflation in the late seventies, the dot-com bubble, 9/11, the Great Recession, and COVID-19—those are just the first 15 events that came to mind. There are many more that aren’t listed here.

Market Declines and Recovery Patterns Over Time

During this time, the stock market also experienced significant volatility. There have been over 40 declines of 15% in the market, which averages out to about once every three years. Declines of 25% have occurred over 20 times, or about once every five years. And 40% declines have happened eight times, approximately once every 15 years.

If this pattern continues over a 30-year retirement, you might experience 10 declines of 15%, six declines of 20%, and two declines of 40% or more while retired.

Listening to your negativity bias might lead you to avoid stocks, opting for safer investments like cash or bonds instead. But let’s see what would have happened if you had invested in cash or bonds instead of stocks over the last 100 years.

Since 1926, if you had invested $1 in cash or Treasury bills, that dollar would have grown to $23. If you had invested that $1 in bonds, it would have grown to $133. Now, let’s see what that $1 would have grown to if you had invested in stocks, despite all the turmoil and volatility that occurred.

That $1 would have grown to $14,568.

If you had let your biases drive you to invest conservatively due to fear and negativity, you would have ended up investing in cash or bonds, missing out on the high returns of the stock market.

Now, to clarify, I’m not suggesting that you invest all your money in stocks during retirement, but I do recommend having a significant portion in stocks. The reason is that listening to your negativity bias and avoiding stocks during retirement is going to negatively impact your life.

Impacts of Avoiding Stocks

How will it negatively impact your life? First, it will result in a lower standard of living. You’ll be limiting yourself to this lower standard if you keep your money in cash and bonds, missing out on the higher returns of stocks.

Second, you won’t be able to beat inflation. Investing in stocks is the best way to keep pace with inflation over the long term.

Finally, it will cause undue stress and anxiety by always focusing on potential negative outcomes instead of allowing you to live in the moment and enjoy retirement.

Now that you know some of the consequences of listening to negativity bias, how do you go about mitigating these biases?

First, know when you should be invested in stocks versus bonds. This depends on when you need the money. It’s about matching your investments with your income needs.

Here’s a cheat sheet or a mental shortcut to know how money should be invested in stocks or bonds. Money that you need in the next, say, zero to five years should be invested in fixed income. With interest rates being so high, this would include bonds, CDs, or high-yield savings accounts. The reason is that average market downturns last about 12 months, and you don’t want to stress about the money you need in the next 12 months being invested in stocks and their associated volatility.

Next, money you don’t need for the next six to ten years should be invested in a mix of stocks and fixed income. And money you don’t need for 10-plus years should be invested primarily in stocks. This is because downturns only last, on average, 12 months, so you can benefit from the upside of those higher returns.

Like I said, this is a good rule of thumb or mental shortcut. Your specific situation may warrant something different. For those of you just a couple of years from retirement, it may seem like you need to put everything in your 401(k) into fixed income, but that’s not quite the case. You’re not going to spend all of your 401(k) the day you retire. When you retire, you might live another 30 years, which means you’ll only be spending a small portion of your portfolio each year.

In addition to matching your investments with your income needs, here are two other things you can do to mitigate negativity bias:

First, schedule regular reviews. I don’t recommend checking the market every day or every minute to see what’s happening, but I do recommend scheduling regular reviews, whether it’s quarterly, biannually, or annually, to see how you’re progressing.

Second, practice gratitude. Focus on what you have achieved instead of the potential losses that may occur.

Now, a quick caution: I’ve met many people who blame their negativity bias or fear of investing in stocks on their religious beliefs, assuming the world is coming to an end tomorrow. I have listened closely to every session of General Conference for years, and all I have heard is optimism for the future. Temples must be built, missionaries need to be sent out, and technology needs to be enhanced for prophecies to be fulfilled. There may be a time immediately before the Savior’s Second Coming when the world is in chaos, but there’s no way to plan for chaos or know when it will happen.

So, let’s not dwell there. I really think President Hinckley expressed it best when it comes to how we should think about negativity. He said, “We have every reason to be optimistic in this world. Tragedy is around—yes. Problems are everywhere—yes. But you don’t build out of pessimism or cynicism. You look with optimism, work with faith, and things happen.”

Being optimistic in the markets means believing that we will continue to build and progress. I also love how President Hinckley did not say that things would go exactly according to plan, that there would be no problems, and that everything would be all sunshine, rainbows, and roses. That’s not the case. But when we assume that it will be, we can fall into the trap of optimism bias.

Optimism Bias (22:38)

Optimism bias is the tendency to overestimate the likelihood of positive outcomes and underestimate the likelihood of negative ones. This bias leads individuals to believe they are less likely to experience adverse events compared to others. While it can encourage a positive outlook, it may also result in underestimating risks and not preparing adequately for potential challenges.

I’m sure many of you have probably had some home renovation project or built a home or something similar. Think back to when you had that project. I’m guessing it was probably less expensive than you thought it would be, and it didn’t take as long as you expected, right?

No, of course not. These things almost always take longer and cost more than we initially think they will. That’s because we allow ourselves to be influenced by optimism bias.

Now, I want to share an example of this with a client I had, whom we’ll call Mr. and Mrs. Optimistic. These were hardworking, blue-collar people—one was a miner, the other a nurse. They saved their whole lives and were ready to enjoy retirement with a nest egg of over a million dollars—more money than they ever thought they would have. However, Mr. and Mrs. Optimistic are currently exhibiting optimism bias, which is influencing their financial decisions in a potentially harmful way.

They expect that between the investment returns on their million dollars and the potential inheritance coming their way, they can spend whatever they want, whenever they want. Because of this optimism bias, they are spending their retirement savings at an unsustainable pace, enjoying frequent vacations, luxury purchases, and an overall lavish lifestyle. They dismiss any concerns about their spending, relying on their optimistic beliefs that market returns and the expected inheritance will justify their actions.

But then reality hits. Market returns are not keeping pace with their spending, and the inheritance they expected turns out to be much smaller than they thought, leaving them without the financial cushion they believed they had.

As their savings dwindle faster than anticipated, they are left with one of three options:

Risk running out of money during their retirement.

Make a challenging transition to a more modest lifestyle.

If they can, they may have to go back to work.

Ultimately, when it comes to the consequences of optimism bias, it’s clear that whenever reality does not match expectations, it causes significant stress.

So, how do we combat optimism bias? I’ve found that the best way is to have conservative yet realistic assumptions when creating your income plan. This includes using conservative assumptions for returns. For a diversified portfolio of 60% stocks and 40% bonds, the average return has been about 7%. What does that mean? It means that a conservative approach would not assume a higher return than that—perhaps even a bit lower than that 7%.

Next, consider inflation. Inflation is real. You’re going to spend more dollars 10 years from now than you do today because things will cost more at that point. Make sure to include inflation in your plan.

When it comes to inheritance, remember that nothing is official until the money is in your bank account. Unless you’ve discussed the amounts with your parents and have seen exactly how it will be distributed, don’t rely on an inheritance to save you. Even then, I would be conservative in how much you expect to receive.

Another factor is life expectancy. People are living longer these days. If you and your spouse are both 60 years old, the chances that one of you will live to be over 90 are more than 50%, and healthcare is only getting better.

Next, consider your budget. People often think they can stick to their budget better than they actually can. I recommend creating a budget, listing everything down, and then adding a 10% buffer to it. This will give you a more realistic picture of what you’ll actually be spending your money on.

Lastly, remember that you’re going into a time when you might have more money than you’ve ever had. It might be hundreds of thousands of dollars, perhaps over a million or even millions. That’s a lot of money, but providing income for decades in retirement takes a lot of money too.

By using these conservative assumptions in your planning, you’ll be able to curb any optimism bias you might have.

Recency Bias (28:42)

Now, the next cognitive bias we’ll focus on is recency bias.

Now, let’s talk about recency bias. This bias is all about the attitude of “what have you done for me lately?” It favors recent events over historical ones. Recency bias causes people to give extra weight to recent experiences when making decisions, often at the expense of a more balanced view of the overall context.

A classic example of this is performance reviews at work. If you have an annual review, chances are your recent performance, especially in the last month, will be weighed more heavily than what you did at the beginning of the year.

For example, if we look back at the last five NBA champions (not including this year), three of those five head coaches were fired shortly after reaching the pinnacle of success. This demonstrates how recency bias can influence decisions, even in high-stakes environments.

So, what does this mean for you and your money?

Recency bias is like adding fuel to the fire. It can intensify our negative bias during market downturns, making us more negative than warranted. Conversely, during market upswings, it can boost our optimism bias, leading us to become overly confident.

When it comes to money, recency bias can be broken down into two categories. The first is reacting to what the market has done recently, and the second is reacting to current or recent events.

Let’s look at a chart that illustrates what happens when we react to what the market has done recently.

In this chart, you’ll see a green line representing a $10,000 investment made in 1992. The green line shows how that investment would have grown over time. The orange line shows what would happen if you sold your stocks and moved to cash at various points.

As you watch this, see if you notice any trends.

This video ends in October 2022. I’ll give you one guess as to what happened since then. The market shot back up, and as of the end of July, that $10,000 would now be worth $246,000.

This type of recency bias is when we become fearful and sell when the markets are down, or on the flip side, buy when the market is high, instead of staying the course. The lesson here is to think long-term and not be swayed by the ups and downs of the market. Remember, retirement is measured in decades, not years.

Now, let’s discuss a different kind of recency bias—allowing current events to dictate how you invest. A classic example of this is letting politics influence your investment decisions.

Let’s consider three different investors. The first is a Republican who only invests when a Republican is president. The second is a Democrat who only invests when a Democrat is in office. The third investor doesn’t mix politics with investing and stays the course no matter who’s in office.

Now, let’s see how their investments would have performed if we look at the track record going back to just after World War II.

This chart shows the growth of $10,000 invested in U.S. stocks since 1949. The red line represents the Republican. If you only invested when a Republican was in office, your $10,000 would have grown to $80,000. If you only invested when a Democrat was in office, that $10,000 would have grown to just over $400,000. And if you stayed the course and didn’t mix politics with investing, that $10,000 would have grown to just under three and a half million dollars.

The two lessons here are: first, never let your politics get in the way of your investing. Second, don’t let recent events impact your investment strategy.

If we let recency bias get the best of us, two primary things can happen:

You’ll let returns determine your mood. Your happiness will depend on whether the market went up or down that day.

You’ll constantly jump in and out of the market over time, likely losing money and not being able to enjoy retirement.

So not only will recency bias affect your money, but it will also affect your mood, preventing you from being present and in the moment. This is why it’s crucial to ensure that these biases don’t go unchecked.

So, how do we mitigate recency bias?

The first step is maintaining a historical perspective. This involves looking at long-term market trends and historical data, as we just did, rather than focusing on recent performance.

The second step is adopting a long-term time horizon. This means planning investments over a longer period, such as decades, rather than reacting to short-term market movements.

When we look at overcoming loss aversion, negativity, optimism, and recency biases, it’s about not being too optimistic or too pessimistic. It’s about controlling our temperament. Like Goldilocks, it’s about finding what’s just right.

Mitigating Other Biases (36:27)

Now, I want to discuss developing a framework for mitigating other biases.

The pioneering behavioral economist Daniel Kahneman said, “Maintaining one’s vigilance against biases is a chore, but the chance to avoid a costly mistake is sometimes worth the effort.”

Because there are so many different biases out there that we can’t cover today, let’s talk about a framework that will help you make decisions and protect you from any biases you might have.

I like to use the acronym ASK because you’ll need to ask yourself and others questions to mitigate your biases.

The A stands for Awareness, the S stands for Seek advice, and the K stands for Know your goals.

So, the first step to awareness is acknowledging that you are not immune to cognitive biases. Like everyone else, you have mental shortcuts that can lead to biases affecting your decision-making process.

Next, be aware by educating yourself—like you did today—about the biases that exist. Then, look for them when making decisions. Also, question why you think a certain way. Is it based on facts and historical data, or is it driven by emotion? Asking yourself why you believe something helps you become more aware of the biases you may have.

Finally, slow down. If you have a big decision to make, take the time to process the necessary information and don’t feel rushed. Don’t feel pressured to sell your investments or to buy a product from someone trying to sell you something.

The next step is seeking advice. Whether you seek professional advice or advice from a trusted contact, there are many benefits.

The first benefit is having an objective perspective. This allows you to take the emotion out of the situation and get an unbiased view of your financial situation and decisions.

Next is expertise. Financial advisors have specialized knowledge in areas like retirement planning, tax strategies, and investment management, and they’ve seen many people go through retirement.

Lastly, there’s accountability. Regular meetings with an advisor or a trusted contact can help keep you on track with your goals and prevent emotionally driven decisions.

But before you start seeking advice, you first need to know where you’re going. As the Cheshire Cat says, “If you don’t know where you want to go, then it doesn’t matter which path you take.”

This is why you need to know your goals. Having clearly defined goals for what you want in retirement will impact the type of advice you receive. If you don’t know what you want, even the best, most qualified advisor in the world can’t help you achieve your goals.

First, define your goals, and then prioritize them. Do you want to maximize your income in retirement? Is leaving a legacy to your kids more important? Do you want to retire now with slightly less income or retire later with a bit more income?

Remember, your goals are your goals, not anyone else’s. One of the most common questions I get when meeting someone for the first time is, “Do I have enough money?” I always tell them, “It depends on how much money you want to spend in retirement.” Some people get by on $3,000 a month and are super content and happy. Others struggle to get by with $25,000 a month.

So, the question of “Do you have enough?” depends on what you want.

I feel Elder Perry sums it up nicely: “You are not competing with anyone else. You are only competing with yourself to do the best with whatever you have received.”

Your goals will be dictated by how much money you currently have and when you plan to retire. You need to find out what works best for you as you determine what your goals are.

It’s important to note that this is a great opportunity. Retirement has only been around for a few generations. People in the past did not have the luxury or opportunity to retire; they worked until they died. We are now seeing people enjoy retirement for 20, 30-plus years—almost a third of their lives. This opportunity means that your generation has a chance to do something few others ever had: the opportunity to help others.

I like how President Benson puts it: “Our desires are that your golden years will be wonderful and rewarding. We hope your days are filled with things to do and ways in which you can render service to others who are not as fortunate as you.”

Retirement is an opportunity to render service to others who are not as fortunate as you. I hope that you’re able to enjoy your retirement.

So, in summary, we talked about the four primary biases that I see retirees struggle with: loss aversion, negativity bias, optimism bias, and recency bias. Then, we looked at a framework to mitigate other biases, using the acronym ASK: Acknowledge, Seek advice, and Know your goals. Finally, remember that retirement is an opportunity to serve. I hope you’re able to enjoy that opportunity as you prepare for retirement.

Thank you very much for attending.

Question & Answer (43:24)

Zach, were there any questions that came through?

Zach Swenson: Nothing came through, Alex. But we’ll give it a second to see if anything does.

Alex Call: Okay. If not, please feel free to reach out with any questions. Also, one thing I wanted to point out is that we’ve had a lot of people ask for a copy of the “Plan on Living” book that Scott Peterson wrote. Many of you have probably received a copy, and some of you have asked for another to give to a friend or colleague. If that’s the case, we’d be more than happy to either send them a book or send you an extra copy to give to them. Please just let us know, and you can respond via email, and we’d be happy to do that for you.

So, it looks like there are no questions coming in. Is that right, Zach?

Zach Swenson: Yep, that’s correct.

Alex Call: Okay, perfect. If you could, I would love it if you could take the time to fill out the survey. I always appreciate feedback to know how I can do better and also to learn what topics you’re interested in, so we can cover those in the future.

Financial Considerations after the Death of a Spouse: Welcome to the Webinar (0:00)

Carson Johnson: Hello everyone, welcome to today’s webinar. While everyone is joining the Zoom meeting here, just a couple of items and reminders for everyone.

First, there’ll be a survey at the end of the webinar that asks for feedback. We’re always looking for good feedback to make sure we’re providing excellent and applicable content for everyone, and to answer everybody’s questions.

Also, there will be a recording sent out tomorrow of this webinar. So, if you weren’t able to attend today, or if you know of somebody who might benefit from this webinar today webinar, you can get that recording and send it to them.

We try to accommodate everybody’s schedules as best we can, but sometimes that doesn’t always work. So, you can watch the recording there.

So, for those who don’t know me, I’ll just introduce myself. My name is Carson Johnson. I’m one of our Certified Financial Planners™ here at Peterson Wealth Advisors, and I’m excited about today’s webinar.

The topic that we’re going to be talking about today is actually very important, and near and dear to my heart, because I’ve seen the value of financial planning work in the lives of widows and widowers, and it can be of great value.

It’s a natural part of retirement. It may not be such a positive topic, but it is such a valuable thing that can make the difference of thousands of dollars and really provide financial peace of mind.

So, for those who are going through this process or have already gone through this process, I hope that today’s conversation can at least provide you with a game plan and a roadmap to have that peace of mind financially and to start to develop your own personal plan.

Financial Considerations after the Death of a Spouse (1:54)

Now, for today, today’s focus is not to turn you all into financial experts by any means. Today, what I want to focus on is the most important financial planning tasks and considerations that widows and widowers should consider.

And in part of that, I want to help answer these five questions.

How do I find financial security as a widowed person?

What are the different stages of widowhood and why are those important?

How do I know how much I need for income?

How do I make the most of special Social Security rules that only apply to widows and widowers?

How do I create my long-term financial plan?

So, once you have experienced the loss of a spouse, many widows and widowers may feel like they wake up and some days think that this is all a bad dream, only to realize that it is not.

This leaves widows and widowers feeling lost, worried, and confused and may relate to a lot of the words that you can see on the slide.

It’s also very normal to have widows feel some form of anger. Now, when I say anger, this isn’t anger towards a particular person. This may be anger that you’ve lost your best friend or someone you’ve cared so deeply about.

Now you have that burden and responsibility to manage your whole household and the financial decisions that come along with it. One thing that might be helpful for you if you’re going through, the loss of a spouse, is to connect with others who understand what you’re going through.

No matter how much you talk with family, friends, or even professionals, they won’t be able to provide you with that same understanding as others who have gone through a similar experience.

Also, I would highly recommend that you consider a session with a grief counselor or a therapist. Although that may seem like a sign of weakness for some, it is actually a sign of strength because they can help you find the strength to work through these emotions and this big change that’s happening in your life and be a very therapeutic experience for you.

Widow Statistics

Now, just to emphasize why planning for widowhood is so important, I want to share some shocking statistics that I learned as I was researching a little bit more about this topic.

First, there are 12 million widows in the US today, with approximately 1 million adding to that number each and every year.

Second, is the average age of a wife that becomes a widow. I’ve listed three different options here, and I want you to think about them, just think to yourself or even post in the chat to keep yourself honest about what you think the answer to that question is. When I first saw this, I thought I knew the answer, but was surprisingly wrong. And the answer is age 59, a lot younger than I originally expected.

Oh, and also, by the way, I forgot to mention this, if you have any questions throughout this webinar, I’ve got Josh Glenn, who’s one of our financial planners here, able to answer your questions. And then we’ll leave some time at the end to answer any questions as well.

The next statistic is half of women over age 65 live 15 more years after their husband dies. 70% of baby boomer wives will outlive their husbands. 80% of women will be single at death. Widowed female seniors outnumber widowed males by more than four to one. And lastly, 70% of widows and widowers said, becoming the single financial decision-maker was the top financial challenge of widowhood.

The Four Stages of Widowhood (5:33)

So, now that we understand the importance of planning for widowhood, let’s dive into the different stages of widowhood. I gathered this information from the Financial Transitionist Institute. They have a really great way of describing these different stages that I think are very applicable.

Stage One: Preparation (5:50)

So, first is the anticipation or preparation stage. Now, for most widows, they may not have the luxury of preparing for the passing of a spouse.

I remember a client who came in a couple of years ago and told us about her 58-year-old husband who was as healthy as can be. Someone who was mindful of what they ate and was always going to the gym, was considered a gym rat in her words. And the thought of her husband passing away never crossed her mind until she had that experience.

Now, preparing for the passing of a spouse may not be a very fun or enjoyable topic to discuss with your loved one. But for those couples that are in attendance at today’s webinar, I would highly recommend doing so. Please make it a priority, because that will make both of you better prepared for the challenges that lie ahead during widowhood.

During the preparation stage, if you have the luxury of preparing for this, there are various things that you may want to consider. Things like healthcare issues, opinions, and options.

This may be related to end-of-life care, whether it be related to life support and what conditions you want to make sure are met, or who you want to list or give authority to make those end-of-life care decisions.

Explore your beliefs about death. Discuss financial and insurance issues as they pertain to your household. Discuss how personal effects will either be passed on to heirs or to you as a surviving spouse. And then discuss funeral planning and logistics to make sure you have enough cash flow to cover those expenses that happen.

Stage Two: Grief (7:36)

The second stage is the ending or the grieving stage. And during this stage, it’s important that widows begin to prioritize what needs to be done and what can wait. There are a lot of resources out there for widows, but most just don’t know where to start.

Many surviving spouses report that they experience what’s called brain fog, or widow’s brain. For those that are going through that, you might be able to relate to this because during a very traumatic event like this, losing your loved one, you may have difficulty performing tasks that might normally be easy for you. Whether that be financial tasks or just day-to-day living tasks, widow’s brain or brain fog is a very real thing.

We’ll talk about ways that you can help yourself prioritize those to-dos so that as you’re going through this experience, it can be easier for you.

Now, during the grieving stage, it’s important that you focus on yourself. This is a highly vulnerable time for you. I suggest that you make no major and permanent decisions for at least six months to a year.

And we’ll talk about a few of the different financial planning strategies related to this. And sometimes it’s actually better to just wait to make those decisions.

Focus on your immediate needs, whether that be emotional needs or financial needs to cover your short-term bills and so forth. Speak with people about what is going on, reflect, and talk about the thoughts and emotions that you’re experiencing.

And this last one, this is interesting and may seem counterintuitive, but identify and name your greatest concerns. By naming and writing down those concerns, it can be actually a very rewarding experience to say these are my concerns and I can overcome them.

I have found that doing so can build a lot of strength for widows.

Next, is getting organized. You don’t have to get everything done and start creating your plan right away during this stage. In fact, I would not recommend it. But create a filing system where you can start gathering important and vital information that you’ll use soon. Things like bank account statements, debt statements, Social Security statements, pensions, and so forth.

Next, make sure you get multiple copies of the death certificate. There will be various institutions that will require a certified copy of the death certificate. Whether that be the bank or investment accounts or an employer or whatever, may require, multiple copies. So, having enough on hand will be really helpful.

Next, is finding the will and other legal documents that might pertain to you. These are very important documents in administering the estate of your deceased spouse.

If you find multiple legal documents or multiple wills or copies, then you may want to talk to an attorney to see how to go about that.

Next is to take notes. This is a helpful tip that I’ve learned while working with widows. That same widow I was talking about with her husband who passed away. I found that she wasn’t the main decision-maker in their household when it came to their finances.

And a lot of this information regarding budgets and investments, taxes, was very overwhelming for her. So she brought a notepad that she would write down everything that was important to her and that meant something to her in her own words. And I think that can be really helpful during that process.

And then lastly, notify relevant parties such as banks, employers, and so forth.

Now, as a widowed person, the truth is there are going to be a lot of items that you are going to have to take care of over the coming months and possibly years. Fortunately, you do not have to do all of them immediately. It is kind of backward thinking because a lot of times widows think they have this mountain of paperwork and a mountain of items that they need to do.

Although there is a lot to do, not all of it is urgent. And if that is one lesson and takeaway that you take from this is that there is a lot to do, but not all of it is urgent.

A good way that I have found to organize your to-dos is by creating your own personal roadmap, which I found is called now, next, and later. And with this now, next, and later, essentially what you do is take a piece of paper or something to write on and make these three columns.

Focus on all the items that are most urgent and that you need to take care of right away, and that’s your now column. Then you take the next most important items that you can take care of shortly after the memorial service and things like that, that you want to focus on next.

And then the later section or a later column, that’s when you start to begin addressing kind of more complex and building your financial plan.

So, just some examples of this for the now column might be planning the memorial service, spending time with family, finding important documents, paying your short-term bills, and so forth.

Next, you want to contact your life insurance agent and determine your cash needs for the next year or two while you’re figuring out this new phase of life.

And then lastly, as I mentioned, start building your financial plan, organizing your investment accounts, and so forth.

One of the points I do want to make is that it is important to make sure you meet with an attorney to create your new estate plan.

One of the big mistakes that we see widows make is they will get so caught up with their to-dos that they fail to prepare for their own estate, which can be a big burden and really a mess for the heirs that follow. So make sure you spend time focusing on yourself and building your estate plan.

Stage Three: Growth (13:41)

Now, the next stage is the passage or growth stage. This is where you start adjusting to your new life situation and where widows and widowers begin to feel the brain fog or widow’s brain lifting.

At this point of widowhood, you begin to figure out your financial plan and start addressing important questions, things like, what does my income situation look like? What should I do with life insurance proceeds? Should I sell my house? What should I do with my housing? When should I claim social security? And much more.

Key Financial Planning Strategies for Widows

So for this stage, I want to focus on some of the most important financial planning strategies and considerations that happen when you start to begin building your financial plan.

The first is determining your income situation. So I’ve kind of outlined this into a four-step process for financial readiness.

And so what that looks like is you need to determine your income needs by creating a budget and maximizing your mailbox money, which we refer to mailbox money as money that’s coming into your bank account that has nothing to do with your investments or life insurance. And if that mailbox money doesn’t cover all of your income needs, then you’ll need to cover the shortfall with savings and investments and have a long-term investment plan to cover those needs.

And then lastly, coordinating all of those resources together into one cohesive plan.

So the first step of that financial readiness is to estimate your current budget. Now, there are a lot of resources out there about budgets, and you’ll want to find the one that works best for you and your situation. But there are two common approaches of ways you can build a budget.

Bottom-Up vs. Top-Down Budgeting Approaches

First is the bottom-up approach, and how this works is you essentially start from the bottom with your different budget categories. So you figure out what amount of money you need for food, for housing, for taxes, for insurance, and so forth. And you allocate the right amount of dollars into each of those categories, and you add that all up to equal your gross income that you need.

On the flip side, you could do the top-down approach where you take your income sources, your total income, and subtract your overall estimated expenses to equal the net income that you need.

Now, the top-down approach is a lot faster and simpler approach which can be helpful when making a decision fairly quickly. But the bottom-up approach might be more advantageous because it’s a little more detailed and can be probably more accurate for your planning purposes.

So whatever method you decide to choose, it’s important that you determine what your income needs are so that you can proceed to the next step.

Now, once you enter widowhood there are various changes that will happen including your expenses.

Healthcare Coverage Adjustments

I’ve listed four of the big, four main changes that will happen. There’s an exhaustive list that I’m not gonna go over all today, but these are the four big ones.

First is healthcare, especially if you’re a widow who’s been a homemaker and is under the age of 65, or is not eligible for Medicare quite yet, then health insurance planning is going to be critical.

It’s important to get the right coverage that you need but to do so in the most affordable way. We’ll talk a little bit more about health insurance options a little bit later, but that’s a big change that might happen.

Housing, oftentimes when a spouse has passed away, the question comes up is, should I pay off my mortgage, especially if there are life insurance proceeds involved? Or should I reduce, downsize my house, etc?

Paying off a mortgage is a perfectly reasonable financial goal and can provide a lot of peace of mind. But as a side note, for those who do decide to pay off their mortgage, be aware that you’re still on the hook for taxes and insurance and should build that into your budget.

Before you make that decision, make sure you understand that you’re taking care of your full income situation first before you just go ahead and pay it off because you may need to figure out the right balance between having that mortgage and having the right amount of income.

The third is hobbies. This may seem like an odd one to put out there, but once you become a widow, it’s important to keep yourself busy. Make sure you set aside some funds to stay connected with your friends and family, and your social network because it can be a very lonely and discouraging experience at the beginning of widowhood. By keeping busy and allocating those funds, it can allow you to have a purpose and stay busy.

Then lastly is taxes. Unfortunately, taxes will be more expensive for a widowed person. There’s something that’s called a widow’s penalty, which we’ll talk about a little bit later, but it’s important to realize that taxes will likely go up.

Even though you may be living on possibly less income as a widowed person or a single person, taxes could still actually go up as you become a widow. Again, we’ll talk a little bit more about that.

So the second step is to maximize your mailbox money. So like I mentioned, this is income that’s coming in that has nothing to do with your investments or life insurance. So things like pensions, Social Security, rental income, part-time work, and so forth.

Now, I’m not gonna dive too much into rental income and part-time work because that’s dependent on the situation, but I do want to spend some time on pensions and Social Security for just a moment. With pensions, oftentimes pensions have survivor options available to a surviving spouse. Meaning that they may continue to receive either 50%, 75%, or 100% of their deceased spouse pension benefit.

Every pension is different, and it depends on the surviving survivor option that your deceased spouse chose when they took the pension. If they haven’t taken the pension yet, then you can just contact the pension provider to see what your options are.

Social Security Survivor Benefits Explained

Next, let’s talk about Social Security benefits. As a surviving spouse, there are a few different types of Social Security benefits that may be relevant to you.

Some of these benefits include paying benefits to minor children, or to you as a surviving spouse who’s caring for minor children, or even Social Security disability benefits.

There’s a lot of unique nuances to each of those special benefits that I’m not going to dive into today. We may want to do that as a separate webinar, a deeper dive into that.

But if you are eligible for any of those more unique benefits, there are significant planning opportunities related to Social Security and claiming options, and that can result in the difference of thousands of dollars that you receive. So be sure you discuss this with a professional or reach out to us, we’ll be happy to review your situation with you.

But for today’s purposes when we talk about Social Security, I’m going to focus on the survivor benefit or the traditional benefit you get as a surviving spouse.

How survivor benefits work is they’re dependent on three main things. First, your deceased spouse’s PIA, which stands for your Primary Insurance Amount, is just a fancy word for your full benefit at their full retirement age.

The second depending factor is the age at which your deceased spouse originally claimed their benefit.

And then lastly, the age at which you as a surviving spouse claims the survivor benefit. We’ll see if those few things will determine the amount that you receive.

But as a general overview, here’s how survivor benefits work. If the spouse dies while you’re receiving benefits, the widower may maybe be able to choose the higher of the two benefits.

Example of How Survivor Benefits Work

So for example, let’s say we have Joe and Julie. They’re married, both over their full retirement age. Joe’s benefit is $2,000 a month, and Julie’s benefit is $1,200 a month. When Joe dies, Julie notifies the Social Security Administration, and her $1,200 benefit is replaced by her $2,000 survivor benefit, which is the benefit that her husband was receiving, Joe.

So knowing that you have the widower, the surviving spouse gets to choose the higher of the two. It’s important that those couples that are in attendance today and are trying to decide what they should do for Social Security, one of the factors that they may want to consider is making sure that the higher benefit of your two benefits is as big as possible. Because if anything happens to you, then your surviving spouse would receive the larger of the two. So, factor that into your decisions there.

Now, there are a few rules to be aware of when it comes to survivor benefits. First, a couple must have been married for at least nine months before the date of death. There are some exceptions to that if there is an accident, but must be at least married for nine months.

Second, a survivor must be at least 60 years old for a reduced benefit which is a little bit different than normal Social Security benefits which you can’t begin taking until age 62. So as a surviving spouse, you’re able to claim a couple of years earlier than regular Social Security benefits, but it’s at a reduced amount.

If you decide to wait until your full retirement age, then you can receive the full survivor benefit and not have to worry about a reduction if you wait until your full retirement age.

Now, for any of you who have been married and got a divorce and your ex-spouse passes away, you may be eligible for what’s called a divorce spouse survivor benefit if your marriage lasted at least 10 years. If that applies to your situation, you’ll also definitely wanna look into that and see how that applies.

Now, one of the biggest questions as it pertains to Social Security is what if you apply for your survivor benefits early, prior to your full retirement age. Ultimately, what happens is your benefit is reduced. You receive a portion of your spouse’s Social Security benefit.

So for example, let’s say my full retirement age is age 66 and I decide to claim my benefit at age 60. I would receive 71.5% of my deceased spouse’s Social Security benefit. If I wait till age 61, I would receive 76.3% and so forth. And then if I wait till my full retirement age, like I mentioned, then you would receive the full survivor benefit.

So how the reduction works is it’s essentially about a 4.75% reduction on average per year for every year you claim early prior to your full retirement age.

Now, another important thing as it relates to survivor benefits specifically is there’s no benefit in waiting till after your full retirement age to claim.

So once you’ve hit your full retirement age, if you go past that then you’re just leaving money on the table and you do need to make sure you are applying for that survivor benefit. So make sure you don’t wait any longer than your full retirement age.

Now, let me quickly describe how the regular Social Security benefits work and this will help explain why these benefits are unique for surviving spouses.

So with the regular Social Security system, the same reduction principle applies. Meaning if you apply for your regular Social Security benefit based on your own work history prior to your full retirement age, then your benefit would be reduced. So again, if my full retirement age is 66, I claim at the earliest age possible of 62, then I would receive 75% of my benefit.

But the thing that’s unique about your personal retirement Social Security benefit is that it can also increase past your full retirement age. So your personal benefit can increase on average by about 8% per year for every year past your full retirement age. So if I wait till the latest that I possibly can, which is age 70, my benefit could be 132% of my original benefit.

Now, I’ve listed how it applies to all the different full retirement ages. So if your birth year is 1955, your full retirement age is 66 and two months, and the reductions and increases for that full retirement age, including age 67 there.

Now you’re probably wondering why am I bringing this up. The reason is that surviving spouses have unique claiming options. Essentially what they can do is they can claim either their own personal retirement benefit or the survivor benefit, but not both at the same time.

But you can coordinate them together by claiming one now and the other later. Generally, as a good rule of thumb, it’s better to wait to claim the higher benefit until you reach your full retirement age. That way you can maximize that larger benefit for the rest of your life or the rest of your retirement, rather than taking a permanent reduction for the rest of your life.

So let me give you an example of how this could apply.

So let’s say we have Jane, she’s currently 62 years old, and her husband just recently passed away. Her full retirement age is 66, and she has worked as a librarian for the local library where she earned a Social Security benefit of about $500 per month at her full retirement age.

Her husband’s benefit was $2,000 a month which is now Jane’s survivor benefit if she waits till her full retirement age.

One strategy that she may want to consider is claiming her own personal benefit first of $375. Let’s say she’s claimed it right away at age 62, she would receive a reduced benefit for her personal benefit that she claimed of $375. And then she can switch to a survivor benefit later at her full retirement age so that she can avoid reducing that larger benefit.

Now, that’s just one example, there are actually a lot of different claiming options that are available to widowers, you may want to do the opposite.

Let’s say your benefit is very close to the survivor benefit. One option that you may want to consider is taking the survivor benefit first and then allowing your personal retirement benefit to grow and increase to age 70, maximizing that benefit, and then switching to that larger benefit later down the road.

So this is why it’s so unique for surviving spouses: you have the flexibility of choosing one or the other without having an impact on each other. And trying to figure out what Social Security claiming strategy works for you is an important question.

Now, the decision of when to apply for benefits is one of the most complicated really difficult questions to answer because there are a lot of factors that flow into this.

So things like your health situation, life expectancy, your need for income, whether you plan on working or not, and so forth, are all different and very important reasons.

Now, a couple of important points. If you are working and you’re under your full retirement age, as a good rule of thumb, it’s best to not apply for Social Security until you are either done working or you’ve reached your full retirement age.

If you are taking Social Security prior to your full retirement age and you are still working, Social Security has a rule called the earnings limit, which means they may withhold some of your Social Security benefit because you are working and they essentially don’t want you double dipping while you are working and prior to your full retirement age.

But once you reach your full retirement age, then at that point it doesn’t matter if you work, that earnings limit does not apply.

Also, the other important note is if you decide to wait to claim your Social Security past age 65, you may want to still apply for Medicare.

There are some exceptions to that where if you’re covered by a group health insurance plan through work or another group health insurance plan, then you may not need to apply. But as a good rule of thumb, make sure you apply at 65 because if you don’t and you’re not covered by a group health insurance plan, there could be significant penalties if you apply later down the road.

All right, now let’s move on to step three, which is covering any shortfall with savings and investments.

So once you’ve determined your budget and your income needs you, then you would subtract your mailbox money or income that’s coming in from Social Security pensions and so forth to equal the amount of income that needs to be covered by your investments or savings accounts.

So for example, let’s say your needed income is $82,350. Your mailbox money or your pension and Social Security income is $65,000. Then the net income that you need to cover is $17,350 or $1,445 per month. That amount would need to be covered by some other sources, for example from your investments or savings.

Now, there are a lot of different ways to make sure that you’re withdrawing a safe amount from your investments each and every year so that money can last you a 20 and 30-year period of time.

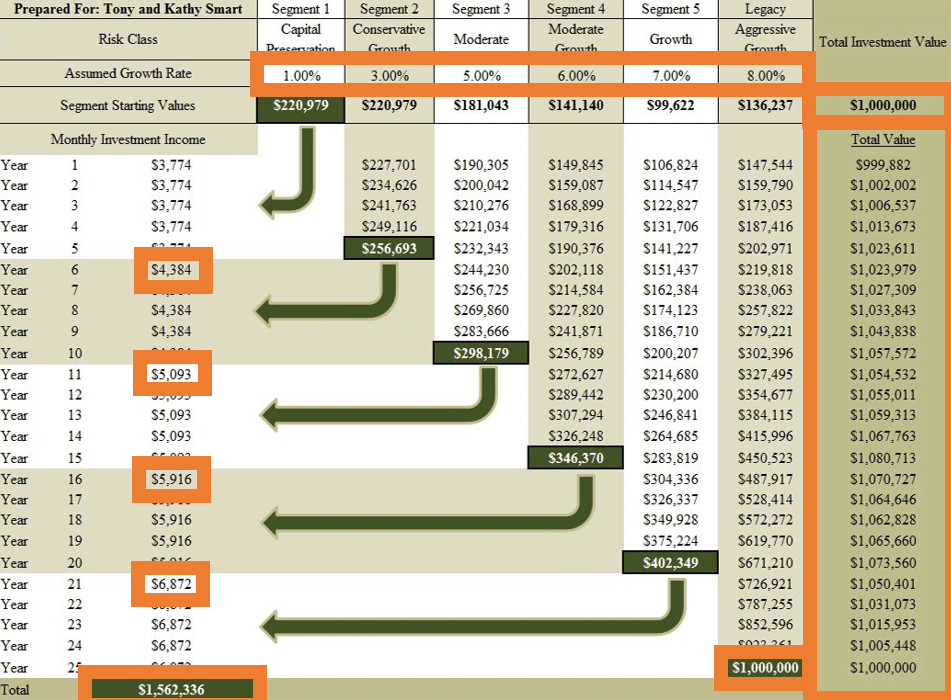

Retirement Income Planning

There are lots of different withdrawal strategies, but one of the values that we provide for our widowed clients is our Perennial Income Model™, where we can help you map out an inflation-adjusted stream of income to last a 20, 25, 30-year period of time where we will coordinate a cohesive plan with your mailbox money along with your investments.

This is an example of what that income model looks like, and I won’t dive into it deeper today but we have lots of resources on our website and videos that talk about how this income model works and can really provide peace of mind to make sure that those investments last throughout your life.

But as a general rule of thumb, if you’re trying to figure this out on your own, I want to introduce you to a guideline called the 4% rule.

This isn’t a hard and fast rule, but this is just a quick calculation to determine what’s the sustainable withdrawal that you could take from your investment portfolio.

So how this would work, let’s say we use the same example as before. We figured out our income shortfall of $17,350 per year. You multiply that by the number of years you need to cover.

So let’s say you’re age 60 and you want to plan for a 30-year period of time to get you to age 90, you would use 30, multiply that by 30, and that equals that $520,500, which is the required investment savings you need to provide that to cover that income shortfall.

Then what you do is you take that income the required investment savings, and you multiply that by the 4% rule or the 4%.

And that equals the sustainable withdrawal amount that you can pull from your investments per year, which should be reasonable as long as it’s reasonably invested, and lasts you a 30-year time horizon.

Now, there’s a lot of assumptions baked into that. You have to, this is assuming that your investment portfolio is invested in about 50% stocks and 50% bonds and things like that. So you have to make sure you are invested in order to meet the sustainable withdrawal. But as long as you’re invested properly, this is again a general rule of thumb that can help you determine how long your investment portfolio will last.

Now the next question is, what should I do with life insurance and retirement funds? I’ve listed a few of the different options and common things that happen. This may be supplementing your Social Security income, setting aside for future retirement, paying off debts, funding college for kids or grandkids, missions, and so forth.

But it’s important that although your life has changed, it’s helpful to evaluate whether you have enough to financially be stable for the remainder of your life first. And I like to compare this to the pre-flight safety instructions that everybody has probably heard if you’ve been on a plane. They usually say something along the lines of, in case of a change in cabin pressure, be sure to place your oxygen mask over your own face first before assisting anyone else, even your own children.

I thought of this kind of ironically because oftentimes we run into widows who are so focused on helping their kids or grandkids. But then they haven’t focused on themselves first and figured out their personal financial plan.

So make sure you place your own financial planning mask first, then you can prioritize other goals such as helping kids with their educations, paying off debt, and so forth. Now I’m not saying that you shouldn’t help your kids or anything like that, but just make sure you’re taking care of yourself first.

Creating a Long-Term Investment Plan for Widowhood

Next is creating a long-term investment plan to reach those goals. And like we talked about with the investment plan, that’s one of the ways that you can help make sure you’re invested properly to provide the income that you need.

Now, oftentimes we see widows, and some of the big mistakes that we see are they may not be investing their life insurance proceeds right away which isn’t a big deal. You might miss out on a few month’s returns, but take time to make sure you’re setting up a well-constructed investment plan.

And I want to talk about the three determining factors of a successful investment plan to make sure that it aligns with your goals. The three determinants are asset allocation, or how you are invested, fees, and investor behavior. So I want to just briefly talk about those.

But as you’re determining your investment plan, be sure to keep it simple. Oftentimes, not only does it help your investment portfolio be more successful, but it makes it even easier for you to manage over the long term.

The first consideration under asset allocation is to determine your investing time horizon. So when we talk about time horizon, we’re just simply trying to find the answer to the question, how long can my money be invested?

Obviously, if you’re investing money to purchase a car within the next year, you would probably invest that much differently than money that you may not need to tap into for 15, or 20 years from now. So, determining your portfolio’s time horizon is the single most important determination before you decide to invest.

As you might guess, a conservative investment portfolio is going to provide a lower expected return because there’s less risk of it going up and going down when you need to use those funds. On the flip side, a more aggressive investment portfolio will likely get a higher expected return because of the additional risk you take with it fluctuating up and down when with the market.

Understanding Fees and Investor Behavior

Now, many retirees and investors ask, well why should I even be investing and or having a portion of my portfolio invested aggressively? The biggest reason is to keep up with inflation. Like many of you are probably feeling the effects of that today, where we’re seeing the cost of goods such as groceries, eggs, and fuel rising because of inflation.

So having the right combination of conservative money to provide your income needs and more aggressive money to keep up with inflation are good components of a well-constructed investment plan.

The second part of how you should be invested is to make sure that you’re diversified. There’s an excellent analogy that I learned from a professor at Utah Valley University, Dr. Craig Israelson, who explains the process of diversification as making a good bowl of salsa.

Salsa has many ingredients as many of you know, that might be tomatoes, onions, cilantro, lime, and so forth.

Everyone has their own preference for how their salsa should be created, whether it be hotter or milder. Some might get more chunky, some might get more runny, whatever may be the case. The proper mix of these different ingredients is what creates the desired salsa.

Just like investments, the correct balance of investments or proportions of investments is what creates the desired investment results. Just like it would be unwise to make a whole bowl of salsa with just tomatoes, the same would apply to investments.

It’s doubly true if you have a stock that you received from, for example, an employer where you have a lot of your money invested in one particular company. Therefore, it’s important to include other types of investments in your portfolio, such as stocks, bonds, real estate, and so forth to create that desired salsa.

Now, while there are a lot of people who make mistakes about properly diversifying, sometimes people think that they get so caught up with deciding whether to own Home Depot or Costco or any individual company when it doesn’t make near the difference as deciding if you’re investing into stock or real estate.

So, you can kind of think of that with salsa. It’s not as important to determine whether you have a red onion or a white onion. It’s important that you have onions, tomatoes, cilantro, and the other ingredients of salsa.

So the right combination of these ingredients is what makes it a properly diversified portfolio. Mistakes may be made by simply not understanding the need to invest or not knowing how to do so, and that’s where a financial advisor can help you make sure you’re doing so.

The second determinant of investment growth is fees. And I like to think of fees in this way, if you have two horses racing and one horse has a 240-pound jockey and one has a 120-pound jockey, which horse do you think might win?

Now on occasion, some may argue that the heavier jockey could win the occasional race which is true, but for the vast majority of time, the lighter jockey would win. The same goes for investments. Generally, the least expensive investments typically win out. Therefore, the fees should always be taken into consideration when selecting your investments.

The last determinant of investing success is investor behavior. Surprisingly enough, there’s a lot of psychology that goes on that influences our investing decisions. One of the foremost thought leaders in our industry, Nick Murray, once said, “Every successful investor I’ve ever known was acting continuously on a plan. Every failed investor I’ve ever known was reacting continually to current events.”

Now, I think he was more inspired than he may realize. Not only is it acting to current events in the news, but these may be events happening politically, and things like that where really that is not what determines investment success. It’s the company’s underlying companies that you’re investing in that determine your investing success.

So, be aware of your investor behavior and your biases that may influence your investing decisions that may cause a big impact.

Now, I’m gonna switch gears here really quick and talk about the tax planning changes that happen in widowhood and talk about the widow’s penalty.

Now, tax planning for widows can be one of the greatest benefits to their financial plan. When this life-changing event happens, there are a lot of questions and challenges that arise. Things like the sale of a home, the sale of an investment property, or health insurance, all have ties back to tax planning.

Although surviving spouses end up living on less income, that is not always the case. However, their income may be subject to higher taxes even if they are living on the same amount of income. There are two main factors that determine that.

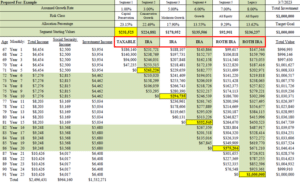

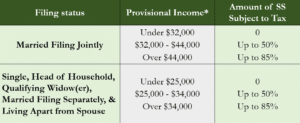

So on the slide, I’ve shown you two different tax brackets. One for those who are married, filing a joint return, and another for those who are single filers.

Let’s say that your income is $80,000 per year. For those who are married and filing a joint return, that $80,000 or the income in that bracket is taxed at 12%.

Once you move to a single-filer tax bracket, even if you continue to live on the same amount of income, that same 80,000, would be taxed at 22%, 10% more than those that would be filing a joint return. So the tax brackets are one factor.

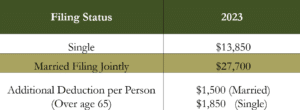

The second factor is the standard deduction. Now, for those who may not know too much about taxes, how it works is everybody gets a standard deduction that reduces the amount of taxes that they have to pay.

With the standard deduction, this is the minimum amount of deductions that the IRS allows you to take. And you can actually have more deductions than the standard, but this is the minimum amount.

For those who are under the age of 65 and are married and filing a joint return, your standard deduction is $27,700. But once you become a single person, that standard deduction is reduced to $13,850.

So the combination of a higher tax bracket as well as a lower standard deduction is what is considered the widow’s penalty. It feels like a penalty for widows when they change their tax filing status.

I’ve also included the standard deduction for those that are over 65 where that might apply, you get a little bit of an additional deduction. So that’s $29,200 for married and $15,700 for those that are single filers.

Next is health insurance which is a critical part of your financial plan. There are generally three options available to you, and there may be some others, but these are the three big ones.

For those who were living on a health insurance plan provided through an employer, you may continue that coverage through what’s called COBRA. COBRA is just a temporary insurance plan that allows you to be on it until you find another option.

Few employers subsidize COBRA, which means a surviving spouse may pay the full cost of their health insurance, plus a 2% administrative fee on top of that. So it can be a very expensive option, but this generally only lasts 18 to 24 months. So it can be an option, but it can be very expensive.

Second is the public marketplace. The public marketplace, also known as Obamacare, is an option for health insurance.

Now, you can qualify for federal assistance to reduce the amount of your monthly premiums, your monthly costs, but it’s based on your income. So as a general rule, the more income that you make and report on your taxes, the higher your monthly premiums will be. So knowing that it’s based on your income, there are a lot of planning situations that might apply.

For example, if you have life insurance, you may want to live on the life insurance for a little while or to bridge the gap till Medicare to show that you have the lowest income on your tax return possible to get the biggest federal assistance possible for your health insurance.

So a lot of planning situations can apply there. You can apply for the public marketplace during the annual and open enrollment period, which is the fall of every year, or you can qualify for a special enrollment period which is the death of a spouse or change of employment and so forth.

Lastly is Medicare. Medicare is an excellent health insurance option compared to the other two.

For the most part, it’s very affordable and has great coverage. When you are determining what to do with Medicare, you may have to decide between either going with a Medicare Advantage plan, which is kind of a package deal, or choosing a supplement plan that is generally more expensive but provides better coverage.

Whatever you choose, that determination can help determine your coverage. But, Medicare Part B and D premiums are based on your income as well. So, the higher income you report on your taxes, the higher your potential Medicare Part B and D premiums will be.

So again, if you’re a surviving spouse and your, taxes are going up, then this could also make an impact on the amount of Medicare premiums that you pay. So, it’s important to think of some of these planning strategies and how to reduce your health insurance costs as well.

So, those are the main financial planning considerations during your financial plan stage. There’s a lot more to that, but those are the kind of the main ones.

Stage Four: Transformation (46:52)

So, now I want to enter the last phase of widowhood, which is your new life or transformation stage.

When you lose your life partner, your soulmate, your best friend, it may be unimaginable to think that you’ll ever find happiness again. For some, you may feel guilty to move on or allow yourselves to ever love again. And maybe that’s not always in your case. But I would suggest that you be open to being happy again.

One of the reasons why I’m so passionate about this topic is because I get to see this transformation happen in the lives of my clients every day. And the client that I was talking about with Social Security who just got married recently, she’s happier than I’ve ever seen her. And it’s amazing to see the new and happy life that you can have.

So, I’ve summarized those different stages all together on this screen. So, the purpose of these stages is so that you can take care of yourself, take care of business, and take care of more throughout your life so that you can be left feeling empowered and financially secure. These stages were created by Dr. Kathleen Rio, who’s a thought leader when it comes to planning for widows. So take a look at her stuff as well.

Now, I didn’t talk about every single question that widows have. There are a lot of other pressing questions that you may have. And so be sure you if you don’t want to do this on your own, consider working and building your financial planning team. Maybe your financial planner, estate planner, CPA, and so forth can help you with these other important questions.

Because financial planning for widow persons is too important for guesswork, as you can hopefully see and realize today, there are a lot of nuances and things that should be done for planning for widowhood.

Key Insights (48:40)

So just to conclude, I want to leave you four key insights that can hopefully allow you to take actionable items for your financial plan.

First, understand the stages of widowhood and create your personal roadmap for now, soon, and later. Remember, there’s lots to do, but not all of it is urgent. Get organized and begin building your financial plan and if it needs to, hire the people that can help you to do so.

Carefully review your claiming options for Social Security benefits because they are unique to you and your situation, and know there is hope for a new, happy, and powered life. So thank you everyone for being with me today. If you have any questions about today’s webinar, please feel free to send me an email. I’ll be happy to answer them.