Your Intermountain Healthcare Pension Plan comes with a choice you have to make. You can take a lump sum and keep control of your assets, or choose an annuity and turn them into a steady stream of payments.

Timing matters just as much, because starting now versus waiting can change both the value you receive and the role your benefits play in your retirement planning. Ultimately, the right decision depends on your personal circumstances and a thorough understanding of what each path trades away and what it preserves.

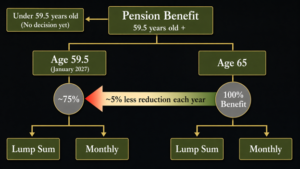

Your Two Core Choices: What You’re Really Deciding

Your Intermountain pension offer is a long-term structure choice. The option you select determines whether this benefit functions more like a steady cash flow or a flexible asset.

Monthly Annuity (Lifetime Income)

Electing the monthly annuity converts your benefit into fixed monthly payments that continue for life. The amount is determined by age and actuarial assumptions at election. Once the stream begins, it is governed by the annuity contract and cannot be adjusted.

The appeal is predictable lifetime income. The limitation is that the payment is level. Intermountain’s pension plan does not provide cost-of-living adjustments, which means purchasing power declines over time when inflation persists. Over a 25- or 30-year retirement, that erosion can materially affect spending flexibility.

Structure also affects payout. A single life annuity provides the highest monthly amount but ends at your death. A joint and survivor election reduces the payment in exchange for continuing benefits to a spouse. That structural tradeoff directly impacts household income security.

Lump Sum (A Transferable Asset)

The lump sum represents the present value of your earned benefit, calculated using interest rate assumptions and life expectancy factors. Pension lump sums are highly sensitive to prevailing interest rates, which influence how future payments are discounted into today’s dollars.

This path creates flexibility. The asset can typically be rolled into an individual retirement account (IRA), integrated with your 401(k), invested according to your allocation strategy, and drawn upon based on your personal income needs. You control timing, tax sequencing, and how this capital fits into your overall retirement savings.

The tradeoff is responsibility and market exposure. Future income depends on allocation, withdrawal discipline, and portfolio performance. There is no contractual guarantee. Instead of a fixed payment schedule, you manage an asset whose outcome reflects investment returns and risk management over time.

Rollover Strategy and Tax Mechanics: Where Precision Matters

A rollover election can be clean and tax-deferred, or it can turn into an avoidable tax problem. The difference often comes down to how the paperwork is processed and where the funds are sent. Below, we’ll cover the mechanics that often cause problems.

Direct Rollover vs. Distribution

A direct rollover sends the lump sum straight from the pension plan to your IRA (or other eligible retirement account). Because the money never lands in your hands first, it typically keeps its tax-deferred status and avoids automatic withholding.

If the plan cuts the check to you instead, it is treated as a distribution even if you plan to redeposit it later. In many cases, that triggers mandatory federal withholding, so the amount you receive can be smaller than the total you meant to roll over.

Mandatory Withholding and Early Withdrawal Penalties

When the lump sum is paid to you rather than sent as a direct rollover, two issues occur: withholding and potential penalties. Both can change how much cash you actually have available to move.1

Eligible rollover distributions paid to you are generally subject to mandatory 20% federal withholding. Additionally, if you take taxable dollars out before age 59½, you may owe an additional 10% tax unless an exception applies.2

What Can and Cannot Be Rolled Over

Most eligible lump sum distributions from employer retirement plans can be rolled over to an IRA or another eligible plan.

Ongoing pension income is different. Once you elect an income form that starts paying out as a stream, those periodic amounts are generally treated as taxable payments to you, not a balance that can be rolled over in a single transfer. This distinction is one reason the rollover decision often needs to be made before payments begin.

Understanding Integration Strategy

A rollover is only step one. The bigger win is deciding how this new account fits into a coordinated retirement-income plan, so it supports cash flow, taxes, and risk management rather than sitting in a silo. A strong rollover integration strategy typically involves:

Account placement: Fold the rollover into the accounts you already have, such as your 401(k) and existing IRAs, so your overall allocation stays intentional, and you avoid ending up overexposed (or underexposed) by accident.

Withdrawal sequencing: Plan future distributions around federal tax brackets, Medicare-related income thresholds (IRMAA), and the timing of other income sources so withdrawals stay proactive and tax-aware.

Understanding required minimum distributions (RMDs): Traditional IRA balances generally have RMD requirements beginning at age 73 (with the starting age scheduled to increase to 75 in 2033 for those born in 1960 or later), which can increase future taxable income if you do not plan for them.

Reviewing Roth IRA conversions: Strategic conversions can sometimes reduce future RMD pressure by shifting dollars from pre-tax accounts into a Roth bucket, but the tax cost and side effects should be modeled before acting.

Portfolio role clarity: Define what this asset is meant to do inside your plan, such as flexible spending, later-life income support, or a legacy reserve, and invest and draw it down in a way that matches that purpose.

A Structured Decision Framework: Matching the Option to Your Retirement Design

The goal is not to pick the “right” option in a vacuum. The goal is to choose the option that fits the way you plan to live, spend, and provide for others.

Define What You Want This Benefit To Do

Some want their pension to function like a personal paycheck that keeps showing up, even if markets are down or plans change. Others want it to behave like an asset that can be shaped around spending needs, tax planning, and long-term goals. Getting clarity on what you want this benefit to do will ground the election and keep the decision practical.

The option that best serves you can depend on the importance of the following:

- Covering baseline expenses like housing, utilities, and insurance

- Creating flexible spending capacity for travel, hobbies, and family support

- Reducing pressure on withdrawals from investments in the early years

- Providing a backstop for later years when spending patterns may change

- Protecting a spouse from an abrupt drop in household cash flow

- Building a buffer for healthcare and long-term care costs

- Supporting charitable giving goals

- Leaving a legacy to children or grandchildren

Decide Which Tradeoff You Are Willing To Live With

Once you define the job you want your benefits to do, line them up against your options and the trade each one asks you to accept. Annuitizing now tends to fit households that want income to start immediately and stay steady, while giving up some ability to adjust later if spending priorities change.

Taking the lump sum now tends to fit households that want control right away and plan to coordinate withdrawals with the rest of their accounts, while accepting that the long-term outcome depends on disciplined management and a consistent withdrawal approach.

Model The Decision The Way You Will Live It

Modeling turns a permanent election into a decision you can defend. It replaces guesswork with a set of scenarios that reflect your household, not generic averages. The best models also show how the plan behaves when conditions are inconvenient.

Important things to model and consider include:

- Your baseline monthly spending and what must be covered no matter what

- How income changes when one spouse dies, and what replaces it

- Expected inflation and how a level payment holds up later in retirement

- A longer-life scenario that reflects the possibility of living well past averages

- Taxes year by year, including brackets and how withdrawals stack with other income

- RMD timing and how it affects taxable income later in retirement

- Portfolio drawdown stress tests during down markets early in retirement

- A legacy scenario that estimates what may remain for heirs under each option

- A healthcare and long-term care stress test that reflects rising costs and changing needs

Lump Sum vs. Annuity for Your Intermountain Pension FAQs

1. How do I determine whether lifetime income or flexibility is more appropriate for my situation?

Start with the job you want this benefit to do. If you want to cover baseline expenses with a predictable check, a life annuity often supports that goal. If you want adaptability, tax planning control, and the ability to preserve remaining value for heirs, the pension lump approach tends to fit better. Your household budget, other income sources, and who will manage the money later all matter.

2. What are the tax consequences if I mishandle a lump sum distribution?

A mishandled lump sum payment can create unnecessary withholding, immediate taxable income, and possible early-distribution penalties depending on age. The clean approach is a direct rollover to avoid avoidable leakage, then a planned distribution strategy over time.

3. Can I change my mind after I elect the annuity or lump sum option?

In most cases, this is an irrevocable decision once the election is processed and the payments or rollover begin. That is why modeling up front matters. Treat the election like you would any other permanent financial commitment and make it with full context.

4. How does this decision affect my spouse or other beneficiaries?

The election affects survivor protection, the continuity of household cash flow, and what remains for heirs. A joint and survivor election can protect a spouse by continuing payments after the first death, while other elections may end at death or change benefit levels. Beneficiary goals and household income design should be discussed before you sign.

Helping You Make a Confident, Coordinated Pension Decision

Intermountain’s pension election is not a standalone form. It touches cash flow timing, taxes, survivor planning, and how much flexibility you will have in the years that follow. A clear plan brings those moving parts into one coordinated decision.

At Peterson Wealth Advisors, we work with Intermountain Health employees to compare each election path side by side, and translate the numbers into real-world outcomes. We build the strategy around your goals, your household, and your timeline, then integrate the election into your broader plan so it supports long-term stability and flexibility.

Don’t wait to get help exploring your options. If you want to see how your pension choices fit with the rest of your retirement picture, schedule a complimentary consultation with our team today.

Resources:

- https://www.irs.gov/retirement-plans/plan-participant-employee/rollovers-of-retirement-plan-and-ira-distributions

- https://www.irs.gov/taxtopics/tc557