Once you’ve decided what to do with your Intermountain Health pension — lump sum or monthly payments — the next question becomes just as important:

When should you act?

Timing can meaningfully impact the size of your benefit, your tax situation, and the long-term success of your retirement income plan. Let’s walk through the key considerations.

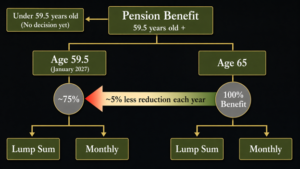

Understanding the 5% Rule

For caregivers between the ages 59½ and 65, your pension benefit is adjusted by roughly 5% per year. If you claim early, your lump sum or monthly benefit is reduced by about 5% for each year before age 65. For example:

- Claiming at 65 = full value

- Claiming at 62 = roughly 15% reduction

- Claiming at 59½ = roughly 25% reduction

On the surface, that makes waiting look like the obvious choice. But timing is rarely that simple.

The Core Question: Can You Beat 5%?

If you’re considering taking the lump sum before age 65, the real financial question becomes:

Can you reasonably earn more than 5% annually by investing that money?

If you believe (and can structure your portfolio) to achieve returns above 5% over time, taking the lump sum earlier may make sense. That way, instead of accepting the guaranteed 5% annual increase by waiting, you’re putting that capital to work immediately.

If retirement is still a few years away, time is still on your side. That lump sum can potentially grow within a 401(k) or IRA while you’re still working. But this requires:

- Discipline

- Proper asset allocation

- Long-term perspective

- Thoughtful tax planning

Without a clear strategy, chasing returns simply to “beat 5%” can backfire.

The Case for Waiting Until 65

There’s also a strong argument for patience. If you wait until 65:

- You receive the maximum pension value

- You avoid the early-claim reduction

- You lock in guaranteed growth

For someone who prefers certainty or who is nearing retirement and doesn’t want market exposure, waiting can provide peace of mind.

The guaranteed 5% annual increase until 65 is difficult to ignore, especially in a low-risk context. If you know you’ll need the income soon, maximizing the base benefit may be the wiser move.

Timing Monthly Payments: A Tax Consideration

Now let’s talk about monthly payments. Intermountain allows you to start receiving pension income while still working. That flexibility is unique — but it doesn’t automatically mean it’s wise.

Here’s a rule of thumb:

If you don’t need the income, don’t take the income.

Why?

Because if you’re still earning wages, pension payments stack on top of your salary. That can push you into higher tax brackets and reduce overall efficiency. You’re essentially accelerating taxable income you may not yet need. Waiting until retirement (when your earned income drops) often creates more tax flexibility.

The Bigger Picture: This Decision Is Not Isolated

Timing should never be evaluated in a vacuum. You must consider:

- Your planned retirement age

- Your other retirement savings

- Social Security timing

- Medicare eligibility

- Current and future tax brackets

- Your overall income needs

For example, if you plan to work until 67 and have other conservative assets, taking the lump sum early and investing it may allow it to grow more efficiently than waiting. But if retirement is just around the corner and you’ll rely heavily on the pension, maximizing the guaranteed amount may be the better fit.

This is not simply a math problem. It’s a coordination problem.

A Practical Framework

Here’s a helpful way to think about it:

- If you can earn more than 5% annually, don’t need the income now, and are comfortable with market volatility — taking the lump sum earlier may make sense.

- If you prefer guaranteed growth, will need income soon, or value simplicity — waiting until 65 maximizes the pension benefit.

Both paths can be appropriate. The key is aligning the timing decision with your broader retirement income plan.

Ultimately, timing your pension decision is one of the most financially impactful choices you’ll make in the coming years. Early action offers growth potential and flexibility. Waiting offers certainty and maximum guaranteed value.

But the right answer depends on your full financial picture, not just the 5% rule. Before making a decision, it’s worth modeling both scenarios within a comprehensive retirement income strategy.

Peterson Wealth Advisors is a registered investment adviser. Information presented is for educational purposes only. Please consult a qualified financial advisor before implementing any strategy.