Retiree Health Insurance: What to know for Open Enrollment – (0:00)

Daniel Ruske: Today’s webinar is health Insurance for Retirees, and I’m joined by Lisa. I’ll give her a chance to introduce herself in here in a moment. We do expect this webinar to go a little bit longer than 30 minutes.

I’m thinking it’s going to be closer to 45, potentially longer, with the question and answer at the end. So we hope to jam pack it with, with helpful information, so it’s well worth your time.

I have on the Zoom call with me, Jeff Sevy, who is operating the question-and-answer feature below. So, if you have questions through, we as we go, feel free to go ahead and send that to Jeff. He’ll be able to answer them.

If for some reason we’re unable to get to them or we don’t know the answer, maybe we need to do more research, you can email us at info@petersonwealth.com.

And then at the end of the presentation, as always, we have a survey. You can give us some feedback on how well we did, what you liked, what you didn’t like, and then also I think most importantly, you get to kind of vote or make a comment on what you would like to see and for information for future webinars.

So today we have a guest with us, Lisa Evans. So Lisa, I’ll let you just take a minute or two to introduce yourself and tell us about you.

Lisa Evans: Hi, am Lisa Evans. I’m grateful to be here. Thanks, Daniel. I do Medicare insurance. I am a licensed agent and have been in the industry for a few years now, and love helping retirees or those turning 65 to kind of take care of their senior benefit options and figure out how to make their golden years golden and not have to stress and worry about the side of insurance.

I have five kids. I only have two left in the house, so I’m, we’re slowly launching people and just enjoying the last few years we have with some of them that are home still.

Daniel Ruske: Awesome, so those last two, they’re the spoiled ones. They get to be on the cruise with you.

Lisa Evans: They’re feeling spoiled this week.

Daniel Ruske: That’s great. Well, very good. Really quick, here’s a quick disclaimer. This information that’s provided on this webinar today is not intended to constitute any investment, legal, tax, or insurance advice. It’s for education purposes only.

So we’d love to get you in contact with a CPA, an attorney, a financial advisor. Obviously that’s what we do. A health insurance professional, what Lisa does, but we wanna make sure we know your situation individually.

Well, here’s a quick agenda of what we’re hoping to cover during today’s webinar. First, we’re gonna talk about the different health insurance options for retirees. Then for those of you under age 65, we’ll focus on the marketplace insurance, including how it works, the important upcoming changes.

We’re then gonna spend a lot of time talking about Medicare, and that’s why we have Lisa, for those of you older, over age 65, we’ll talk about enrollment tips as well as the costs, and also discuss the differences between advantage and supplement plans. So that’s today’s agenda.

Well, let’s talk briefly about health insurance options for retirees. Now, we break this down between before age 65 and then after age 65 options. If you are younger than age 65 and you stop working, you’re gonna need health insurance.

You can hop on marketplace, you can pay for a private plan to get coverage there, or you might also have a spouse that’s still working through their employment and can get coverage through their, your, their, your spouse.

And then even some employers offer kind of a retirement benefit where you can either they either subsidize it or you can pay for the health insurance coverage until you hop on Medicare.

Now, what is not mentioned on this list, but probably should have been was, is Cobra. Cobra is kind of an extension of your employment insurance. It’s not necessarily a long, long-term solution, but it, it definitely can bridge the gap to Medicare.

Also a strategy if you’re a member of the church and choose to serve a mission before the age of 65. If you’re a full-time away from home missionary, you can jump onto the church’s senior service medical plan. This is adequate coverage that you can pay for that can cover you until 65 where you help on Medicare once again.

Now, for those of you over the age of 65, we’re gonna be talking about Medicare. There are probably some other options, but for pretty much every American, you’re gonna jump on Medicare at age 65 or when you retire, whichever comes later. So for the purpose of this webinar, we’re gonna spend the majority of our time talking about the marketplace insurance for those of you under age 65. And then for those of you over age 65, we’ll talk all about Medicare.

If you do have questions about some of these other options we’d happily talk to you, but we’re not gonna be tackling them during today’s presentation. And then specifically, if you have questions about the senior mission health insurance, we have webinars already recorded. We will happily get you a recording of that and get you the information that you need there.

Overview of the Marketplace – (5:14)

Okay, we’re diving into pre 65 insurance. To give you an overview of the marketplace in March of 2010, the Affordable Care Act, or also called Obamacare, was passed with the goal of making health insurance more affordable. The law also may offer individuals and families government subsidies or call also called premium tax credits. These help lower the cost to the monthly premiums for the households. Some states offer their own exchange, but for most states, including here in Utah, the federal government is the one who operates the health insurance marketplace.

Now, you can see their website on the page there is healthcare.gov. I’m actually gonna take us there, here in a few slides to show you kind of a quick tour and how you can shop prices there. I do also want to add here that you can utilize a health insurance professional to help you select an Obamacare plan.

The healthcare professional is compensated from the plan that you select. And so what’s nice about this is you can use somebody who’s done it dozens of times, they can kind of hold your hand, help you select a plan, and then you actually pay the same amount for that plan. And so it is kind of a good service.

I don’t really see a downside. If you wanted to use a healthcare professional. Lisa, I believe you’re licensed to do this, but your expertise is Medicare, is that right?

Lisa Evans: Actually I only do Medicare, but I do have coworkers that do the marketplace if they need help with that or a referral.

Daniel Ruske: Awesome. So reach out to our office. We’ve got a couple others that do the pre 65 insurance, and then it sounds like Lisa does too.

Okay, well, how does it work? Well, during open enrollment, which runs annually from November 1st through December 15th for coverage, starting the following year, you’ll fill out an application with your basic personal information for both you and those in your household who will be covered.

Included in this application will be your best estimate on your income for the following year. An important note here is marketplace does not use your previous year’s income, but rather you are projecting your income for the following year. So essentially, you have to guess what your income will be in the year before your premiums you’re about to pay.

So we’ll talk in a slide or two about what happens if you don’t estimate accurately. But for now, just know that you do have to estimate your income, and that’s gonna depend, that’s gonna change your monthly premiums for this.

As I mentioned before, you qualify for subsidies based on the income that you report. Any household that reports income between 100% of the federal poverty level and 400% of the federal poverty level will receive a subsidy. The more income you report, the lower your subsidy is going to be.

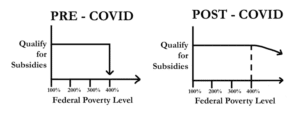

I do want to make a major note here, and if there’s one thing from today’s presentation that I want you to take away, especially those of you under age 65, is this. That the income required to qualify to receive these subsidies is changing in 2026, you’ll no longer be able to make over that 400% of the federal poverty level and receive a subsidy.

To give you some history, as part of the American Rescue Plan during COVID, these subsidies were extended to those with income beyond 400% of the poverty line. This means that you could make over 400% and you would still get a subsidy. It would simply just taper off as you see on that left hand side, you’d simply receive less and less until you went to zero. That is no longer the case.

Starting 2026, if you cross that 400% of the federal poverty line, even by $1, you’ll lose 100% of your subsidy. As you can see on the right hand side, it’s a cliff. You will, you’ll fall off that cliff if you cross that.

So how much is 400% of the poverty level? Well, I’ve got it highlighted here. You can see on the left hand side the household. If you’re a retired couple, empty nester, maybe, then you can follow the line to 400% 84,600. If you’re single, potentially have a kid or two at home, you can, you can look at your respective household size, but that is going to be the, the 400% of poverty level.

This is 2025s. 2026s has not been published yet. A quick Google search will tell you, but just be aware of that. It typically does go up every year, but, this is 2025 per now.

Okay, here is another graph showing exactly the same thing, but I feel like it displays the difference between 2025 and 2026. Much more clear. So going from left to right, this is the income that a couple at age 64 could make. And then from on the vertical access, you can see the amount of subsidy they would get.

If they only made $35,000 per year, they would get a $25,000 subsidy in federal subsidy to help pay for the health insurance. And then as their income gets higher, the subsidies become less and less.

And then if you can see, I know it’s kind of small here, but the income between $84,500 and $95,000, that subsidy in 2026 goes straight to zero, whereas before this subsidy would be tapered off until eventually hit zero.

So if you are on Obamacare and are currently receiving these subsidies, let’s talk to make sure that your income for 2026 is gonna fall in the right spot and that you don’t cross this 400% of the poverty level for your household and potentially increase your health insurance by $18,000.

So, okay, for this next part, I actually am going to change my, let’s see if I can share my browser here. I wanna give you a quick tour of healthcare.gov. So I’m gonna just throw this on the screen here.

As I mentioned, the website is healthcare.gov. If you’re ready to enroll, you can hit get coverage or apply for coverage. But today we’re gonna just browse plans and costs.

I’m gonna go ahead and just put the zip code for the office here in Orem. Once again, Utah is based on the federal. If you put in a zip code and your state is run on the state level, it’s gonna divert you to their website.

We’ll now, fill out the application here for our household. I’m sorry, I said application, but this is a quote for our purposes today. I’m going to say that I’m 64 years old and that my wife and I need insurance. I’m gonna say you and another person, hit continue. Are you married? Yes. Do you have any other dependents on your tax return? No, for this, in this case, we’re empty nesters today, and I’m gonna say that I’m 64. I am a male. Am I eligible for any other insurance through a job, Medicare, Medicaid? No. Am I a parent of anybody under 19? Not today. Not pregnant. I don’t use tobacco. I can hit next. This is for my spouse today. She’s also 64, female, and none of these apply to her as well.

So we can continue that. We have our household here, and this is gonna be the major factor here. You can put in your estimate and it will then show you what subsidies receive for 2025. As a reminder, this is showing 2025. It will update in the coming months for 2026. I’m gonna put $75,000 under that household of two 400% of the poverty level.

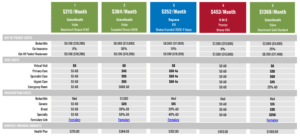

I’ll hit continue. And for a couple of 64 year old’s that, uh, report $75,000 of income, my spouse and I are going to share a subsidy per month of $1,623. And so this is gonna be applied to our plan. I’m gonna hit view plans here. And you can see here on the right hand side, they group the plans by bronze, silver, gold, platinum, bronze is gonna be the cheapest and the worst coverage. Platinum is gonna be the most expensive, the best coverage.

And so just know that there, the cheapest option for us here is the regions Blue Cross of Utah. You can see this plan was originally $1,700 per month. We apply the tax credit of $1,623, and so my spouse and I can get coverage for $110 per month. Now, as you can see here, the deductible is not pretty.

So this is more kind of a catastrophic plan. But if you wanted to, you can add a filter here. You can look for an HSA eligible plan, if that’s what you’re looking for. You can also search for some of these more expensive ones and better coverage. So I’m gonna select the gold plans, apply the filter here. You can see Molina is offering a plan. It was $2,100. After I $1,600 tax credit, I’m gonna have to pay about $535 per month. You can see the deductible is a lot more affordable.

And then obviously, feel free to scroll through these. You can see if you’re maybe looking for like Select Health I know works well with a lot of these in the area.

So anyway, it’s gonna be a different for everybody. And then also it’s going to be, um, specific to the area. And everybody’s gonna look for different types of coverage here. So let me see if I can get the screen back up here and hopefully that looks good there.

So one thing I wanna say is when it comes to selecting individual plans, that is where we will refer you to a health insurance expert, somebody who is doing this all the everyday. Here at Peterson Wealth Advisors we feel very comfortable projecting your income and helping to make sure that falls where you want it to be.

I don’t feel comfortable going over your prescription list or your favorite doctor and surgeon and getting you a plan there. So we’ll help you estimate your income, get you this number to put into that, that box there. And then at that point in time, the health insurance professional is gonna help you kind of take, take it from there and select the plan.

Here’s a quick summary of the plans in Utah. This is only helpful if you’re local, but you can see here, a lot of different options and then you can see the doctors and hospitals that are covered. And then as a reminder, open enrollment is November 1st through January 15th.

Okay, we’re now circling back to answer the question, what happens if my income doesn’t end up being exactly what I projected on my application? Well, the answer is you will reconcile any differences when you file your tax return.

If your income was way less than what you projected, you’ll get a credit for the subsidies that you should have gotten along the way. It will then be given to you in the form of a tax refund.

If your income was more than what you projected, you were receiving a higher subsidy than, than you should have been, you’ll actually have to pay back that subsidy if you cross that 400% of the poverty level, potentially the entire thing.

So a lot of people end up on the wrong side of this. And so I’ll just add here, if your income does change throughout the year, you’re able to go back into healthcare.gov and change your income to make sure that you’re paying as accurate as possible each month for those premiums to make sure that you’re not surprised come tax time.

I do wanna give you just a quick real world example. Some of the things we do for our clients here, here we have an example. David and Susan, they are retiring at the end of this year. They’re 63 years old, and they need insurance for two years before they hop onto Medicare at 65.

David and Susan have accumulated $1 million in retirement assets. They have $900,000 in 401k/IRAs, and then they have a hundred thousand dollars in a brokerage account or bank account.

David and Susan would like to have $8,000 per month, or $96,000 a year in retirement income, and they haven’t started Social Security yet and they have no pensions. So essentially we have complete control over what their income is going to be on their tax return.

So rather than sending the full $8,000 per month from all of the, the 401k/IRA taxable accounts, we will send only up to, or just before 400% of the poverty level from these taxable accounts. And the rest we’re gonna send from the bank or brokerage accounts to make sure they qualify for these subsidies.

By doing this, David and Susan get to spend their desired monthly income in retirement, but then they also get to qualify for around $18,000 of health insurance subsidies per year until they hop onto Medicare.

To wrap it up here, the marketplace insurance, before I turn it over to Lisa, just wanna take a moment to explain how marketplace insurance can fit into your financial plan. Healthcare is an important part of any financial plan, so understanding it is critical.

Now, marketplace can be a great option to use until Medicare kicks in, but it’s important to be able to have a clear idea of what your income will be in retirement. Because the marketplace uses your best estimate of your income to qualify for a subsidy, having a sound financial plan in place that allows you to pinpoint what your income is going to be in retirement is extremely helpful. So you don’t have any tax surprises come April when you file.

Another important aspect for marketplace is that there may be ways that you can qualify for a higher subsidy by reporting lower income for tax purposes, while at the same time providing you for that desired cash flow in retirement, like we talked about with David and Susan.

This is just another reason why we recommend having a retirement plan. Again, if you have any questions about the the retirement plan or the the health insurance, please let us know. We’d love to talk about your situation.

Medicare Planning – (19:31)

Daniel Ruske: Okay, I know that was a lot, but that is, that wraps up the, the pre 65 insurance. And so at this point we’re gonna be talking about those of you who are leading up to 65 or 65 and older. And so Lisa, I’ll let you, they jump in and tell us about Medicare.

Lisa Evans: Thanks Daniel. I also wanna echo what Daniel said with just having a financial plan in place. Because sometimes even with Medicare and the insurance that you put in place, knowing what you have to work with and your income that you’re gonna be able to retire on can help that planning as well. So it’s important to kind of have all those pieces in place.

So really quick, just kind of understanding what Medicare is. There’s Medicaid and Medicare, and I often hear people say, you know, I’m getting Medicaid or I’m getting Medicare, and they don’t necessarily know the difference between the two.

So Medicaid care is where the health department, it’s the National Health Insurance Program for people over 65. And so it’s the care of people over 65. Medicaid is the aiding of people who are financially struggling. So Medicare is for your care. Medicaid is for aiding people. So we’re gonna talk about Medicare today.

It’s administered by the center of Medicare and Medicaid Services. So everything’s regulated by CMS and your enrollment into Medicare is done through the Social Security Administration. So as you apply and things like that, we’re gonna use Social Security to do that or socialsecurity.gov to do that.

Everyone over 65 is eligible for Medicare. This includes all US citizens and legal residents who have lived in the US continuously for at least five years. Some people under 65 can get Medicare if they’ve received Social Security benefits for disability over more than 24 months. They have ALS or end stage renal disease.

But in our discussion today, we’re just gonna talk about people that are over 65. There’s a lot of things in the fundamentals of enrollment and I’m excited to talk to you a little bit about those today.

First, we’re gonna start with enrollment and understanding that this is really important. Unless you’re covered by credible employer work insurance, you must enroll in original Medicare when you turn 65. So I’m gonna refer to original Medicare as what the government requires you to do.

So unless you have a credible work employer group plan in place, you have to enroll in original Medicare when you turn 65. Meaning you or your spouse can be working and you can get work insurance through either one as long as you’re employed.

If you’re no longer employed and you have a retirement plan with your work, it’s not considered credible. And as long as that stays in place forever, that’s no big deal. But if you ever lose that insurance, you’ll have to go back and apply for part B and A, and there can be penalties for that. So it has to be credible work insurance. If you aren’t sure whether yours is credible or not, you can always ask your HR department. They have a letter that defines whether or not it’s credible and they’re required to, to send that out and give that information to you.

If your employer has under 20 employees, you’ll also need to check with your employer to see if your required to enroll in both parts A and B to get your healthcare services. A lot of times if it’s a small company, you will be required to enroll in parts A and B in order to maintain that insurance.

Another thing to evaluate is even if you have work insurance, sometimes those copays, those max out-of-pockets and deductibles can be expensive. Sometimes your premiums are expensive. So it’s worth comparing original Medicare and your work coverage and seeing which option is financially better for you.

Sometimes it’s better to stay on your work insurance and sometimes it’s better to go onto a Medicare program and the benefits are a little bit cost effective or cheaper or things like that for you. So something to look at and to evaluate. And you can ask an agent like myself or a healthcare care professional to help you evaluate that. They can help you compare different plans and different options and look at the summary of benefits between the two programs.

So what if you don’t enroll in Medicare on time? The consequences can be pretty dire. First, you’ll be charged a late enrollment penalty, and the longer you go without enrolling, the higher the penalty will be and it’ll continue for the rest of your life. So they’ll apply that a penalty for your premiums forever.

Second, sometimes your healthcare expenses may not be covered simply because if they require Medicare as your primary insurance and then you have a secondary insurance, but you don’t have that primary insurance, the secondary insurance will be waiting for Medicare to pay. If they never pay, then your secondary insurance won’t kick in and they won’t cover anything, so you’ll be left with the entire bill. So there’s a risk there by not having that.

And the last thing is that sometimes your in private insurance options are limited because some of those things, if you wait too long, they go through underwriting or health screens screening or things like that, premiums can be higher. And so it’s important to look at your options right when you’re able to enroll so you can avoid those penalties and those different things.

If you’re receiving Social Security when you turn 65, you will automatically be enrolled in parts A and B. So if you’ve already taken out Social security in three months before your birthday, they will send you the red, white, and blue card and have you enrolled in parts A and B.

Now, if you’re still working, but you’re taking Social Security and they send you this automatic enrollment to parts A and B, but you wanna stay on your work insurance, you can decline Part B.

There’s an application that you have to fill out some paperwork that has to be done. My email will pop up at the end of this. If you wanna reach out to me, I can send you that paperwork and those application forms to help you submit that and go through the process of how to do that.

Supplement and advantage plans or Part D or different things like that, those insurances are not automatic, even though your Medicare is part A and B are. And so you’ll have to choose to proactively get enrolled in those plans before your birthday or your open enrollment window closes.

Your coverage will start on the first of the month you turn 65 when you’re automatically enrolled. So if your birthday is June 15th, your coverage will begin on June 1st.

So the initial enrollment period for those who aren’t covered by a group plan or who aren’t automatically going to enroll will start three months before you turn 65 and last three months until after your 65th birthday. So you have a total of a seven month window.

So before, if you enroll before you turn 65, your coverage will start on the first of the month that you turn 65. Going back to June 15th, if your birthday is June 15th, it will start June 1st.

If you enroll the month of your birthday, meaning you wait till June to enroll, your coverage will start the next month. If you wait two months or month, it always enrolls or starts the month after you’ve enrolled in the program.

So they won’t retro it except for on the third month, if you sign up on the last of that window, they will retro it to the beginning of that month. Other than that, it’s, it’s always the month after you put the application in the cat.

There is one little situation that that’s different, and that’s if your birthday happens to fall on the first of a month. So if your birthday was June 1st, your coverage would actually start May 1st and your window would open three months before that.

So you would actually have your window open in February instead of March. So if your birthday happens to be the first, you can pay attention to that one little window that will open up a little bit early for you and to be able to get that coverage started sooner.

There are special enrollment periods, and these are for people who are covered by employer group plans. So when you turn 65 and you have work insurance, you do not have to enroll, but when you decide that you want to retire, you can get your part B in place anytime before your coverage ends, or you have an eight month window after your coverage ends that you can get your insurance in place.

I would always advise to get your coverage in place before your old coverage ends, just so you don’t have gaps in your insurance coverage, but you do have a window there if for some reason you feel like you wanna take advantage of that.

Part D is your prescription drug coverage, and that window of coverage is only 63 days from the time it ends. So you’ll wanna make sure that you, you don’t miss that.

You wanna avoid late penalties by enrolling on time, making sure that you pay attention to your special enrollment periods and you’re avoiding the gaps. And most importantly, just kind of be ahead of the game so that you can make sure that you don’t have gaps in your coverage and that you keep the coverage you need.

So the question is, how do we sign up for parts A and B? And it’s pretty easy. You can go to socialsecurity.gov and there’s a little tab that will say Medicare, you’re gonna click on it, and then a big bar you can see on this slide that says Apply for Medicare benefits. You can click on that or you can call Social Security, at the 1-800 number.

This number, just so you know, you’re gonna be online for a little while waiting. It’s a really slow response time. There are local numbers that are way faster. If you wanna reach out to me, I can email those to you. If you’re applying for part B and or Medicare when you turn 65, this is really easy to do online.

If you are retiring and you’re after 65, you’re gonna need some forms and you’re gonna have to drop those off in person. So if you need those forms, feel free to email me and I can email those forms back to you.

You usually will take those forms, have your HR person fill out their portion, you fill out your portions of the forms, and then you’ll drop those off at the Social Security office and then they’ll process them that way. So that’s kind of a little bit about that enrollment.

Okay, we’re gonna talk really quick about what original Medicare is and what it looks like. Okay, so first original Medicare is what covers or part a original Medicare Part A is what covers your hospitalizations, your skilled nursing facilities, your home healthcare and your hospice. It is free to those who have worked or their spouses worked for 10 plus years and paid Medicare taxes.

If you don’t qualify for part A for free, you can pay a monthly premium to get the coverage. For this presentation, we’re gonna assume that everyone here is getting it for free. If you have questions about that premium, you can always reach out to me, but as long as you’ve worked for 10 or more years, you or your spouse and pay those taxes, it’s gonna be a free premium. It’s typically free for most people.

So Part A does have deductibles, copays, and co-insurances. And one of the things that’s important to understand about original Medicare is that there is no max out of pocket. So if you go to the hospital and stay for a week, you can see from this chart it’s a deductible of $1,676. And if you go back to the hospital sometime within a year that’s more than a 30 day break after your first visit, you’ll pay that deductible again. And heaven forbid you end up there three times, you’ll pay it again as long as there’s more than a 30 day break between the previous visit.

So with no max out of pocket, you can see that if something catastrophic happened in your life, that could add up pretty quickly.

Part B has a monthly premium of $185 for 2025. Rumor has it that this is gonna go up to about $200, $206, something like that for next year. This part covers your doctor visits, your emergency room surgeries, radiology, any type of emergency care, things like that. So this is kind of gonna be where the bulk of your coverage is going to come when you need things.

And the thing to understand about original Medicare is that if you’re to stay on original Medicare each year in January, you’ll have a $257 deductible for each calendar year. And then after you reach that deductible, you’re gonna have cost sharing of 80/20 for all approved services for the rest of the calendar year.

So let’s go through an example. If you had knee surgery in January and that cost of that knee surgery was $60,000, you would pay your annual deductible of $257, and then you would pay 20% of that surgery, which if it was $60,000 would be $12,000.

And if in November you slipped on some ice and broke your arm and had to have another surgery, which cost another $40,000, you’d pay another 20% on that surgery as well, which would be another $8,000. So with original Medicare, again, there’s no max out of pocket. So if those two scenarios happened in the same calendar year, you would pay the $20,000 out of pocket after you paid your $257 deductible.

So as you can see from this example, not having a max out of pocket puts you at risk for a lot of expense should anything catastrophic happen in your life.

Also understand that Medicare doesn’t cover everything. There is a Medicare and new booklet that they send out that you can access to on medicare.gov has 20 pages talking about all the things that Medicare does cover and only one page talking about what it doesn’t.

There’s a lot of things that aren’t necessarily going to probably make a big difference. Maybe not cosmetic surgeries or things like that. They don’t cover long-term care, but they also don’t cover any dental vision or hearing in original Medicare and some of these other things. And so these things you have to cover yourself, that’s all out of your own pocket.

We’re gonna pause for just a second talking about original Medicare and talk a little bit about those premiums. I’m gonna turn the time back over to Daniel. He’s gonna talk to us a little bit about the premiums with original Medicare and how those can vary depending on your income.

Daniel Ruske: Perfect. So you get too many numbers on this screen and, and then it’s, it’s my turn again, I guess. I just wanna take a minute and explain this. First of all, this is IRMAA, so this is the income related monthly adjustment amount.

And so the way this works is you pay, like Lisa mentioned, $185 per month for 2025. We don’t have 2026s yet, so just be aware of that. Like she mentioned the speculation about, what’d you say, $206 or so. And this is gonna be per person per month for Medicare Part B and D.

So if you make less than a certain amount, then that’s what you’re gonna make, that’s what you’re gonna have to pay per person per month. So the graph shows how much more you would have to make to increase your original Medicare premiums per month.

Now they don’t make it super simple. Your income in 2025 does not determine your original Medicare premiums in 2025 like it did in the Obamacare, right? Obamacare, you project for the year and you look at that actual year. This is not the case for Medicare. They actually look back two years.

So your income you made in 2023 is going to determine your original Medicare premiums in 2025. So once again, for the premiums you’re paying in 2025, you are looking back to 2023’s income. You’ll see a single filer on the left column and then a minoring filing joint there in the middle column showing what income you would have to be be at.

Once again, this is modified Adjusted Gross Income to have those increased premiums. So for instance, if a married finally couple, if you made over $212,000, then in 2025, 2 years later, your premium’s gonna be up to that $272 per person per month.

So this becomes difficult to start planning because as I mentioned, we don’t have 2026’s numbers yet, but as we know, 2024, that income is already in the books. It’s already been filed. So we’re making projections on as to where your income will be in 2024, to calculate your premiums for 2026 before they even publish the brackets.

And one important note here, these brackets work also similar to the cliff as the pre H 65 insurance, where if you cross into the bracket by even $1, you will pay more for your original Medicare premiums two years later.

And so we have to be very careful when we’re looking at Roth conversions and these tax projections to make sure that we leave a sizable buffer to make sure we don’t accidentally cross into one of these higher IRMAA brackets. Just to kind of get you familiar with that name, and cross that threshold.

So this says the same thing just laid out a little bit differently. Once again, for 2025s premiums, we are looking at the income on 2023. And then at the same, the same planning scenario kind of works out for Medicare as it did for the pre 65 insurance, where we can manipulate the income on the tax return by sending clients the money from the correct bucket, whether it’s taxable or non-taxable, to make sure we don’t cross into one any of these unwanted added insurance costs.

I’ll kick it back to you, Lisa.

Medigap/Supplement and Medicare Advantage Options – (37:28)

Lisa Evans: Okay. One thing I think too, Daniel can also help you with besides keeping yourself inside those tax brackets is that after you turn 65, there are rules and regulations about you continuing to contribute to your HSA account and there can be tax fines if you can continue to contribute after 65.

And so Daniel and his team might be great resources on understanding at what point you need to stop contributing and where you need to go from there so that you don’t incur those fines as well.

So the next thing we’re gonna talk about is our options of how we can remove the risk of those no max out of pockets with original Medicare from yourself and place those risks into the responsibility of an insurance carrier, thus protecting yourself and your finances from catastrophic events in your life.

There are typically two options to place put in place with original Medicare, and no matter which option you decide to go with, you will have to keep original Medicare’s parts A and B to add these options, and you’ll always pay part B monthly premium, which again, this year has been $185.

So just know that no matter what you decide to add or put onto your plan, you’re gonna always pay that part B premium.

The first option that we’re gonna look at is a Medicare supplement or a Medigap plan. Sometimes they’re referred to as as synonymous. A supplement and a Medigap plan are the same thing.

Medicare is referred to as in parts. So there’s part A, part B, part C, part D, where Medigap plans are referred to as plans and they’re different. Medigap plans are standardized. They’re identified by letters A through N. So if you buy a Plan F in California, it will be the same offer, the same benefits as a Plan F in New York.

However, the premiums can vary considerably from company to company and from area to area. For example, in one Florida County, the monthly premiums for Plan F ranged from $192 to $465 per month for exactly the same policy.

So this is really important why you have to evaluate your Medigap insurance because a lot of them charge differently, but they are required and regulated to provide the same benefits and just often charge different fees.

Medigap policies are issued by private insurance companies. They’re designed to fill the gaps that Medicare doesn’t cover. And though they are not affiliated with Medicare, they do have to follow certain federal and state laws designed to protect to protect you.

We’re going to talk about Plan G just because it’s the most inclusive plan that’s available for anybody that turns 65 after 2020.

So if you look at this chart, you can see there’s other options, but again we’re gonna just refer to plan G. If you’re interested in the Medigap options, we can kind of look at the different pricings and different places, understanding that the different plans have less coverage and so they are cheaper, but you will sacrifice some of that coverage.

The reason they call these Medigap plans again is because they fill in the gaps of original Medicare. So you still pay your part B premium and you would also pay a monthly premium for the Medigap plan. You would also pay an annual deductible, that $257 annual deductible, and then Medigap Plan G would pay all of your copays, cost sharing, and co-insurances for anything that’s covered by original Medicare.

So we’re gonna go ahead and look at our example that we talked about with the knee surgery before. So if I have knee surgery in January and I’m on a Medigap plan G, the cost of that surgery is $60,000. I would pay my $257 annual deductible, and then the surgery co-insurance of the 20%, which would’ve cost me 12,000, would be paid by my Plan G.

And then if I slipped on ice in November and broke my arm again, that other surgery would cost $40,000 and my cost sharing would’ve been $8,000 would be covered by Plan G.

So what would happen is, if I was on Plan G, I would pay my part B premium, I would pay my monthly premiums for Plan G, and then I would pay my annual deductible, and that would be all that I pay. And Plan G would pick up the expenses on both of those surgeries, that $12,000 and that $8,000.

So it can save a lot of money for some things that happen that are are large and catastrophic, but you do have a constant payment each month. So the pros of a Medigap option is that the primary insurance is original Medicare, so you’re gonna keep your original Medicare and then the Medigap fills in those spaces.

A nice thing about a Medigap plan also is that there’s no networks and you can choose anywhere that med original Medicare covers or accepts, you can go to those type of places. So it travels really well across the United States. You can go see doctors anywhere you want in the US.

It’s also guaranteed renewability, meaning once you have that plan in place, they can’t kick you out. If you have health problems or issues when you turn 65 or the first time that you enter the Medicare market, it retirement, you’re guaranteed issuance, they can’t reject you because of previous health problems. And then you maintain that guaranteed renewability as long as that plan is in place.

And once you pay your monthly premiums, there’s no, or little to no out-of-pocket costs except for those monthly premiums and that annual deductible. The cons of a Medigap plan is that those monthly premiums can increase with age. There’s not prescription drug coverage included. The policies may have to be underwritten. That’s meaning if you didn’t jump in one of those guaranteed issuance windows, meaning turning 65 or retirement. If you want to go from an advantage plan to a Medigap plan later, you have to go through underwriting then. And some of those additional benefits like dental hearing and vision are still limited on these plans. So there isn’t always coverage in those ways.

There is not one best option for everyone when it comes to picking your insurance coverage. With a Medigap plan, you pay the same premium each month, but you pay for very little along the way as you go to the doctors and things like that. You pay a premium to the carrier for the carrier to assume the risk which could be about $200 with prescription drug coverage included. With a Medicare Advantage plan, you pay a lower monthly premium if at all, but you’ll pay co-insurances, cost sharing and max out of pockets, and things like that.

So we’re gonna talk a little bit about those advantage plans in just a second. We don’t have time to go into all the details, so it’s important to get some help. Looking into those options, you can reach out to someone like myself. You can go onto medicare.gov. There’s different ways to to kind of sift through all that information that’s available.

Really quick, just because it goes along with original Medicare and the Medigap plan is the prescription drug coverage. This is what they call Part D, and Part D is simply prescription drug coverage. It is required by Medicare for you to have prescription drug coverage or Part D in place.

If you do not, there are penalties that do incur for this as well. If you don’t have a plan. It’s offered by private insurances who contact contract with Medicare. Each prescription drug plan is slightly different. So not every carrier is going to cover every prescription drug the same. So it’s important to shop carefully for your drug plans.

Agents like myself can take your prescription drugs and look at the different carriers and compare the coverage for you and help you to see which plans will cover your drugs most inclusively.

There are also some inexpensive drug plans available. So if you don’t take a lot of drugs and you’re like, I just have to have this because I have to have that, there are some inexpensive ones in place that you can put just to avoid that penalty.

The second way you can get Medicare coverage is through Medicare Advantage plans. And this is typically what you see all the commercials on TV about and are throwing out all these different incentives of things like come get thousands of dollars in grocery benefits and things like that. A lot of the things you see in the commercials are meant for people who qualify for Medicaid and Medicare.

So don’t be bamboozled by all the commercials you see, not everything there is true and honest for everyone that is out there. They’re usually very limited on who can qualify for the stuff that the commercials talk about.

Medicare Advantage plans are also offered through private insurance companies that contract with Medicare. Medicare pays an amount to the plan for each member’s care, and the plan is responsible for providing that care. Advantage plans look a lot like your typical insurance that you’ve had for most of your life. There are many companies in the area offering advantage plans.

So if you go this route, it’s important to shop for plans and find one that meets your needs. You will have to use their doctors in network and their hospitals in network, and you’ll wanna a plan that includes your prescription drug coverage. So you will want to look up and see if your doctors and prescription drugs are in their network before you enroll in a specific advantage plan.

Again, an agent like myself, or there’s websites that you can go individually to each carrier and enter in all of your information and they can show whether or not you’re in your network.

You may be able to get extra benefits on advantage plans. They often include dental hearing and vision. They often include things like gym memberships. They sometimes include over the counter benefits. Sometimes they have grocery benefits if you have some type of chronic issues. So it’s important to shop carefully to find plans that will fit your needs.

Part C and D are provided in an advantage plan. So an advantage plan to me looks like a big circle that incorporates everything. It wraps it all up and puts it in kind of a little package for you. So it’s gonna cover that part A, it’s gonna cover that part B, it’s gonna cover your prescription drug coverage, put it all in, and then it’s gonna give you some other things as well.

But like your typical insurance that you’ve had all along the way, you’re gonna have possibly deductibles, premiums, copays and co-insurances that you’re gonna pay along the way.

Medicare Advantage does offer some really great things. All your preventative care has to be included. So most of the time these plans will offer preventative care for zero copayments and co cost sharing. You do get pretty low monthly premiums on these plans. And so you, the pros of a Medicare Advantage plan is that you’ll have a low monthly premium, you’ll have prescription drug co coverage, you will have a max out of pocket, which original Medicare doesn’t offer you. So you do have the limited max out-of-pocket limits, and you can get those extra benefits.

The cons of a me Medicare advantage plan is that you have to be inside the provider networks. The plans can change from year to year. Some of the things inside of an Advantage plan still have only 20% coverage of co-insurance, so they still will only cover it, the 80/20, and your healthcare will be managed by the insurance company. And so they kind of decide what that’s gonna look like and how that works.

So it’s a big decision and it needs to be individualized. There’s not necessarily a right or wrong answer, but it is something that you wanna be thoughtful about because it does determine a lot of how your care will work for throughout your retirement.

Okay, this image shows two ways to have Medicare.

So on the left side you can see that your original Medicare is the part A and the part B, and if you keep original Medicare, you add the Part D, which is under that, that’s your prescription drug coverage. And then you have that option of adding the Medigap plan.

So that would be option one is you put that all in place and keep the coverage that way. And option two is gonna be the right column, which is a Medicare Advantage plan, and it takes in and puts the A, the B, and the D altogether into a plan, which again would have those premiums copays max out of pockets and things like that as you go.

So in this last slide, you’re gonna see what it really is comparing the two, what you’re facing. So with the doctors in a Medicare supplement plan, you can go to any doctors and hospitals as long as they accept original Medicare.

Where in an advantage plan, you’re gonna be required to use the hospitals and doctors that are in the network of the plan you pick. In a supplement plan, you do not have to get referrals to see specialists in an advantage plan. There are some networks that require referrals and some that don’t. It kind of depends on which plan you pick.

With a Medicare supplement plan, you’re not restricted to the network, where in a Medicare Advantage plan, you are required to stay within their networks.

In a supplement plan, you can apply to buy your Medicare supplement insurance anytime after you turn 65 and join the Medicare part B. So you can add it, you do have to go, like I said, go through underwriting if you wait till after your 65th birthday window open. So you’ll wanna make sure if that’s something you’re looking at, you wanna get to that.

An advantage plan, if you’ve been on original Medicare for five years and you decide you want to join an advantage plan, as long as it’s during an annual enrollment period, you can add that advantage plan at any time.

The cost with the supplement plan, again, are the monthly premiums and the cost with the Medicare Advantage plan is generally a lower monthly premium, but you’re gonna have that cost sharing and co-insurances along the way.

And then prescription drug coverage is not included in a Medicare supplement plan where it is often included in the advantage plan. So that’s kind of what the difference is between those two and how they look. And that kind of wraps up what I was going to talk about today.

Summary – (51:49)

Daniel Ruske: Thank you, Lisa. Great. So once again, just to summarize, we talked about insurance for pre 65, primarily Obamacare. We talked about those changes between 2025 and 2026. We talked about Medicare. Lisa covered it in detail. The costs, the difference between advantage and supplement plans.

And then once again, I just want to mention that with our clients, the way we work with Lisa is we can help you on the timing of Medicare. We sometimes even help you file for Medicare. And then at that point in time we pass it over to Lisa and she’s gonna help you select whether an advantage or a supplement plan, whichever one is best. And then obviously the many options on both of those sides, the array of Advantage plans, and then for the Medigap plans.

So key takeaways here, the cliff on the under age 65, and then you can see the open enrollment dates there. And then for Medicare over age 65, make sure the enroll on time, choose the best plan for you. And then you can see the dates there.

That’s the end of our presentation.

Question and Answer Session – (53:02)

Thank you again for coming. Just a reminder, we’ll take a few questions here. I know Jeff’s probably been busy the entire time. If you do have questions or if your question is more lengthy than we can type out or answer right now, please reach out to one of us.

We have info@petersonwealth.com, and then Lisa’s contact is there if you wanted to get to her directly: evans4health@gmail.com.

Well Jeff, what questions do we have? Do we have any that you think would be beneficial for the group?

Jeff Sevy: Yeah, we have a couple here that I wanted to save till the end because they were great questions. Some of them might be geared more towards Lisa, so I’ll ask those.

Q: What if you get a PPO Advantage plan, do you still have to have in network?

Lisa Evans: Great question. So you do not have to stay in network, but often if you get a PPO plan and you can go out of network, the co-insurance can be up to 50% of whatever the cost of the service is. And so it can get really expensive even though there’s the flexibility of it. It’s a really expensive option. But if that’s something you feel like you want that flexibility, you’re gonna pay to have that flexibility incorporated in your plan.

Q: Can you provide more details on the fines if I continue to fund my FSA account?

Lisa Evans: Daniel, do you know that one? I just know that there’s like a double tax that happens. That’s all I’ve got.

Daniel Ruske: Yes. They’re significant enough that you’re gonna want to undo it and it’s just a big chore to undo it. And so I actually don’t know the details as like the specific dollar amounts. If you over contributed a hundred dollars or something, how much you would have to pay. But what I do know is we’ve helped clients unwind them and it’s just not fun. And so that’s something to be aware of.

Q: If I am on an advantage plan, can I switch to original Medicare during the the annual enrollment period?

Lisa Evans: Yes, you can.

Q: How soon can I, or should I engage with a healthcare professional to begin planning for Medicare enrollment?

Lisa Evans: I think you can engage anytime you’d like. I have met with clients sometimes a year in advance just because they wanna kind of understand what that looks financially for them. And so we’ve kind of sat down, looked at their options, we’ve weighed out whether they wanna stay on work insurance, they wanna continue to, or they wanna switch over.

So sometimes it can be a couple years before they’re even ready to retire, as we’re kind of looking what those options look like. So if you feel like it’s something that you want to understand, reach out to somebody. If it’s something you’re like, nah, I’m fine where I’m at, you can wait a little bit. I don’t think it’s too soon to reach out anytime.

Daniel Ruske: Can I jump in here? As people are approaching 65, I don’t know how we end up on some list, but I feel like our mailboxes are just bombarded with advertisements.

And so sometimes it might be nice to just kind of take a lap interview with a couple people, see if Lisa’s a good match or we have others. And that way you can just ignore everything that is coming because you know that you’re taking care of.

Lisa Evans: Can I throw something out there too? If you do engage with an agent and you don’t feel like they’re doing what you want them to do, feel free to reach out to a different agent. There’s a lot of agents out there who don’t take care of their clients the way that they should.

I’ve had a client that I had an, he had an agent for 10 years and he had been diagnosed with diabetes five years previously and his agent had not been aware and switched him to a plan that was specific for diabetes.

And if your agent isn’t looking out for your best interest, go find an agent who will look out for you. Because that’s really important to have somebody that’s looking out for you.

Jeff Sevy: Awesome, thank you. We’ll do one more question here and then and close up. For anyone that didn’t get their question answered, I included a link for a free consultation with us. So you can go ahead and schedule there and get your questions answered.

Q: Is DMBA coverage after retirement an advantage or a supplement plan, or do they offer both?

Daniel Ruske: This is gonna be a supplement plan. Yep. And so if you have questions specifically about DMBA, let’s talk, we work with a lot of retirees from BYU or church employment. It’s a supplement plan, so we, we can talk about that. That’s kind of pretty specific, so.

Jeff Sevy: Okay. Awesome. Thank you Daniel. Thanks Lisa.

Lisa Evans: Can I just throw one more thing out really quick? I’m also happy to do free consultations just so you understand, as an agent we get paid through the carriers and so our time is free for you if you need something. If you have questions, we’re here to answer those for you and we want what’s in your best interest. So that’s kind of how that works.

Daniel Ruske: Awesome. Okay, thanks again all in the presentation and thanks again for filling out the survey.