Creating a Perpetual Stream of Income to Last through Retirement – (0:00)

Scott Peterson: Welcome, everybody! It’s good to have you with us again this year.

I’d just like to take a moment to welcome everyone. Every year, we like to go through the Perennial Income Model™ to ensure that our clients fully understand how it works. For those of you who are not yet clients, we want to introduce you to this approach.

I’ll admit, I’m probably the least technologically advanced person you’ll ever meet! That’s why I surround myself with great people who can help with that.

For those of you who don’t know us, Peterson Wealth Advisors specializes in managing money for retirees. Over the years, we’ve developed and refined processes that make us leaders in the retirement income space.

Today, I’m going to introduce—or, if you’re already a client, remind you—how the Perennial Income Model works. This is our proprietary process for managing money during retirement. You’ll see why hundreds of retired families across the country depend on this common-sense approach to managing their retirement income.

One of our lead advisors, Carson Johnson, is managing the chat room during this presentation. You’re welcome to reach out to him with any questions you might have. I’ll also set aside time at the end of the presentation to answer any questions.

I find it so interesting that we spend four decades preparing for what we hope will be a comfortable retirement. We’re laser-focused on contributing to our 401(k)s and IRAs, making sure we get our employer match, and ensuring our investments are properly allocated. Over time, we get really good at the art of accumulation. We understand how compound interest works, and we see its power in the years leading up to retirement.

Then something happens that shakes our confidence—we actually retire. Suddenly, we realize that the skill set we’ve spent decades mastering—accumulating wealth—doesn’t necessarily help us when we transition into the decumulation phase, where we start withdrawing money.

This is a completely different skill set, and that’s where we specialize. At Peterson Wealth Advisors, we help retirees effectively manage their money during retirement.

Every retiree has to answer this critical question: How do I create a reliable, tax-efficient, inflation-adjusted stream of income from my benefits and investments that will last throughout retirement with the least amount of risk? That should be the goal of every pre-retiree and early retiree.

The problem is that retirement today is far more complicated than it used to be. I’ve been in this industry for a long time, and early in my career, most retirees had pensions. They might have had a little savings on the side, but pensions were the primary source of retirement income.

Fast forward to today—pensions have largely been replaced by 401(k)s. If you still have a pension, consider yourself lucky. But for most people, managing their own 401(k)s, IRAs, and other savings is now their responsibility.

This shift has created big decisions in retirement—decisions that can have massive financial consequences. Some decisions that seem small or insignificant can end up having a huge impact.

Every financial decision you make in retirement affects other areas of your plan. Nothing happens in a vacuum.

For example:

- The type of retirement account you withdraw from can determine how your Social Security benefits are taxed and how much you’ll pay in Medicare premiums.

- Converting too much of your IRA to a Roth IRA too soon could result in unnecessary taxes now and cause you to miss out on future tax-saving opportunities—especially when it comes to charitable giving.

- Taking what seems like a logical step to minimize taxes today might end up increasing your tax burden down the road when Required Minimum Distributions (RMDs) kick in.

And to make things even more challenging—the rules keep changing.

So, here’s the challenge retirees face: How do you take your Social Security, pension benefits, and investments and turn them into a reliable, lifelong income stream?

I like to use this analogy—In my house, we have a junk drawer in our kitchen. It’s where we keep random items that don’t really have a designated spot. It’s not that the items in the junk drawer aren’t useful—it’s just that they’re unorganized. If I ever need a shoelace or a stapler, I know I can find one in the junk drawer… eventually.

After working with retirees for over three decades, I’ve found that organizing a retiree’s various investments and benefits into a structured income plan is a lot like cleaning out that junk drawer.

Now, just to be clear—I’m not saying your investments are junk! Quite the opposite. They have significant value. But without a structured, organized plan, they can feel scattered, making it difficult to create a reliable income stream in retirement.

This is where our approach comes in. The Perennial Income Model helps retirees turn their accumulated assets into a structured, tax-efficient, and inflation-adjusted income stream designed to last throughout retirement.

And that’s exactly what we’re going to cover today.

On the contrary, these assets have tremendous value. But I want you to think about your own junk drawer of investments and benefits.

Maybe you have a Roth IRA that you opened years ago. You might still have an old 401(k) from a previous employer, along with your existing 401(k). What about your Social Security benefits or a monthly pension? Perhaps you have a lump sum pension and aren’t sure what to do with it.

The challenge is taking this junk drawer of investments and benefits and organizing them into a structured income stream that will last three decades.

Now, that may seem like an overwhelming task. And the reality is, mistakes made at or during retirement can be unforgiving—there are no do-overs.

I once had a client describe the retirement planning process as “like putting a jigsaw puzzle together in the dark.”

Maybe that’s true—but here’s the good news: you don’t have to do it alone. This is what we do—day in and day out. Myself and my team specialize in helping retirees organize their financial puzzle, and we’ve gotten pretty good at it.

We Need a Plan! – (7:23)

At the end of the day, everyone needs an individualized retirement income plan. It’s surprising how few Americans actually have one.

Most people retire with a pile of money, but they don’t know:

- How they should invest it

- How much they can safely withdraw

- Which accounts they should pull from first

And yet, we make plans for everything else in life. We write down a list when we go to the grocery store. We map out itineraries when we go on vacation. But very few people enter retirement with a clear income plan.

That’s concerning because the quality of the next 30 years of your life depends on the decisions you make at retirement and the plan you put in place.

A well-thought-out plan provides discipline, order, safety, and peace of mind. A sound retirement income plan allows you to focus on your retirement dreams instead of constantly worrying about daily market movements, interest rates, or current events.

And here’s the thing—a retirement income plan should be unique to you. That means copying your retired neighbor’s plan won’t work. Following a generic withdrawal rule of thumb from a financial advisor isn’t enough. Buying an annuity that can’t keep up with inflation will only erode your future purchasing power.

And if you’ve been investing for decades, you probably already know that timing the market and guessing its next move isn’t a winning strategy.

So now that I’ve pointed out the common mistakes in retirement income planning, you’re probably wondering—what should you do instead?

That’s exactly what we’re going to cover today. We’re going to build a retirement income plan together, and I’ll show you how we professionally design plans for our clients.

But before we dive into how to build a plan, let’s take a step back and define what a retirement income plan should accomplish.

First of all, it needs to be goal-specific. I like to use this example: There’s a big difference between a person who says, “When I retire, I’d like to own a cabin by the lake.” Versus someone who says,

“I want to retire in 20 years, and I want a cabin by the lake. I estimate it will cost $600,000, so I need to save $1,300 per month for the next 20 years and earn a 6% return on my investments to reach my goal.”

The first person has a wish. The second person has a plan. A goal-specific, date-specific, and dollar-specific plan defines exactly how much income will be needed during retirement and when it will be needed.

By knowing when income will be needed, we can create an investment blueprint to guide us through retirement. A properly structured retirement income plan delivers future income with the least amount of risk, after considering all potential challenges.

Second, it must provide a structured withdrawal framework. At retirement, you are managing the largest sum of money you’ll ever have—and it has to last you the rest of your life.

That means you need to answer this fundamental question: How much can I, or should I, withdraw from my investments?

This isn’t something you can guess at. It has to be carefully planned so that your income is sustainable throughout retirement, allowing you to fully enjoy the experience.

We see two common types of retirees when it comes to this challenge. We see two common tendencies when it comes to retirees and their spending habits.

First, some retirees overspend once they retire. And I get it—you’ve spent 40 years saving for retirement. Now that you’ve finally arrived, it’s easy to feel entitled to spend your money however you want.

The problem is, without a plan, some retirees blow through their savings in the first 10 years of what should be a 30-year retirement. That’s obviously not a good situation.

On the other extreme, some retirees underspend because they’re afraid of running out of money.

Even though their investment statement shows a large balance, they hesitate to withdraw anything. Their fear of the future leads them to shortchange their retirement experiences, preventing them from fully enjoying the life they worked so hard for.

So how do you strike the right balance?

To give yourself the best chance of not outliving your money, experts generally recommend withdrawing no more than 4% per year from your total nest egg.

However, a recent study by the Employee Benefit Research Institute—a nonprofit research group—found that many retirees withdraw an average of 15% per year from their retirement investments. This is simply unsustainable.

A distribution framework provides the structure and discipline needed to withdraw the right amount from your investments throughout retirement.

Third, we need an investment framework that provides reliable income with the least amount of risk—after all risks have been considered.

But first, let’s define what risk actually means. We believe risk is the chance of losing purchasing power. Many retirees either ignore certain risks or don’t fully understand the risks that can cause the greatest financial harm in retirement.

Some of your retirement funds will need to be liquidated in the next few years to provide income. We call this short-term money. Other money won’t be needed for many years. We call this long-term money.

These two types of money face different risks and different rewards.

Two Main Types of Risk- (14:23)

When it comes to retirement risks, there are two main concerns:

- Stock market volatility in the short-term

- Inflation risk over the long term

Let’s talk about the short-term market volatility. Equities (stock-related investments) experience a lot of volatility.

You already know this if you’ve been managing your own money for a long time. If mismanaged, retirees can lose money investing in equities—especially when they need to withdraw funds during a market downturn.

That’s why having a portion of your investments in safe, low-volatility assets is critical for protecting your short-term income. We refer to these as “safe money” accounts, typically fixed-income investments.

However, while fixed-income investments can help avoid short-term volatility, they are terrible for long-term growth because they can’t keep up with inflation.

We all understand inflation much better now than we did five years ago. Inflation is a gradual but lethal loss of purchasing power. Even during periods of relatively stable inflation, the historical long-term average has been around 3% per year.

At just a 3% inflation rate, $1 today will only buy 41 cents worth of goods at the end of a 30-year retirement. Unless you’re willing to reduce your lifestyle and spending by 60%, inflation must be actively addressed in your investment strategy.

Fortunately, we can mitigate inflation risk by investing in inflation-beating assets—namely, equities. Equities experience short-term volatility, but they have always outpaced inflation over the long run.

Let’s think about risk in terms of time. Over time, the risk of owning equities decreases. Over time, the risk of owning fixed-income investments increases due to inflation.

That’s why a well-structured retirement plan must include safe investments for short-term income that are not subject to stock market volatility and also growth investments in equities to ensure your money keeps up with inflation over time.

A solid plan strikes the right balance between volatility-protected assets and inflation-beating investments. Ultimately, your plan must match your future income needs with your current investment portfolio—ensuring your money is both protected and growing.

So far, we’ve covered three essential components of a strong retirement plan. Now, let’s add a fourth of minimizing taxes. Tax-saving opportunities don’t happen by accident—they come from careful planning. This is especially true for retirees.

A well-designed retirement income plan must consider all sources of income and create a tax strategy that minimizes taxes over a 30-year retirement.

It’s not just about withdrawing the right amount of money—it’s about withdrawing from the right types of accounts in coordination with Social Security and pension benefits for maximum tax efficiency.

We need to determine in advance which accounts—or which combination of accounts—to withdraw from each year to create a tax-efficient retirement income stream.

To summarize, these are the four things we need our retirement plan to do for us.

We’ve created a plan that does all of this—but before we dive into how it works, let me explain how this plan came to be. Back in the early 2000s, after the dot-com bubble burst and the 9/11 attacks, I became extremely frustrated with the investment industry. Like most financial advisors, I was constantly searching for the right economist to follow—someone who could accurately predict the market’s short-term direction. The idea was simple: if we could correctly predict where the market was headed, we could adjust our clients’ investments accordingly.

The problem was every economist—and there were thousands of them—had different predictions about where the market was going. And I was supposed to figure out which one to believe.

Well, after years of watching the mutual fund industry, the financial media, and countless economists fail to accurately predict the markets, I realized there had to be a better way to invest than just trying to guess the future.

During this time of frustration, I started searching for answers. That’s when I came across a research paper written by Dr. William Sharpe, a Nobel Prize-winning economist from Stanford. Reading his paper changed the trajectory of my career and has since positively impacted hundreds of retired families across America.

Dr. Sharpe introduced the concept of time segmentation.

In his paper, he suggested that a retiree’s investment portfolio should be divided into 30 separate accounts—each responsible for one year of income during a 30-year retirement.

For example, one account would cover year 1 of retirement. Another account would cover year 2 of retirement. And so on—until 30 years of retirement income were accounted for.

The value of this approach was immediately clear to me. Money set aside for year 1 of retirement should be invested very conservatively—because it needs to be safe and stable.

But money set aside for year 30 of retirement needs to be invested entirely differently—because its biggest risk isn’t volatility, but inflation.

In other words, short-term and long-term investments should be managed differently.

While Dr. Sharpe’s concept made perfect sense in theory, it wasn’t practical to implement. Because managing 30 separate accounts for every retiree would be a logistical nightmare.

I didn’t want to create and oversee 30 individual accounts for each of my retired clients. And my clients certainly didn’t want to receive 30 separate account statements in the mail every month.

The hassle and cost made this academically solid idea completely impractical in the real world. So, while the concept was great, nobody was actually going to implement it.

Not long after reading Dr. Sharpe’s paper, I visited a Christmas tree farm with my family. This was one of those farms where you could cut down your own tree.

As we walked through the farm, I noticed something interesting: We passed by saplings—tiny trees that had just been planted. Then we walked by 1-foot trees…then 2-foot trees…then progressively taller trees. Finally, we reached the section of fully grown trees, which were ready to be cut down and sold.

At that moment, something clicked. The Christmas tree farm had planned years in advance for its future income needs. They weren’t just planting trees randomly—they were time-segmenting their income, ensuring a continuous cycle of trees would be available for harvest every single year. And that’s when I had my breakthrough.

The Christmas tree farm had implemented a time-segmented approach of its own—just like Dr. Sharpe’s paper suggested for retirement planning. I remember thinking—if a Christmas tree farm can figure this out, then surely, with all the tools and resources available in the financial industry, I should be able to do the same. There had to be a way to take Dr. Sharpe’s concept of time segmentation and transform it into a practical investment strategy for retirees. So, we went to work.

As I thought through the details, I realized that instead of breaking retirement into 30 separate accounts, I needed to adjust the timeframe for each segment. Instead of one-year increments, I expanded each investment segment to five years.

By structuring six investment segments—each covering a five-year period instead of just one year—the approach became much more practical while still achieving the same objective.

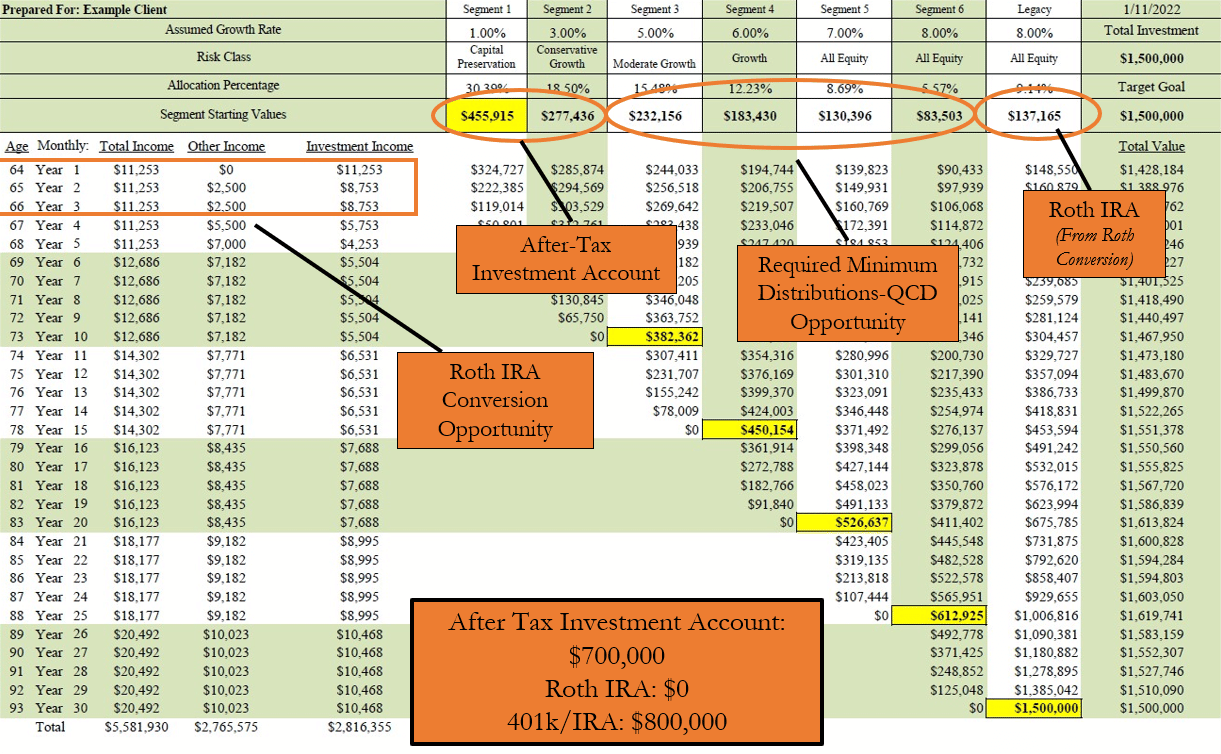

With this refined approach, we created a structure like this:

- Segment 1: Provides income for years 1-5

- Segment 2: Covers years 6-10

- Segment 3: Covers years 11-15

- Segment 4: Covers years 16-20

- Segment 5: Covers years 21-25

- Segment 6: Designed to preserve wealth for heirs

We call these five-year periods “segments” in our office. Once we worked out all the logistics of turning this academic idea into a real-world investment strategy, we officially launched our trademarked version of time segmentation—the Perennial Income Model.

The Perennial Income Model – (25:05)

The Perennial Income Model is not a product. It’s not a one-size-fits-all rule-of-thumb approach. Instead, it’s a customized investment methodology designed to provide a structured, inflation-adjusted income stream.

The Perennial Income Model was born in 2007, and today, it provides income to hundreds of retired families across the U.S. In the 18 years since its creation, this methodology has been tested and refined through some of the toughest financial conditions imaginable.

Think about it—it was tested immediately when the 2008-2009 financial crisis hit.

Yet, despite market downturns, recessions, and economic uncertainty, the Perennial Income Model has continued to help retirees successfully navigate retirement with confidence.

We firmly believe that the Perennial Income Model should be the default approach for generating retirement income for most retirees.

Now, let’s build a real plan using the Perennial Income Model. We’ll create a plan where a family matches their current investments with their future income needs.

This plan will be goal-based, date-specific, dollar-specific, and structured to guide retirees through investing, distribution, risk management, and taxation.

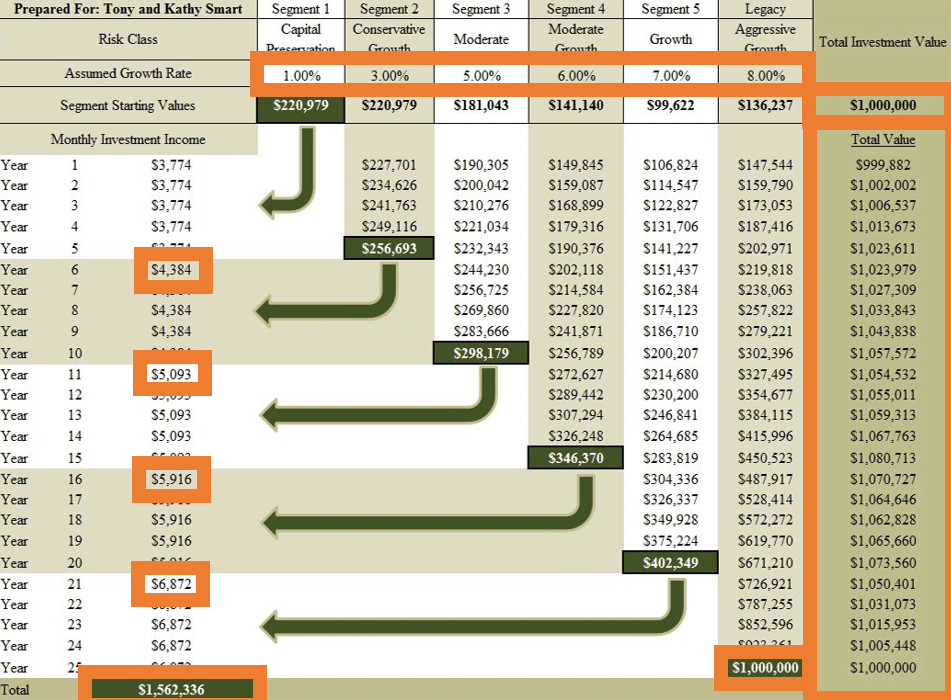

Let me introduce you to the family we’ll be building a retirement plan for Tony and Kathy Smart. Tony Smart is a 65-year-old engineer who has been diligently saving for retirement throughout his career. His wife, Kathy, is a junior high school principal who is very ready to retire.

Together, they have accumulated $1 million in their 401(k)s and IRAs.

Now, they want to know how their $1 million be invested using the Perennial Income Model and how much income can they reasonably expect from their portfolio.

Tony and Kathy believe a 25-year plan will be sufficient, though many retirees plan for 30-35 years. They also want to pass down as much of their $1 million as possible to their children.

For simplicity, I’m going to show you a Perennial Income Model plan using $1 million. I use $1 million as an example because it makes the math easy to follow, but the Perennial Income Model works for portfolios of all sizes—both larger and smaller.

Now, let’s break their $1 million into five investment segments—each designed to provide income for a specific time period. And then we’re going to do a sixth segment that is designed to return a million dollars to the children.

Segment 1: The First 5 Years of Retirement

The first segment will be funded with $220,979 of their $1 million portfolio. The goal of this segment is safety—not high returns.

Since this is the money Tony and Kathy will live on for the first five years, it must be stable and secure. This segment will generate $3,774 per month for their first five years of retirement. The investment approach here is ultra-conservative because this money cannot be subject to market volatility.

We are not trying to hit home runs with this segment. Instead, we are prioritizing safety and stability so Tony and Kathy can comfortably withdraw their monthly income without worrying about market fluctuations.

You’ll notice that I’m using very conservative growth assumptions in this plan. You might be wondering—are we assuming a growth rate higher than 1%? Yes. In reality, we’re seeing 5%+ guaranteed rates in today’s environment. However I intentionally use conservative assumptions to ensure the plan is realistic and stress-tested.

The idea is simple. If the plan works with conservative growth rates, it will absolutely work when returns are higher. Historically, returns have been higher.

Now that we’ve laid the groundwork for Segment 1, we’ll continue building out the full Perennial Income Model plan for Tony and Kathy—covering the remaining segments, risk management, and investment strategies for long-term success.

I want to share some historical rates of return with you. These numbers come from a Vanguard study, and they provide real, data-driven expectations for different types of investment portfolios.

Segment 1 (our most conservative portfolio, with 90% fixed income and 10% stocks) has historically returned 6.9%. Segment 2 (slightly more aggressive) has historically returned 7.7%. And so on, with each segment taking on slightly more risk as time allows for market fluctuations to smooth out.

These aren’t hypothetical numbers—they are based on real historical performance. And these are the conservative numbers we’ll use in today’s presentation.

I don’t want to be accused of using “pie in the sky” numbers, so we’re going to work with ultra-conservative growth assumptions to ensure this plan is realistic. Because if I were retiring, I’d want to make sure my plan worked under the most conservative assumptions possible—not just under best-case scenarios.

Segment 2: Years 6-10

While Segment 1 is distributing income for the first five years of retirement, the remaining balance of the $1 million portfolio continues to grow. Of this remaining amount, we now set aside $220,979 for Segment 2.

Segment 2’s role will start providing income once Segment 1 runs out at the end of year five. Since this money won’t be needed for at least five years, it can be invested slightly more aggressively than Segment 1. However, we don’t want it to be too aggressive—a prolonged bear market could last longer than five years, so we need some level of stability.

In the Perennial Income Model, we assume Segment 2 earns a conservative 3% return. Historically, Vanguard’s study suggests a more typical return of 8%, but we’re staying conservative.

With a 3% return, the original $220,979 grows to $256,000 by the start of year six—right when it’s needed for the next five years of income.

One key thing to notice, their monthly income increases from $3,774 to $4,384 when they enter Segment 2. This is an important feature of the Perennial Income Model—it builds in inflation-adjusted raises every five years.

Segment 3: Years 11-15

Segment 3 is designed to provide income for years 11-15. Because this money won’t be needed for 10 years, we can invest it more aggressively than Segment 2.

In this case, we allocate $181,000 from the original $1 million portfolio into a moderate portfolio (roughly 50% stocks / 50% fixed income). Vanguard’s study shows that a moderate portfolio has historically returned 8.7%, again we’re assuming a conservative 5% growth rate.

With 5% growth, the original $181,000 grows to $298,000 by the time it’s needed in year 11. Their monthly income increases to $5,093 per month when they enter Segment 3.

Segment 4: Years 16-20

For Segment 4, we allocate $141,000 from the original portfolio. This money has 15 years to grow before it’s needed. Since it has a longer time horizon, we can invest more aggressively than in Segment 3. We assume a conservative 6% growth rate (even though historical returns for a moderate portfolio have averaged 9.4%).

With 6% growth, the original $141,000 grows to $346,000 by the time it’s needed in year 16. And once again, the Smarts get another raise—their income increases to $5,916 per month in year 16.

Segment 5: Years 21-25

For Segment 5, we allocate $99,000 from the original portfolio. This money has 20 years to grow, so it can be even more aggressively invested. We assume a 7% growth rate (again, lower than the historical average for long-term equities).

With 7% growth, the original $99,000 grows to $402,000 by year 21. Since this money won’t be needed for two decades, it is heavily invested in equities.

At this point, short-term market volatility doesn’t matter—we aren’t touching this money for 20 years. And once again, the Smarts get another raise.

Segment 6: The Legacy Fund

This brings us to Segment 6, or the Legacy Segment. Remember—Tony and Kathy wanted to leave their original $1 million to their children, if possible.

To achieve this, we set aside $136,000 in a growth-focused account designed to rebuild the original $1 million over time. With an assumed 8% growth rate, this money will compound over 25 years and restore the family’s legacy goal.

This means Tony & Kathy enjoy a secure, structured income throughout retirement. They receive inflation-adjusted raises every five years. They still pass down their original $1 million to their children.

What makes the Perennial Income Model so effective is that it eliminates short-term volatility concerns by keeping near-term income in safe investments. It addresses inflation risk by investing long-term money in equities. It provides a structured, goal-based framework so retirees can enjoy peace of mind.

Unlike generic withdrawal strategies, this plan is designed around the retiree’s specific goals and income needs—ensuring a disciplined, well-structured approach to retirement investing.

With an 8% rate of return, the $136,000 allocated to Segment 6 grows back to the original $1 million over 25 years. Now, keep in mind—8% is the highest return assumption I’ll allow in any of these projections.

Historically, an all-equity portfolio has averaged closer to 12%, but we’re staying conservative to ensure the plan remains realistic. It’s incredible to see how compound interest works in our favor in these later segments.

Think about it—we’re putting in $136,000, and 25 years later, it’s grown back to $1 million. That’s the magic of long-term investing—as long as you let compound interest work for you instead of against you.

Now that we’ve built out the entire plan, let’s step back and look at the big picture.

We’ve used ultra-conservative assumptions. If this plan works using these conservative numbers, it will work even better in real life. In reality, we’re seeing higher returns than this, which should give you confidence in the strength of the model.

You might assume that, because we’re withdrawing money from Segment 1, then Segment 2, then Segment 3, the total account value would gradually decline over time. But that’s not what happens—because while early segments are being used for income, the later segments are still growing. You’ll notice that, even after 25 years of withdrawals, the total value of the portfolio remains close to $1 million—all while funding a full retirement.

Over 25 years, this plan generates more than $1.5 million in retirement income—while still leaving behind $1 million for heirs. This shows how structured investing allows retirees to create a sustainable, inflation-adjusted income without running out of money.

A common question I get is, “Can we take out more money than what’s shown in this plan?” The answer is yes—but it comes with a trade-off.

If you withdraw more, you’ll simply leave less money behind for your kids. This model is built with a balance between lifetime income and legacy goals, but it can be adjusted depending on what’s most important to you.

Whenever I present this at BYU Education Week or other public settings, this is the slide where everyone takes out their cameras to snap a picture. And that’s totally fine—go ahead and take a screenshot if you’d like.

Some people ask, “Why are you so willing to share your ‘secret sauce’?”

Here’s the thing—the magic isn’t in the spreadsheet. Yes, you can take this same pattern and build your own version in an hour or two. But don’t think that means you’re done. Building the plan is the easy part—successfully following it for 25+ years is the real challenge.

The Perennial Income Model takes just a few hours to create, but it takes 30 years of discipline to implement successfully. Those who simply build a spreadsheet, invest, and then forget about it will not have a successful outcome.

When investor discipline fails, the plan fails. This brings us to the most crucial step in implementing the Perennial Income Model: Harvesting.

The Importance of Harvesting – (39:48)

Harvesting is the process of gradually shifting investments from riskier, more volatile assets (like equities) into safer, stable assets (like fixed income) once your goals for each segment are achieved.

Think of it like farming. A farmer spends months fertilizing, pruning, watering, and caring for their trees. But all of that effort only pays off if they harvest the fruit at the right time. If they pick the fruit too early, it’s not ripe. If they wait too long, it rots on the tree.

In the same way, retirees must harvest investment gains at the right time—locking in growth and preserving wealth instead of risking unnecessary losses.

Let me get back to the chart again. You’ll notice that each segment has a green number—that’s the target growth amount for each segment. Whenever a segment reaches that green target number, we have a conversation with our clients.

At that point, we ask do you want to shift this money into safer assets? Or do you want to keep it invested aggressively?

Since we work primarily with retirees, most prefer to take a more conservative approach once their target is met. This allows them to secure their income without worrying about short-term market fluctuations.

Without proper harvesting, the Perennial Income Model takes on unnecessary risk.

If a segment reaches its target amount, but the retiree keeps it invested aggressively, they risk losing that money in a downturn—delaying income and disrupting the plan.

But by locking in gains at the right time, we can ensure that near-term income remains stable and secure, long-term investments still have time to grow, and the retiree can enjoy peace of mind throughout retirement.

The Perennial Income Model is more than just an investment strategy—it’s a disciplined, structured approach to managing retirement income. It eliminates short-term volatility concerns. It protects against inflation over the long term. It provides a structured roadmap so retirees never have to guess what to do next. And most importantly—it works.

By following this approach, retirees can enjoy a steady, reliable, inflation-adjusted income—while still leaving behind a legacy for their children.

Now that we’ve covered how the plan works, let’s take a deeper look at how to implement this strategy successfully over time.

Harvesting is critical to the long-term success of the Perennial Income Model. At first glance, someone unfamiliar with the strategy might notice what appears to be a flaw in the plan.

Without proper management, the older a retiree gets, the more aggressively their portfolio is invested. Now, does it make sense for an 85- or 90-year-old to have all of their money in long-term, aggressive equities? Of course not. But that’s not how the Perennial Income Model actually works—as long as it is being properly harvested and maintained.

This is why the harvesting process—where we gradually shift investments from aggressive to more conservative holdings—is absolutely essential to the model’s success.

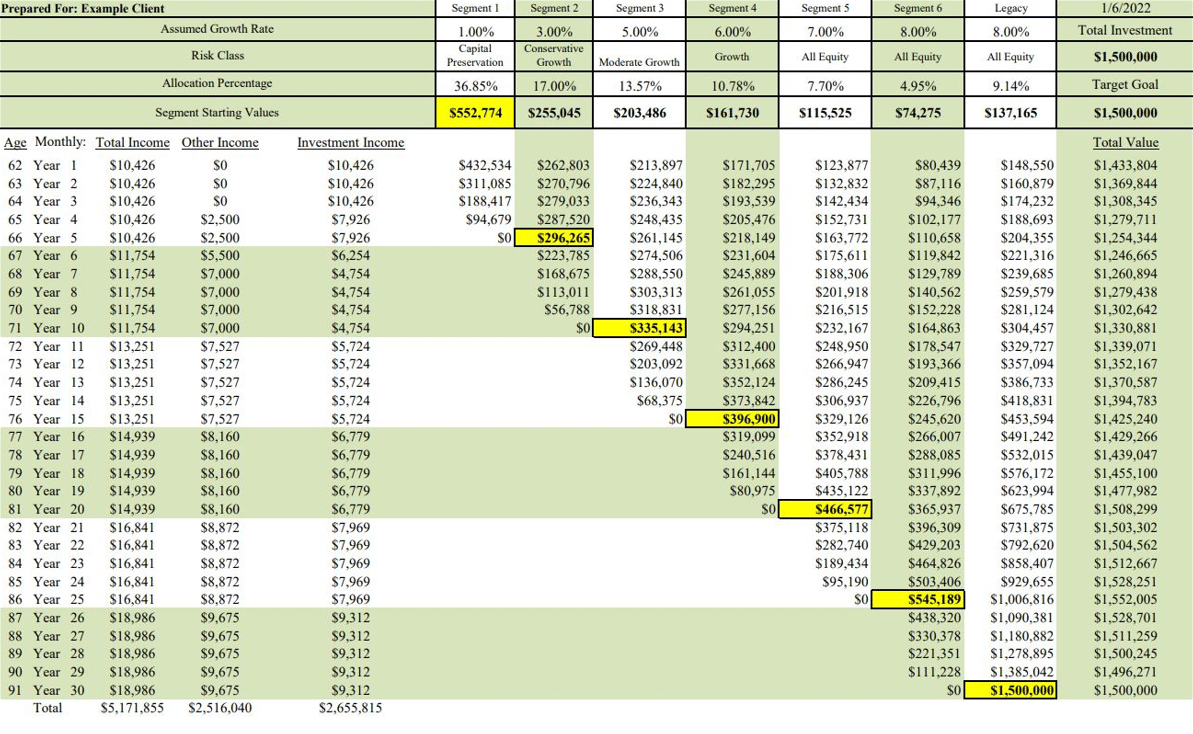

Let’s walk through an example of Segment 5 to illustrate this concept. We allocated $99,000 to this segment. We assumed a 7% growth rate—which means this money is projected to grow to $402,000 over 20 years. In year 21, this segment will begin distributing income for the next five years.

Because Segment 5 won’t be needed for 20 years, we invest it mostly in equities to allow it to grow over time. Now, let’s look at real-world returns. Historically, a growth portfolio has averaged 10% since 1950. But in this model, we are only assuming a 7% return—well below historical averages.

Now, let’s consider what happens if Segment 5 earns 9% instead of 7%. Instead of reaching $402,000 in 20 years, this segment would reach that goal in 16 years and 2 months. At that point, we would have a conversation with the client to discuss shifting some of this money into safer, more conservative investments.

This is exactly how harvesting works—we monitor each segment, and once a goal is reached, we lock in gains and reduce risk.

If you’re trying to implement this plan on your own, harvesting is by far the hardest part. Because you’re not just keeping track of your overall portfolio—you have to track each individual segment.

Over the years, our firm has developed specialized software that allows us to monitor each segment in real time.

For our clients, this means they can log in anytime to see how each segment is performing. They can track their progress toward income goals in a structured way.

Harvesting adds order and discipline to the investment process which results in better investment returns, lower risk, and less selling based on emotions.

How did we do? – (44:30)

At the start of this presentation, we outlined a few key objectives for an ideal retirement plan. Now, let’s go through them again to make sure we accomplished everything.

Is the plan goal-specific? We matched the Smart family’s current investments with their future income needs. The Perennial Income Model provides a date-specific, dollar-specific roadmap for their retirement.

Does it provide a distribution framework? We know exactly how much income the Smart family can withdraw each year while keeping their assets intact. This allows them to spend with confidence, knowing their plan is designed to last.

Even with ultra-conservative growth assumptions, the best annuity in America cannot match the inflation-adjusted income of the Perennial Income Model. If you are being sold an annuity right now, beware—because you can do so much better.

Another question I often get is, “Is this plan too rigid?” Absolutely not.

The Perennial Income Model is not set in stone—it is designed to be flexible and adaptable. Markets Don’t Move in a Straight Line. We make adjustments as market conditions change. If returns are higher than expected, we harvest early and adjust the plan accordingly.

Retirees may need more income than originally planned. Unexpected expenses like illness, family emergencies, or large purchases may arise. The plan allows for withdrawals and adjustments as needed.

Does the plan provide an investment framework? The model ensures that each segment is invested appropriately based on when the money will be needed. Short-term segments are conservative, while long-term segments maximize growth potential.

Do we coordinate all income sources to reduce taxes? Yes.

This model is a guideline for managing money in retirement. We continuously refine and optimize the plan to reflect new financial realities.

At the end of the day, this plan is about giving retirees confidence and control—while ensuring long-term financial security.

Each segment within the Perennial Income Model has a clear responsibility—to provide five years’ worth of income at a future date.

As you can see in the orange box, each segment is strategically invested to fulfill its future income responsibility. This structure allows retirees to invest with confidence. A goal-based plan like this is the antidote to panic during market volatility.

Frankly, I don’t know how anyone could create a retirement income plan without first mapping it out in a structured, logical way—just like we do in the Perennial Income Model.

Now, let’s talk about another critical aspect of retirement planning—coordinating all income sources to reduce taxes. Tax savings in retirement don’t happen by accident—they must be planned.

In the Perennial Income Model, we incorporate all sources of retirement income into our projections, including Social Security, pensions, and investment withdrawals.

We have found that mapping out future income significantly enhances our ability to execute tax-efficient withdrawal strategies.

How can a retiree make smart tax decisions without first understanding their future income stream? How could you possibly determine whether a Roth conversion is beneficial without projecting your future income and tax brackets?

This is why coordinating income distributions is so critical.

By carefully designing the Perennial Income Model, we can create a withdrawal strategy that minimizes taxes by pulling income from the right accounts at the right time. This ensures that retirees can keep more of their hard-earned money and avoid unnecessary tax burdens throughout retirement.

I’d say we met every one of these goals.

Through this plan, we have successfully protected near-term income from market volatility by keeping short-term investments in safe, low-risk assets.

We have protected long-term purchasing power by investing in equities that will grow over time to combat inflation.

We have provided clear guidelines for harvesting investments at the right time to reduce unnecessary risk.

Because of this structured approach, we can confidently say that this plan does everything we need it to do for retirees.

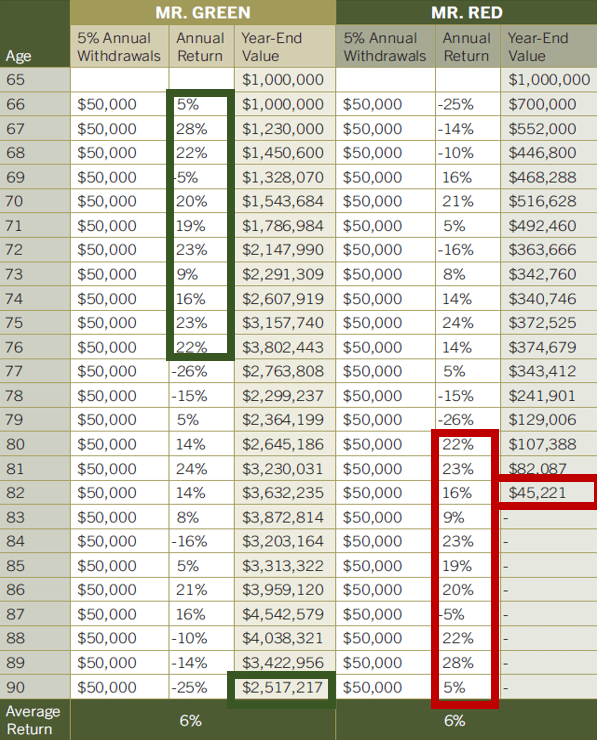

When we first rolled out this plan in 2007, it was almost immediately tested by the 2008-2009 financial crisis.

At the time, about half of our clients had already been transitioned into the Perennial Income Model, while the other half had not yet made the switch.

What we observed was fascinating.

Clients who were following the Perennial Income Model remained calm and disciplined during the market crash. They didn’t panic-sell their investments at a loss. They understood why they owned equities and when they would need them.

Meanwhile, many of the clients who weren’t yet using this strategy struggled. It wasn’t necessarily that their investments performed worse—it was that they lacked the structure and discipline that this plan provides.

This experience reinforced why a structured approach is so important—especially in times of market turmoil.

Benefits of the Perennial Income Model – (51:18)

One unexpected benefit of this model is that it acts as a “bad luck insurance policy” for retirees. What do I mean by that?

The five years before and after retirement are the most dangerous years for investors. If the stock market crashes right when you retire, it can severely impact your long-term financial security—unless you’re prepared.

Many of us remember people who retired in 2007, just before the financial crisis of 2008-2009.

During that time stocks dropped 50%. Many unprepared retirees had to sell their equities at a loss just to pay their monthly bills. Their retirement accounts were devastated.

The Perennial Income Model protects against this scenario by ensuring that retirees have enough safe, stable investments to ride out a market crash. Long-term investments have time to recover before they are needed.

So even if you are the unluckiest person in the world and retire right before a stock market crash, your long-term financial plan won’t be derailed—as long as you follow this model.

Another benefit is The Perennial Income Model protects us from our older selves.

Studies show that as we age, our memory worsens and our financial decision-making skills decline. Many retirees struggle with when to sell investments, when to adjust risk, or when to withdraw income.

A cognitively sharp, confident 65-year-old gradually transforms into a less confident, slower-to-comprehend 80- or 90-year-old. And the reality is—this will happen to every one of us, to some degree or another.

Our older clients who follow the Perennial Income Model are less prone to panic during market downturns because they’re continuing the same plan they’ve followed for years—giving them confidence even as they age.

One of the most unexpected benefits of this model is that it serves as a financial guardian when a spouse passes away. If you’re the only one watching this webinar today, chances are you are the designated financial decision-maker in your household.

Who will help your spouse make sound financial decisions if something happens to you?

It’s a cruel reality that a newly widowed spouse must make major financial decisions at the worst possible time—right after losing their partner.

Many widows and widowers experience shock, situational depression, and struggle to get through each day. Unfortunately, this is also the time when they are most vulnerable to fraud and financial mistakes.

Experience has taught me that more fraud is committed against new widows and widowers than any other group.

I’ve personally seen cases where a brand-new motorhome worth $100,000 was sold for $19,000. Homes and cabins were sold for hundreds of thousands below market value by panicked spouses who feared they wouldn’t have enough money.

When a spouse passes away, there will certainly be some paperwork to sign to transfer assets. But beyond that, the surviving spouse doesn’t have to make drastic financial decisions—they simply continue following the same plan they’ve been using for years.

This predictability and structure provide tremendous peace of mind during an incredibly difficult time.

The benefits of this model are clear. It’s goal-specific. It provides a structured framework for investing, withdrawals, and taxation. It protects against market downturns, cognitive decline, and financial vulnerability.

At its core, the Perennial Income Model is simply a common-sense approach to managing investments during retirement.

Summary – (57:24)

The Perennial Income Model is a commonsense approach to managing your investments during retirement. This model is not about chasing the highest possible returns. It is not a guarantee.

Instead, it is a structured plan to provide the most consistent, inflation-adjusted income possible. It’s also a strategy designed to minimize risk while maximizing long-term income stability while being a proven approach to managing investments for retirees.

In my experience, this is the best approach to managing retirement income that I’ve ever seen.

I get this question all the time, “If this strategy makes so much sense, why don’t all retirees use it?”

Here’s my honest answer. It’s more complex to create and manage. Unlike traditional investing—where you just buy mutual funds and let them grow—this model requires monitoring multiple investment segments and harvesting at the right time.

It requires ongoing adjustments. The plan is not static—it evolves over time as market conditions change and as investors meet their goals.

It takes more effort than traditional “buy-and-hold” investing. Accumulating money for retirement is simple—you just contribute and let your investments grow. But managing money in retirement is different—you need a structured withdrawal plan, tax strategy, and investment discipline.

Because this model requires careful tracking and adjustments, we’ve developed custom software tools that monitor the growth of each segment, alert us when it’s time to harvest gains and ensure every client stays on track with their long-term income plan.

The Perennial Income Model is designed for people who accept reality—that market timing is a gamble and that a structured, long-term plan is the smartest approach.

I’ve written a book about building a retirement income plan using the Perennial Income Model. If you don’t already have a copy, I invite you to scan the QR code or visit our website to request a complimentary copy.

At the end of the day, every retiree must ask themselves, “Will I outlive my money, or will my money outlive me?”

I don’t know everything about your finances. But I can tell you this. You are much more likely to have your money outlast you if you follow a structured plan.

Your retirement income plan should be goal-based and serve as a long-term guide for your financial decisions. It should drive your investment and withdrawal choices and influence your spending and gifting decisions.

Planning your retirement income is so much more than just buying an annuity or following an oversimplified withdrawal rule.

My hope is that this presentation has opened your eyes to a better way to manage retirement income.

By incorporating these strategies, you can face your financial future with confidence, have the peace of mind to freely pursue your retirement dreams, and enjoy retirement without the constant worry of running out of money.

The Perennial Income Model appeals to logical, goal-based investors. We know the economy and the stock market will always have ups and downs.

I appreciate you spending time with us today.

The purpose of this model is simple to provide a secure stream of income that keeps pace with inflation and to allow you to focus on what’s truly important—family, faith, and personal fulfillment.

That’s the real reason we use the Perennial Income Model.

Question and Answer Session – (1:02:35)

Scott Peterson: Now, I know there are some great questions coming in, and Carson has been answering them in the chat. But let’s take a few minutes to address some of the best ones.

Carson Johnson: We have some great questions and should take 5 minutes to answer these. How is the investment management fee factored into the plan?

Scott Peterson: When we show you this plan, our fee is already built in. We intentionally use conservative return assumptions to account for our management fee. If our management fee is 1%, it is already factored into the projections.

We don’t add additional costs on top of the plan—it’s all included.

This ensures that the numbers we present are realistic and achievable.

Carson Johnson: How does Peterson Wealth charge fees? We charge a percentage-based fee on assets under management. This fee is billed quarterly—we take one-fourth of the annual fee every three months.

Scott Peterson: If the annual fee is 1%, we take 0.25% per quarter. The fee is clearly listed on your statements—there are no hidden charges. Unlike commission-based advisors, everything is fully transparent.

Carson Johnson: How long will Peterson Wealth be around to manage this plan for me?

Scott Peterson: I get this question all the time—especially since retirement planning is a 30+ year process. First of all—yes, I’m 63 years old, and I understand the concern.

Right now, we have 18-19 people on our team, and every one of them believes in and follows the Perennial Income Model.

Carson, who’s answering questions online, is just over 30 years old. Our team of advisors is young, dedicated, and fully aligned with this approach. So whether you’re working with me or another advisor, you’ll always get the same plan and the same results—because our process is structured, repeatable, and built to last.

We also have a transition plan in place for when I retire. The Perennial Income Model will continue carrying on with or without me, ensuring you have the same trusted process for decades to come.

Carson Johnson: How Are Required Minimum Distributions (RMDs) Factored into the Plan?

Scott Peterson: When we create your plan we match your investments with your projected income needs, take into account Social Security, pensions, and RMDs, and make sure withdrawals are optimized for tax efficiency.

Every client is different, so RMD strategies vary from person to person. If you follow this plan, RMDs are naturally accounted for—you won’t have to scramble to figure out how to handle them later.

Carson Johnson: When is the right time to start this strategy?

Scott Peterson: Reach out to us about a year before you retire. At that stage, we can help you optimize your 401(k) investments in preparation for retirement. We won’t start charging fees until you’re actually in retirement, but getting ahead of the process ensures everything is set up properly.

Carson Johnson: Do you work with clients outside of Utah?

Scott Peterson: Yes, in fact, about 50% of our new clients are from outside Utah. So if you’re outside of Utah—we can still work with you and implement this plan for your retirement.

I really appreciate everyone joining us today. We look forward to talking with you soon. Have a wonderful day, and thank you for joining us!